Notes

|

Topics to be Learn : (1) Meaning of Reconstitution of Partnership :

(2) Admission of a partner :

|

Meaning of Reconstitution of Partnership :

- Reconstitution means forming or creating something again.

- Reconstitution of partnership means changing the old relationship among partners and creating a new one.

- It happens when partners make a new agreement.

- This change may occur due to admission, retirement, or death of a partner.

Different Forms of Reconstitution :

Reconstitution occurs whenever the internal structure of a partnership is altered. According to the Partnership Act and established accounting standards, there are four primary forms of reconstitution:

(1) Change in Profit Sharing Ratio (PSR) : Existing partners redistribute profit entitlements, often due to a change in roles or one partner purchasing a share from another.

- Existing partners may decide to change their profit and loss sharing ratio.

- One partner may purchase a share from another partner.

- The old partnership agreement ends.

- A new agreement is made with a new profit-sharing ratio.

(2) Admission of a New Partner : A new individual joins the firm, contributing fresh capital and expertise.

- A new person can be admitted with the consent of all existing partners.

- The new partner becomes a co-owner of the firm.

- He brings capital and goodwill.

- He gets a share in future profits.

- The partnership agreement changes.

(3) Retirement of an Existing Partner : An existing member exits the firm, requiring a settlement of their capital and share of reserves.

- A partner may retire due to old age, illness, or personal choice.

- He is called an outgoing partner.

- The firm must pay all his dues.

- The remaining partners get a higher profit share.

- The partnership agreement changes.

(4) Death of a Partner : The partner’s legal heir receives their share, and the agreement among continuing partners is revised.

- When a partner dies, he is no longer a part of the firm.

- The partnership ends on natural grounds.

- The profit-sharing ratio of remaining partners changes.

- A new partnership agreement is formed.

Strategic Impact and Liability :

- Each form of reconstitution terminates the old agreement.

- From a strategic perspective, this redefines partner liability and entitlement to future earnings.

- Admission is particularly critical because the existing partners must "sacrifice" a portion of their future profit share to accommodate the newcomer.

- This necessitates a rigorous financial adjustment to ensure that the founding partners are fairly compensated for the business's built-up value.

Meaning of Admission of a Partner :

- Admission of a partner means adding a new person to an existing partnership firm.

- It is done according to the terms and conditions of the partnership deed.

- The new partner brings capital, goodwill, skills, experience, or services.

- In return, he gets a share in future profits.

- He also gets rights in the assets of the firm.

Need of Admission of a Partner :

- Increase in Capital : A new partner brings additional capital into the business. This helps in expanding and improving the firm’s activities.

- Benefit of Skills and Experience : The new partner may have better skills, knowledge, or experience. He may also bring useful business contacts. This improves efficiency and overall performance of the firm.

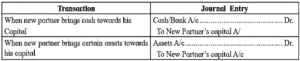

Capital brought in by new partner :

At the time of admission, new partner is required to bring in cash or/and other assets, if any, as his capital, to get rights in the assets and definite share in the future profit of the firm.

When a new partner brings in cash towards his share of capital, the following journal entry is passed :

New Profit Sharing Ratio :

- When a new partner is admitted, he gets an agreed share of future profits.

- The remaining profit is shared by the old partners.

- Therefore, the profit-sharing ratio of old partners changes.

- A new ratio is calculated for all partners (old + new).

- This new ratio is used for goodwill adjustment and capital account changes.

Calculation of New Ratio :

(1) When New Partner’s Share is Given

Assume total profit = 1.

Remaining share of old partners = (1 – new partner’s share).

New Ratio = Remaining share × Old Ratio.

(2) When Sacrifice Ratio is Given :

Sometimes, old partners sacrifice a part of their share.

New Ratio = Old Ratio – Sacrifice Ratio.

The new profit-sharing ratio shows how profit will be divided after admission of a new partner.

Sacrifice Ratio :

- When new partner is admitted old partners have to sacrifice their share of profit to give the share of profit to new partner.

- The ratio in which the old partners sacrifice their share of profit is called as sacrifice ratio.

- This ratio is used to retain the goodwill in premium method.

Sacrifice ratio = Old Ratio - New Ratio

Examples :

Ex.1: (Calculation of New ratio)

Mohan and Ganpat are sharing profits and losses in the ratio of 2:3. They admitted Chandrakant for 1/4th share in future profit. The new profit sharing ratio of Mohan, Ganpat and Chandrakant will be as under

Formula = 1 - share of New Partner = 1 – \(\frac{1}{4}\) = \(\frac{3}{4}\) Remaining Profit

New Ratio = Old Ratio × balance of 1

Mohan’s New Ratio = \(\frac{2}{5}\) × \(\frac{3}{4}\) = \(\frac{6}{20}\)

Ganpat’s New Ratio = \(\frac{3}{5}\) × \(\frac{3}{4}\) = \(\frac{9}{20}\)

Chandrakant’s Ratio = \(\frac{1}{4}\) i.e. \(\frac{5}{20}\)

New Profit Sharing Ratio will 6 : 9 : 5

Ex.2: (Calculation of Sacrifice Ratio)

A and B are Partners sharing profits in the ratio of 6:4. C is admitted as a partner. The new profit sharing ratio of A, B and C is 10 : 6: 4. Find out the sacrificing ratio.

Sacrifice ratio = Old Ratio - New Ratio

A's sacrifice = \(\frac{6}{10}\) - \(\frac{10}{20}\) = \(\frac{2}{20}\)

B’s Sacrifice = \(\frac{4}{10}\) - \(\frac{6}{20}\) = \(\frac{2}{20}\)

Sacrifice ratio of A and B = \(\frac{2}{20}\) : \(\frac{2}{20}\) or 2:2 = 1 : 1

Ex.3: (Calculation of Sacrifice Ratio and New Ratio)

Pravin and Navin are partners sharing profits in the ratio of 7:3 They admit Reena for 1/5th share of profit which he takes equally from Pravin and Navin. Calculate sacrifice ratio and new profit sharing ratio.

Reena’s share = \(\frac{1}{5}\)

Sacrifice Ratio of P and Q = 1:1 or \(\frac{1}{2}\) : \(\frac{1}{2}\)

Pravin’s Sacrifice = \(\frac{1}{5}\) × \(\frac{1}{2}\) = \(\frac{1}{10}\)

Navin’s Sacrifice = \(\frac{1}{5}\) × \(\frac{1}{2}\) = \(\frac{1}{10}\)

New Ratio = Old Ratio - Sacrifice Ratio

New Share of Pravin = \(\frac{7}{10}\) - \(\frac{1}{10}\) = \(\frac{6}{10}\)

New share of Navin = \(\frac{3}{10}\) - \(\frac{1}{10}\) = \(\frac{2}{10}\)

Reena’s share = 1/5th share = \(\frac{2}{10}\)

Therefore, New Ratio is 6 : 2 : 2 = 3 : 1 : 1

Ex.4: (Calculation of Sacrifice Ratio and New Ratio)

X and Y are partners sharing profits in the ratio 7:3. X surrenders 1/7th of his share and Y surrenders 1/3rd of his share in favour of Z, a new partner. Calculate new ratio and sacrificing ratio.

Old Ratio of X and Y = 7:3 or \(\frac{7}{10}\) : \(\frac{3}{10}\)

X’s Sacrifice = \(\frac{1}{7}\) × \(\frac{7}{10}\) = \(\frac{1}{10}\)

Y’s Sacrifice = \(\frac{1}{3}\) × \(\frac{3}{10}\) = \(\frac{1}{10}\)

Sacrificing ratio of X and Y = \(\frac{1}{10}\) : \(\frac{1}{10}\) or 1:1

Z’s share = X’s share + Y’s share = \(\frac{1}{10}\) + \(\frac{1}{10}\) = \(\frac{2}{10}\)

X’s New share = Old ratio - Sacrifice ratio = \(\frac{7}{10}\) - \(\frac{1}{10}\) = \(\frac{6}{10}\)

Y’s New share = Old ratio - Sacrifice ratio = \(\frac{3}{10}\) - \(\frac{1}{10}\) = \(\frac{2}{10}\)

Therefore, New Ratio of X, Y and Z = 6 : 2 : 2 = 3 : 1 : 1

Meaning of Goodwill :

- Some firms earn more profit than others in the same business.

- This extra earning capacity is called goodwill.

- Goodwill is the value of a firm’s reputation and future profit-earning ability.

- It includes benefits like good name, reputation, and business connections.

- It is an intangible asset, which means it cannot be seen or touched.

- Goodwill is built slowly over time through continuous efforts.

Definitions :

- According to Lord Macnaghten: Goodwill is the benefit of good name, reputation, and connections of a business.

- According to ICAI: Goodwill is an intangible asset arising from business reputation, connection, or trade name.

Factors Affecting Goodwill :

- Monopoly position of the business.

- Continuous success and prosperity.

- Reputation, location, and business connections.

- Trademark, brand name, and patents.

- High profit-earning capacity.

- Good relations with customers, employees, etc.

Nature of Goodwill :

- It is an intangible asset.

- It cannot be seen or physically verified.

- It cannot be sold separately from the business.

When Goodwill is Valued :

- At the time of sale or purchase of a business.

- On admission of a partner.

- On retirement or death of a partner.

- On change in profit-sharing ratio.

Methods of Valuation of Goodwill :

As prescribed in the syllabus, the value of goodwill as on a particular date is ascertained by using any one of the following methods : (A) Average Profit Method and (B) Super Profit Method.

(A) Average Profit Method : Under this method, goodwill is valued at certain number of years' purchases of the average profit of the firm. To compute the value of Goodwill as per this method the following formulae are used :

(1) Total Profits = Profits of the given number of years - losses, if any.

(2) Average Profit = \(\frac{\text{ Total profit of given no. of years}}{\text{No of years given}}\)

(3) Goodwill = Average Profit x No. of years' purchases

(B) Super Profit Method of Goodwill : Under this method, goodwill is calculated based on super profit. It is valued as a certain number of years’ purchase of super profit.

(1) Super Profit : Super profit is the extra profit earned over normal profit.

Super Profit = Average Profit - Normal Profit

(2) Normal Profit (Normal Return on Capital Employed) : It is the reasonable profit required for a business to survive. It depends on capital employed and normal rate of return.

Normal Profit = Capital Employed x Normal Rate of Return

(3) Capital Employed : It is the total capital used in the business.

It includes:

- Fixed assets (excluding goodwill)

- Plus current assets

- Minus current liabilities

(4) Normal Rate of Return : It is the average profit rate earned by similar firms in the industry. It depends on the type of business and risk involved.

(5) Goodwill under Super Profit Method : Goodwill is calculated as:

Goodwill = Super Profit x Number of Years' Purchase

Higher super profit leads to higher goodwill value.

Examples :

To value goodwill, businesses often use the performance of past years to estimate future reputation and profit-earning capacity.

Below are examples of valuation using the Average Profit Method and the Super Profit Method.

(i) Average Profit Method : Under this method, goodwill is calculated based on the average profits of a past number of years. It assumes the firm will maintain this level of profit for a certain period in the future.

Example: Suppose a firm has the following profits and losses over the past four years:

- 2016: ₹1,20,000 (Profit)

- 2017: ₹80,000 (Profit)

- 2018: ₹20,000 (Loss)

- 2019: ₹60,000 (Profit)

Step 1: Calculate Total Profit Total Profit = 1,20,000 + 80,000 - 20,000 + 60,000 = ₹2,40,000.

Step 2: Calculate Average Profit Average Profit = Total Profit / Number of years Average Profit = 2,40,000 / 4 = ₹60,000.

Step 3: Calculate Goodwill If goodwill is valued at 2 years' purchase of the average profit: Goodwill = Average Profit × Number of years' purchase Goodwill = 60,000 × 2 = ₹1,20,000.

(ii) Super Profit Method : Super profit is the profit earned over and above the normal profit expected in the industry. This method considers the capital employed and the Normal Rate of Return (NRR).

Example: Consider a firm with the following data:

- Capital Employed: ₹3,50,000

- Normal Rate of Return (NRR): 12%

- Average Profit (calculated from past 5 years): ₹66,000

- Goodwill Valuation: 2 years' purchase of super profit.

Step 1: Calculate Normal Profit Normal Profit = Capital Employed × (NRR / 100) Normal Profit = 3,50,000 × (12 / 100) = ₹42,000.

Step 2: Calculate Super Profit Super Profit = Average Profit - Normal Profit Super Profit = 66,000 - 42,000 = ₹24,000.

Step 3: Calculate Goodwill Goodwill = Super Profit × Number of years' purchase Goodwill = 24,000 × 2 = ₹48,000.

The treatment of goodwill :

The treatment of goodwill during the admission of a partner is handled separately from other assets. According to the sources, there are two primary methods for recording goodwill: the Premium Method and the Valuation Method.

(i) Premium Method : This method is used when a new partner brings their share of goodwill in cash or kind. This goodwill can be retained in the business, withdrawn by old partners, or paid privately.

| No. | Transaction | Journal Entry | Ratio Used |

| 1 | When new partner brings goodwill in cash and it is retained in business. | (a) Cash / Bank A/c ...Dr.

To Goodwill A/c (b) Goodwill A/c ...Dr. To Old Partners’ Capital / Current A/c. |

Sacrifice Ratio |

| 2 | When new partner brings goodwill in cash and it is withdrawn by old partners. | (a) Cash / Bank A/c ...Dr.

To Goodwill A/c (b) Goodwill A/c ...Dr. To Old Partners’ Capital / Current A/c (c) Old Partner’s Capital / Current A/c ..Dr. To Cash / Bank A/c. |

Sacrifice Ratio (for distribution) |

| 3 | When goodwill is paid to old partners privately. | No entry is required in the books of the firm. | N/A |

(ii) Valuation Method : This method is used when the new partner does not bring their share of goodwill in cash. Instead, the goodwill is "raised" in the books of the firm at the time of admission.

| No. | Transaction | Journal Entry | Ratio Used |

| 1 | When goodwill is raised in the books. | Goodwill A/c ...Dr.

To Old Partners’ Capital / Current A/c. |

Old Ratio |

| 2 | When goodwill is raised and then written off. | (a) Goodwill A/c ...Dr.

To Old Partners’ Capital / Current A/c (b) All Partners Capital A/c ...Dr. To Goodwill A/c. |

(a) Old Ratio (b) New Ratio |

Important Notes on Goodwill Treatment :

- Sacrifice Ratio: This ratio (Old Ratio - New Ratio) is specifically used to distribute goodwill among old partners under the Premium Method.

- Existing Goodwill: If goodwill already appears in the Balance Sheet before the new partner is admitted, it is desirable to write it off among the old partners in their old profit-sharing ratio.

- Balance Sheet Appearance: If goodwill is raised and not written off, it will appear on the asset side of the new Balance Sheet. If it is written off, it will not appear in the new Balance Sheet.

Revaluation of Assets and Liabilities :

- Before admitting a new partner, assets and liabilities are revalued.

- This shows the correct and current value of the firm.

- The profit or loss from revaluation is shared only by old partners.

Revaluation Account (Profit and Loss Adjustment A/c) :

- A separate account is opened to record these changes.

- It is called Revaluation A/c or Profit and Loss Adjustment A/c.

- It is a nominal account.

- Expenses and losses are shown on the debit side.

- Incomes and gains are shown on the credit side.

Debit Side of Revaluation A/c :

- Decrease in value of assets.

- Increase in liabilities.

- Outstanding expenses.

- Provision for bad and doubtful debts.

Credit Side of Revaluation A/c :

- Increase in value of assets.

- Decrease in liabilities.

- Income receivable.

- Prepaid expenses.

- Provision for discount on creditors.

Distribution of Profit or Loss : The balance of this account is transferred to old partners. It is shared in their old profit-sharing ratio.

Balance of Revaluation Account :

- Debit balance → shows loss on revaluation.

- Credit balance → shows profit on revaluation.

| Sr.

No. |

Transaction | Journal Entry |

| 1. | Increasing the value of asset and Decreasing the value of liability | Asset A/c.......................................................................................... Dr.

Liability A/c.......................................................................................... Dr. To Revaluation A/c / P & L Adjustment A/c (Being the value of asset increased and value of liability decreased) |

| 2 | Decreasing the value of asset and Increasing the value of liability | Revaluation A/c / P & L Adjustment A/c.......................................................................................... Dr.

To Asset A/c To Liability A/c (Being the value of asset decreased and value of liability increased) |

| 3. | Recording the unrecorded asset in the books of accounts | Asset A/c.......................................................................................... Dr.

To Revaluation A/c (Being, unrecorded asset brought in the books of accounts) |

| 4. | Creating new liability in the books | Revaluation A/c.......................................................................................... Dr.

To New Liability A/c (Being unrecorded liability brought in the books of accounts) |

| 5. | Transfer of Profit on Revaluation to old partner’s Capital/Current A/c | Revaluation A/c.......................................................................................... Dr.

To Old Partner’s Capital/Current A/c (Being profit on revaluation credited to partners’ capital/ current A/c) |

| 6. | Transfer of Loss on Revaluation to old partners’ Capitals/ Current A/c | Old Partners’ Capital/ Current A/c................................................................. Dr.

To Revaluation A/c (Being loss on revaluation transferred to partners’ capital / current A/c) |

Dr. Specimen of Revaluation / Profit & Loss Adjustment Account Cr.

| Particular | Amt (₹) | Paritcular | Amt (₹) |

| To Asset A/c (Decrease-- in Asset) | xxx | By Asset A/c (Increase in Asset) | xxx |

| To Liability (Increase in Liability) | xxx | By Liability (Decrease in Liability) | xxx |

| To Old Partners’ Capital / Current | xxx | By Old Partner’s Capital / Current A/c | |

| A/c (Profit on Revaluation transferred) |

xxx |

(Loss on Revaluation transferred) |

xxx |

Adjustment of Reserves Accumulated Profits and Losses :

(1) Different Types of Reserve Funds :

Every year, a part of profit is kept aside to meet future losses. This is done for unexpected events like fire, flood, theft, or price fall. Such amounts are called reserve funds.

Examples of Reserve Funds :

- General Reserve

- Reserve Fund

- Workmen’s Compensation Fund

- Investment Fluctuation Fund

- Joint Policy Reserve

Nature of Reserve Funds : These reserves are created from past profits. They belong only to the old partners. A new partner has no right over these reserves.

Treatment on Admission of a New Partner :

- Entire reserve balance is transferred to old partners.

- It is distributed in their old profit-sharing ratio.

- The amount is credited to their capital or current accounts.

Reserve funds must be adjusted before admitting a new partner to ensure fairness.

The following journal entry is required to be passed for transfer of balance in various reserves :

Each Reserve A/c (individually) …………………….Dr.

To Old Partners' Capital/Current A/cs (old ratio)

(Being balance in reserve transferred to old Partners' Capital/Current A/cs)

(2) Accumulated Profit / Loss :

Sometimes, profit is not fully distributed among partners. Such undistributed profit is carried forward to the next year. Over time, it becomes accumulated profit.

Treatment in Balance Sheet :

- Accumulated profit is shown on the liabilities side.

- It appears under the heading “Profit and Loss A/c”.

- Similarly, unadjusted losses may also be carried forward.

- These accumulated losses are shown on the assets side.

- They also appear under “Profit and Loss A/c”.

Treatment on Admission of a New Partner :

- Entire accumulated profit or loss is transferred to old partners.

- It is shared in their old profit-sharing ratio.

- The amount is adjusted in their capital or current accounts.

A new partner has no right over past profits or losses, so adjustments are made before admission.

The following entries are required to be passed for transfer of accumulated profit/losses :

(a) Transfer of accumulated profit :

Profit and Loss A/c ……………..………………..Dr.

To Old Partners' Capital/Current A/cs

(old ratio)

(Being accumulated profit transferred to old partners Current/Capital A/cs)

(b) Transfer of accumulated loss :

Old Partners' Capital/Current A/cs ……………..………………..Dr.

To Profit and Loss A/c

(Being accumulated loss transferred to old partners Current/Capital A/cs)

Adjustment of Capitals :

Sometimes capitals of all partners are to be adjusted in the new profit sharing ratio after the admission of new partner. The capitals of the partners may be adjusted in any one of the following ways.

(1) Capitals of old partners may be adjusted on the basis of the capital of the new partner In this case, capital of the new partner is taken as base to find out the total capital. The total capital can be calculated as follows : -

Total Capital = New partner’s capital × Reciprocal of his PSR (Profit sharing ratio)

Example :

‘Z’ is admitted in the firm with 1/5th share of the profits of the firm.

‘Z’ contributes ₹ 50,000 as his capital.

‘X’ and ‘Y’ the other two partners were sharing profits in the ratio of 2:3.

Then the required capital of X and Y should be calculated as follows.:

Calculation of New profit sharing ratio:

X’ s Share of Profits = 2/5 × (1 - 1/5) = 2/5 × 4/5 = 8/ 25

Y’ s Share of Profits = 3/5 × (1 - 1/5) = 3/5 × 4/5 = 12/ 25

Z’ s Share of Profits = 1/5 = 5 / 25

So new ratio is 8:12:5

Calculation of New Capital :

If Z’ Capital / Share is ₹ 50,000,

then the total capital of the firm has to be ₹ 50,000 × 5/1 = ₹ 2,50,000

X’s share should be ₹ 2,50,000 × 8/25 = ₹ 80,000

Y’s share should be ₹ 2,50,000 × 12/25 = ₹ 1,20,000

(2) Capitals of the new partner may be determined on the basis of the total capital of the old partners:

In this case, new partner is required to bring his share of capital in proportion to total capital of old partner’s. It is calculated as follows:

Example :

After making all adjustments as regards goodwill reserve, accumulated profits / loss, revaluation profit / loss etc. the capitals of ‘P’ and ‘Q’ are ₹ 60,000 and ₹ 48,000. The profits and losses are shared by P and Q in the ratio of 3:2 respectively.

R is admitted and is to be given 1/4th share of profits. He has to bring in capital representing his share, which is explained as under.

R gets 1/4th share, so 3/4th share is left for P and Q.

Therefore the combined capital of P and Q is 1,08,000 represents 3/4th share.

Thus total capital should be ₹ 108000 × 4/3 = 1, 44,000.

Therefore R should bring ₹ 36,000 i.e. ₹ 1,44,000 × 1/4

Proportionate capitals of the partners are recorded in capital accounts. The difference is adjusted normally through Cash / Bank / Current / Loan account.

Difference between the actual capital and proportionate capital can be shown by passing following entries.

(1) An entry for surplus capital

Concerned Partner’s Capital A/c ..........................Dr.

To Cash / Bank / Current A/c

(2) An entry for deficit capital

Cash / Bank / Current A/c .....................................Dr.

To Concerned Partner’s Capital A/c

We reply to valid query.