Notes

|

Topics to be Learn :

|

Introduction to Books of Accounts

Books of accounts are divided into two main types.

- The first type is Journal or Subsidiary Books, which are also called books of original entry.

- The second type is Ledger, which is known as the book of final entry.

In the journal, all transactions related to assets, liabilities, expenses, income, cash, or credit are recorded. However, from the journal alone, we cannot find the total balance of any account or know the total income or expenses. To solve this problem, the ledger is used.

Meaning, Definition and Importance of Ledger :

Meaning of Ledger : Ledger is the main book of accounts where all transactions are finally recorded in a classified manner. It is also called the book of final entry. The word “ledger” comes from a Latin word which means “to contain”.

Definition of Ledger : According to S. P. Jain and K. L. Narang, a ledger is a summary of all transactions related to persons, assets, expenses, or incomes over a period of time, showing their overall effect.

Importance of Ledger :

- The ledger keeps records in a proper and systematic way. It gives clear information about assets, liabilities, expenses, income, and other accounts. This helps in managing the business.

- It helps to know how much money is to be received from customers (debtors) and how much is to be paid to suppliers (creditors). This makes planning of payments and collections easier.

- The ledger is useful for preparing the trial balance and final accounts.

- It helps in preparing financial statements, which are useful for businessmen, banks, management, and the government.

- By looking at ledger balances, management can take important decisions like expansion, development, or improvement of the business.

- It helps in controlling and monitoring different expenses of the business.

Contents of Ledger :

A ledger is usually a bound book with many pages. Each page is used for one account. All pages are numbered, and an index is kept at the beginning to easily find any account.

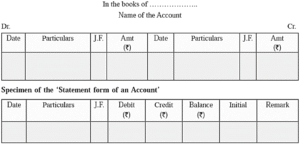

Each side of the ledger (debit and credit) has four columns:

- Date ; This column shows the date of the transaction. The date is written in the order of year, month, and day.

- Particulars : This column shows the name of the related account. On the debit side, the word “To” is used, and on the credit side, the word “By” is used.

- Journal Folio (J.F.) : This column shows the page number of the journal or subsidiary book from where the entry is taken.

- Amount : This column shows the amount of money that is debited or credited in the account.

Specimen of Ledger :

Specimen of the ledger in ‘T’ form is given below:

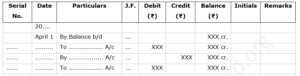

Specimen of ‘Statement form of Account format’ is often used in actual practice, such as in bank passbooks. It presents a running balance after each transaction.

In the books of ........ Statement Account for ........

Posting of Entries to Ledger :

Meaning of Posting : All transactions are first recorded in the Journal or Subsidiary Books. After that, these entries are transferred to the Ledger. This process of transferring entries to the ledger accounts is called posting.

Steps of Recording (Posting Process) :

- (i) Posting from Journal : First, the entries recorded in the journal are taken for posting into the ledger accounts.

- (ii) Open Ledger Accounts : Create separate ledger accounts for each item like cash, sales, purchases, etc., with proper headings.

- (iii) Record Opening Balance : If any account has an opening balance, it should be written first. It is written as “To Balance b/d” (on debit side) or “By Balance b/d” (on credit side).

- (iv) Write the Date : While posting each entry, write the date of the transaction in the date column of the ledger.

- (v) Write Particulars (Account Name) : On the debit side, write the name of the account which is credited in the journal entry. On the credit side, write the name of the account which is debited in the journal entry.

The above process of recording transactions can be studied with the help of following example;

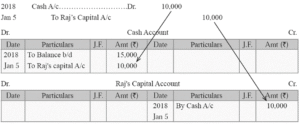

Ex. (1) Posting of simple entry

1) Balance of Cash on 1st January 2018 ₹ 15,000

2) On 5th January 2018 Raj invested ₹ 10,000 in the business.

The Journal Entry for the transaction would be

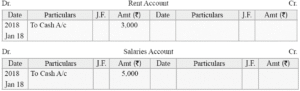

Ex (2) Posting of combined entries :

2018, Jan 18 Paid ₹ 3,000 as Rent and ₹ 5,000 as Salaries.

Combined entry:

Rent A/c………………………………Dr. 3,000

Salaries A/c……………………………Dr. 5,000

To Cash A/c 8,000

Rent A/c and Salaries A/c are debited only with the amount against them in the Journal Entry. Cash A/c is credited with ₹ 8,000 in Journal entry. But since it is on account of two different expenses, both have to be written in the credit side, the total of which is equal to ₹ 8,000

There are total 3 accounts involved in the entry so posting of this entry will be done in 3 ledger accounts.

Posting of entries from Subsidiary Books :

Posting from subsidiary books means transferring summarized totals and individual entries into the correct ledger accounts to keep proper records.

(1) Posting from Cash Book :

- The cash book itself works as both Cash Account and Bank Account.

- Entries written on the debit side of the cash book are posted to the credit side of related accounts.

- Similarly, entries on the credit side of the cash book are posted to the debit side of related accounts like personal, real, or nominal accounts.

(2) Posting from Purchase Book :

- The total purchases of the month are recorded on the debit side of the Purchase Account.

At the same time, each supplier’s account is credited with the amount of goods purchased from them.

(3) Posting from Sales Book :

- The total sales of the month are recorded on the credit side of the Sales Account.

- Each customer’s account is debited with the amount of goods sold to them.

(4) Posting from Purchase Return Book (Return Outward Book) :

- The total purchase returns for the month are recorded on the credit side of the Purchase Return Account.

- Each supplier’s account is debited for the goods returned to them.

(5) Posting from Sales Return Book (Return Inward Book) :

- The total sales returns for the month are recorded on the debit side of the Sales Return Account.

- Each customer’s account is credited for the goods returned by them.

(6) Posting from Journal Proper :

- Entries in the Journal Proper are posted to the ledger accounts in the same way as normal journal entries.

Balancing of Ledger Accounts :

Meaning of Balancing : Balancing a ledger account means finding the difference between the debit side and credit side to know the final amount (balance) of that account. Balancing helps us understand the financial position of the business.

Steps for Balancing Ledger Accounts :

- Find Totals : First, add the amounts on both the debit side and the credit side of the account.

- When Debit Side is Greater : If the total of the debit side is more than the credit side, find the difference. Write this difference on the credit side as “By Balance c/d”.

- When Credit Side is Greater : If the total of the credit side is more than the debit side, find the difference. Write this difference on the debit side as “To Balance c/d”.

- Carry Forward Balance : The balance c/d (carried down) becomes the opening balance for the next period. It is written as “Balance b/d (brought down)” on the opposite side.

Types of Ledger Accounts and Their Balancing :

(i) Personal Accounts : Personal accounts can have a debit balance, credit balance, or zero balance.

- If the balance is debit, the person is called a debtor (they owe money to the business).

- If the balance is credit, the person is called a creditor (the business owes money to them).

(ii) Real Accounts : Real accounts are related to assets and property like cash, building, machinery, etc. These accounts always show a debit balance.

(iii) Nominal Accounts : Nominal accounts include income, expenses, profit, loss, gains, etc. These accounts may have debit or credit balance. At the end, their balances are transferred to the Trading Account or Profit and Loss Account.

Preparation of Trial Balance :

Meaning of Trial Balance : A Trial Balance is a statement that shows the debit and credit balances of all ledger accounts on a particular date.

- A trial balance is a summary of all account balances that helps to check mistakes and prepare final financial statements.

Types of Trial Balance :

- Gross Trial Balance : In this type, the total of debit side and total of credit side of each account are shown separately in the trial balance.

- Net Trial Balance : In this type, only the final balance (either debit or credit) of each account is shown. This method is commonly used in practice.

Methods of Preparing Trial Balance

- Vertical Method (Journal Form) : In this method, accounts are listed in a vertical column with their debit and credit balances.

- Horizontal Method (Ledger Form) : In this method, accounts are shown side by side like a ledger, with debit and credit columns.

Uses (Utilities) of Trial Balance :

- Shows Balances of Accounts : It shows the balances of all ledger accounts in one place.

- Checks Accuracy : It helps to check the arithmetical accuracy of the books of accounts.

- Helps in Preparing Final Accounts : Trial balance is useful for preparing final accounts like Trading Account and Profit & Loss Account based on assets and liabilities.

We reply to valid query.