Notes

|

Topics to be Learn :

|

Introduction, Meaning and Need for maintaining Subsidiary Books

Introduction :

- When the number of business transactions is small, all transactions can be recorded in one book called the journal.

But when the number of transactions increases, it becomes difficult to record everything in a single journal. - To solve this problem, the journal is divided into different books.

These separate books are called Subsidiary Books.

Meaning of Subsidiary Books : Subsidiary books are books of original entry. They are maintained along with the journal to record similar types of repeated transactions.

Need for Maintaining Subsidiary Books

- Specialisation : Different clerks can maintain different subsidiary books. This creates specialisation in work and increases efficiency.

- Saving of Time and Money : Many accounting tasks can be done at the same time by different persons. This helps in saving time and reduces cost.

- Division of Work : Work can be divided among many employees. This reduces workload and keeps accounts updated regularly.

- Quick Information : Information about a particular account can be found quickly. It also becomes easy to check and verify entries.

- Internal Check : Entries recorded in subsidiary books can be checked easily. This helps in reducing mistakes and improving accuracy.

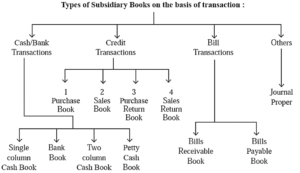

Following are the important Subsidiary Books.

1) Cash Book. 2) Petty Cash Book.

3) Purchase Book 4) Purchase Return Books (Return Outward Book)

5) Sales Book 6) Sales Return Book (Return Inward Book)

7) Journal Proper

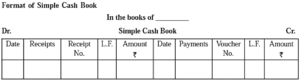

Cash Book with Cash Column (Simple Cash Book) :

All cash and bank transactions are recorded in the Cash Book. The Cash Book has two sides:

- Left-hand side – Receipt Side (Debit Side)

- Right-hand side – Payment Side (Credit Side)

Receipt Side : When money is received, the details are recorded on the receipt side.

Payment Side : When payments are made, the details are recorded on the payment side.

Features of Cash Book :

- The Cash Book is a Book of Original Entry because transactions are recorded in it for the first time.

- It is also a Ledger because cash and bank transactions are classified in ledger form.

- It helps in finding the cash balance and bank balance at the end of an accounting period.

- Thus, the Cash Book serves a dual purpose: (i) As a Journal (ii) As a Ledger

Cash Book with Cash and Bank Columns (Two Column Cash Book) :

Banks play an important role in business activities. They provide many useful services to traders and businessmen.

Services Provided by Banks :

- Banks accept deposits from customers.

- They allow withdrawal of money through: Cash, Cheques, Net banking transactions

- Banks make payments through cheques and drafts.

- They provide loan and cash credit facilities.

- They collect cheques on behalf of customers.

- Banks also provide safety for cash.

- A businessman with a current account can get an Overdraft Facility.

Current Account : Businessmen who have many banking transactions usually open a Current Account. This helps them to use the overdraft facility provided by the bank.

Columns in a Two Column Cash Book

A Two Column Cash Book contains:

- Cash Column

- Bank Column

Both columns appear on:

- Receipt Side (Debit Side)

- Payment Side (Credit Side)

Bank Column :

- The Bank Column is used to record only bank transactions.

- It represents the Bank Current Account of the business.

A Two Column Cash Book helps in recording both: Cash transactions and Bank transactions in one book in a simple and systematic manner.

Format of Cash Book with Cash and Bank columns :

Accounting treatment of banking transactions in Cash Book with Cash and Bank columns :

In a Cash Book with Cash and Bank columns, the "Bank" column is used to record all banking transactions, representing the business's Current Account. The accounting treatment for these transactions is detailed below:

(1) Opening Balances

- Debit Balance: If the bank account has a positive balance, it is recorded on the receipt (debit) side in the bank column as "To Balance b/d".

- Credit Balance (Bank Overdraft): If the account is overdrawn, it is recorded on the payment (credit) side in the bank column as "By Balance b/d".

(2) Cheque Transactions :

- Cheque Received:

- Crossed Cheque: Recorded on the receipt side in the bank column.

- Bearer Cheque: Treated as cash and recorded on the receipt side in the cash column.

- Same-day Deposit: If a cheque is received and deposited immediately, it is recorded on the receipt side in the bank column.

- Cheque Issued: Recorded on the payment side in the bank column.

- Dishonoured Cheques:

- If a received cheque is dishonoured, it is recorded on the payment side to cancel the previous receipt.

- If an issued cheque is dishonoured, it is recorded on the receipt side.

(3) Bank Advices and Statements :

Transactions initiated by the bank are recorded based on bank advices or statements:

- Receipt Side (Bank Column): Includes direct deposits by customers, interest allowed by the bank, and dividends or interest on investments collected by the bank on behalf of the trader.

- Payment Side (Bank Column): Includes interest charged on overdrafts, bank charges for services rendered, and payments made under standing instructions (e.g., insurance premiums, utility bills).

(4) Contra Entries :

Contra entries occur when a transaction affects both the Cash and Bank accounts simultaneously. They are denoted by a "C" in the Ledger Folio (L.F.) column.

- Cash Deposited into Bank: Recorded on the receipt side (Bank column) and the payment side (Cash column).

- Cash Withdrawn for Office Use: Recorded on the receipt side (Cash column) and the payment side (Bank column).

- Bearer Cheque Deposited Later: When a previously received bearer cheque (initially treated as cash) is deposited, it is treated like a cash deposit.

(5) Transfers Between Accounts :

- To Current Account: Transfers from a loan account or a proprietor’s personal savings account (treated as Capital) are recorded on the receipt side in the bank column.

- From Current Account: Transfers to a loan account or a proprietor’s personal savings account (treated as Drawings) are recorded on the payment side in the bank column.

(6) Balancing the Bank Column :

At the end of the accounting period, the bank column is balanced:

- A Debit Balance (Receipts > Payments) is a positive balance.

- A Credit Balance (Payments > Receipts) indicates a Bank Overdraft.

Types of bank account :

(1) Current Account : A trader or a businessman can open a Current Account with bank, as there is no restriction on number of transactions for deposits, payments or withdrawals. Interest on current account is not given by bank but bank can give overdraft facility on current account. with certain conditions.

(2) Savings Account : To develop the habit of savings, for a person having fixed or regular income, Savings Account can be opened in a bank. Restriction is imposed on the withdrawals and payments in a savings account. No overdraft facility is available on this account.

(3) Fixed Deposit Account : An account in which fixed amount is deposited for a fixed period of time in order to earn higher rate of interest is known as Fixed deposit account.

(4) Recurring Deposit Account : An account in which account holder deposits fixed amount, at regular interval for a predecided period, is known as Recurring deposit account.

Simple and Analytical Petty Cash Book Under Imprest System :

A book which is maintained for recording small expenses, which cannot be paid by cheque, is known as Petty cash book. It is maintained by Petty cashier, in large business organisation.

There are two types of Petty cash book.

(1) Simple Petty Cash Book :

Meaning : When cash or cheque is received by petty cashier, it is recorded in the 'Amount received' column and different types of small expenses/petty expenses are recorded in the 'Amount paid' column. Then after it is to be posted to respective expense account which require more time. So, in practice, it is not used by traders.

Specimen of the Simple Petty Cash Book :

| Amount Received (₹) | Date | Particulars | Voucher No. | L.F. | Total Amount Paid (₹) |

| Total Expenses | [Total] | ||||

| By Balance c/d | [Balance] | ||||

| [Total] | [Total] | ||||

| [Balance] | (Next Date) | To Balance b/d |

Key Features of the Simple Petty Cash Book:

- Amount Received Column: Cash or cheques received from the head cashier as an advance (imprest) are recorded here.

- Particulars Column: This column is used for both receipts (usually starting with "To Cash A/c") and payments (usually starting with "By [Expense Name] A/c").

- Total Amount Paid Column: Every petty expense paid out is recorded in this column.

- Balancing: At the end of the period, the book is balanced to find the remaining cash in hand, which is then brought forward to the next period.

(2) Analytical (Columnar) Petty Cash Book :

Meaning : In analytical petty cash book, when cash is received it is recorded on the 'Receipt side' and when payment is made it is recorded on the 'Payment side' in sub columns for recording various expenses.

Specimen of the Analytical (Columnar) Petty Cash Book :

| Amount Received (₹) | Cash Book Folio | Date | Particulars | Voucher No. | Total Amount Paid (₹) | Analysis of Petty Expenses (Sub-columns) | L.F. | Ledger Account (₹) |

| (Receipts) | (Ref to main Cash Book) | (Date) | (Description) | (Ref No.) | (Total for entry) | (e.g., Printing, Postage, Carriage, etc.) | (Personal/Real A/c) |

Key Components of the Format:

- Receipt Side: Contains columns for the Amount Received from the head cashier and the Cash Book Folio number.

- Transaction Details: Includes columns for the Date, Particulars (describing the nature of the receipt or expense), and the Voucher Number.

- Total Amount Paid: This column records the total value of every petty expense at the time it occurs.

- Analysis Columns: These are multiple sub-columns used to categorize expenses by type, such as Printing & Stationery, Postage, Carriage & Cartage, Travelling Expenses, and Miscellaneous Expenses. There is no "hard and fast rule" for the exact number of these columns; they are created based on the business's needs.

- Ledger Column: A specific column used for payments that need to be posted to Personal or Real accounts rather than general expense accounts.

- Balancing: At the end of a period (usually a month), the total of each expense column is found, and the book is balanced to show the remaining cash in hand (Balance c/d).

This columnar arrangement saves time and labor because it allows the petty cashier to submit a summary of categorized expenses to the chief cashier rather than posting every individual small transaction to the ledger.

Imprest system of Petty Cash Book : The Imprest System is considered the most effective method for maintaining a Petty Cash Book. It operates through a cycle of advance payments and replenishments to ensure the petty cashier always has a fixed amount of cash available at the start of each period.

The system works through the following steps:

- Initial Advance: At the beginning of a specific period (usually a month), the head cashier makes an estimate of the petty expenses required and provides this sum as an advance to the petty cashier.

- Recording Expenses: The petty cashier uses this fund to pay for small, recurring expenses—such as postage, carriage, and stationery—and records them in the Petty Cash Book.

- Account Submission: At the end of the period, the petty cashier presents the record of all payments made to the head cashier for verification.

- Reimbursement (Replenishment): After checking the accounts, the head cashier gives the petty cashier a sum exactly equal to the amount actually spent during that period.

- Restoring the Balance: This replenishment restores the petty cash fund to its original starting amount, allowing the petty cashier to begin the next period with the same fixed sum (the "imprest" amount).

This system is efficient because it provides a built-in check on the petty cashier's work and prevents the accumulation of large sums of unaccounted cash in various departments.

Purchase Book (Bought Day Book) :

The Purchase Book is used to record only credit purchases of goods made for:

- Manufacturing

- Resale

This book is also known as the Purchase Journal.

Transactions Recorded in Purchase Book :

- Only goods purchased on credit are recorded.

- Goods purchased for resale or manufacturing are entered in this book.

Example :

- A business dealing in machinery spare parts will record only the credit purchase of machinery spare parts in the Purchase Book.

- Transactions Not Recorded in Purchase Book

The following transactions are not recorded in the Purchase Book:

- Cash purchases

- Purchase of office equipment

- Furniture

- Stationery

- Building

- Any asset purchased on credit other than goods

Goods purchased on credit are always recorded at their net value.

The Purchase Book helps in recording all credit purchases of goods in a separate and systematic manner.

Purchase Book - Format of Purchase Book :

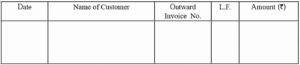

Purchase Return Book (Return Outward Book) :

Goods purchased on credit, if returned to the supplier, are recorded in the purchase return book.

Specimen of Purchase Return Book :

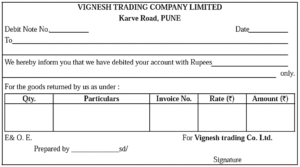

Debit Note : Debit note is a statement containing details of the goods return to supplier. It is prepared by the purchaser of goods.

Format of Debit Note :

Sales Book :

- The Sales Book is used to record only credit sales of goods.

- Cash sales are not recorded in the Sales Book.

- This book is also known as the Sales Journal.

Transactions Recorded in Sales Book

- Only goods sold on credit are recorded.

- Goods sold for business purposes are entered in this book.

Example : A businessman dealing in furniture will record only the credit sale of furniture in the Sales Book. Cash sales of furniture will not be recorded in this book.

Transactions Not Recorded in Sales Book

The following transactions are not recorded in the Sales Book:

- Cash sales

- Sale of assets on credit

- Sale of newspapers or other items not treated as goods of the business

- Recording of Sales

- Goods sold on credit are always recorded at their net value.

The Sales Book helps in recording all credit sales of goods separately and systematically.

Format of Sales Book :

Sales Return Book (Return Inward Book) :

Sometimes customers return goods purchased on credit because:

- The goods are damaged

- The goods are not according to sample

- The goods do not match specifications

- Goods are damaged during transport

Such returns of goods sold on credit are recorded in the Sales Return Book. This book is also known as the Sales Return Journal.

Transactions Recorded in Sales Return Book :

- Only goods returned by customers from credit sales are recorded.

- Transactions Not Recorded

- Return of goods sold for cash is not recorded in this book.

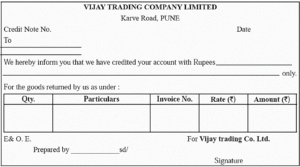

Credit Note :

When goods are returned by the customer, the seller prepares a Credit Note.

Meaning of Credit Note : A Credit Note is a document containing details such as:

- Quantity of goods returned

- Rate of goods

- Amount of return

It shows that the account of the customer returning the goods is credited.

Difference Between Credit Note and Debit Note :

- Credit Note is prepared by the seller.

- Debit Note is prepared by the buyer.

The Sales Return Book helps in recording all returns of goods sold on credit in a separate and systematic manner.

Format of Credit Note :

Format of Sales Return Book :

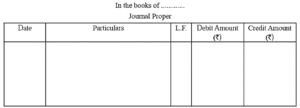

Journal Proper :

- A book used to record transactions that cannot be entered in any Special Journal (Subsidiary Book) is called Journal Proper.

- Transactions that do not fit into books like Cash Book, Purchase Book, or Sales Book are recorded in Journal Proper.

Example : Purchase of assets on credit cannot be recorded in the Purchase Book. Such transactions are recorded in Journal Proper.

Transactions Recorded in Journal Proper :

(1) Opening Entries : At the beginning of a new accounting year, opening balances of:

- Assets

- Liabilities

- Capital

are recorded in Journal Proper.

(2) Adjustment Entries : These entries are made at the end of the accounting period to update accounts on an accrual basis.

Examples:

- Outstanding rent

- Prepaid insurance

- Depreciation

- Commission received in advance

(3) Rectification Entries : These entries are made to correct errors in:

- Recording transactions

- Posting entries into ledger accounts

(4) Transfer Entries : These entries are used to transfer balances from one account to another.

Examples:

- Transfer of Drawings Account to Capital Account

- Transfer of expenses and incomes to Trading and Profit and Loss Account

- These are also called Closing Entries.

(5) Other Entries :

- a) Purchase of assets on credit

- b) Sale of old assets on credit

- c) Withdrawal of goods by proprietor

- d) Bad debts written off

- e) Loss of goods due to: Fire, Theft, Damage in transit

- f) Goods distributed as: Free samples, Charity

- g) Discount received and allowed on cash transactions

Journal Proper is used for recording special transactions that cannot be entered in other subsidiary books. It helps in keeping accounts complete and systematic.

Specimen of Journal Proper :

We reply to valid query.