Notes

|

Topics to be Learn :

|

Introduction :

- Retirement of a partner means a partner leaves the partnership firm and stops working as a partner.

- The partner who leaves the business is called a retiring partner.

- The partners who continue in the business are called continuing partners.

Meaning of Retirement of a Partner :

- A partner may leave the firm because of old age, illness, personal reasons, or business problems.

- After retirement, the retiring partner has no connection with the firm.

- At the time of retirement, the amount payable to the retiring partner is calculated.

This amount is calculated after considering:

- Balance in Capital Account

- Balance in Current Account

- Share of accumulated profits and reserves

- Share of goodwill

- Revaluation profit or loss

- Share of losses, if any

Reasons for Retirement of a Partner :

A partner may retire from the firm due to the following reasons:

- Old age or continuous illness

- Losses in the business

- Loss of interest in the firm

- Desire to start a new business

- Differences of opinion or misunderstanding among partners

Methods of Retirement :

A partner may retire from the firm in the following ways:

- According to the terms of the Partnership Deed

- With the consent of other partners

- By giving written notice of retirement to the other partners

New Ratio :

The ratio in which the continuing partners decide to share the future Profits and Losses is known as New Profit Sharing Ratio.

Examples :

(1) A, B and C are the partners, sharing profits and losses in the ratio of 4 : 3 : 2 respectively. If B retires from the firm due to old age, calculate new ratio of the continuing partners.

Answer :

The new profit sharing ratio of A and C is 4 : 2 i.e. 2 : 1. It is calculated as follows :

Ratio of A, B and C = 4 : 3 : 2

Now cancel out B's ratio i.e. 3 from the above ratio. The remaining ratio is 4 : 2 i.e. 2 : 1 is the new ratio of A and C.

(2) X. Y. and Z share profits and losses equally. Z retires and his share is acquired by X and Y in the ratio of 3:1. Calculate New Profit sharing ratio.

Answer :

Calculation of New Profit Sharing Ratio

Old Ratio = X : Y: Z = 1:1:1

Z’s share is acquired by X and Y in the ratio of 3:1

X’s gain = 1/3 × 3/4 = 3/12

Y’s gain = 1/3 × 1/4 = 1/12

X’s New Share = 1/3 + 3/12 = 7/12

Y’s New Share = 1/3 + 1/12 = 5/12

New Profit Sharing Ratio of X and Y = 7:5

Gain Ratio :

Profit sharing ratio which is acquired by continuing partners on account of retirement or death of a partner is called Gain Ratio. It is generally calculated at the time of retirement or death of a partner.

Gain ratio is calculated by using the following formula :

Gain Ratio = New Ratio - Old Ratio.

Gain ratio is calculated and used to write off the goodwill raised or created to the extent of retiring partner's share only.

Examples :

(1) A, B and C are sharing Profits and Losses in the ratio of 4 : 3 : 2. B retires and A and C share future profits equally. Calculate gain ratio.

Answer :

Gain Ratio = New Ratio - Old Ratio

A’s Gain = 1/2 - 4/9 = 1/18

C’s Gain = 1/2 - 2/9 = 5/18

Gain Ratio of A and C is 1:5

(2) X, Y and Z are sharing Profits and Losses in the ratio of 4 : 3 : 2. Z retires the new ratio of X and Y is 3 : 2. Calculate the gain ratio.

Answer :

X’s Gain = 3/5 - 4/9 = 7/45

Y’s Gain = 2/5 - 3/9 = 3/ 45

Gain Ratio of × and Y is 7:3

(3) P, Q, and R and partners sharing Profits in the ratio of 2 : 2 : 1. Q retired. Calculate the gain ratio.

Answer :

Old Ratio = 2:2:1

New Ratio = 2:1

P’ s gain = 2/3 - 2/5 = 4/15

R’s gain = 1/3 - 1/5 = 2/ 15

Gain Ratio = 4:2 i.e. 2:1

Treatment of Goodwill :

Accounting for goodwill during retirement depends on whether the goodwill is raised for the whole firm or only for the retiring partner, and whether it is retained or written off.

| Transaction | Journal Entry | Balance Sheet Impact |

| Entire firm's goodwill raised and retained | Goodwill A/c …………………………………..(Dr)

to All Partner's Capital A/c (Old Ratio) |

Appears in the new Balance Sheet. |

| Entire firm's goodwill raised and written off | 1. Goodwill A/c ……………………………….(Dr)

to All Partner's Capital A/c (Old Ratio) 2. Continuing Partner's Capital A/c ..(Dr) (New Ratio) to Goodwill A/c |

Does not appear in the new Balance Sheet. |

| Raised to the extent of retiring partner's share and retained | Goodwill A/c …………………………………..(Dr)

to Retiring Partner's Capital A/c |

Appears in the new Balance Sheet to that extent. |

| Raised to the extent of retiring partner's share and written off | 1. Goodwill A/c …………………………….. (Dr)

to Retiring Partner's Capital A/c 2. Continuing Partner's Capital A/c .(Dr) (Gain Ratio) to Goodwill A/c |

Does not appear in the new Balance Sheet. |

| Goodwill already appears in the old Balance Sheet | Difference shown in Profit and Loss Adjustment/Revaluation A/c or Partners' Capital/Current A/c | Depends on the valuation adjustment. |

Transfer of Reserve Fund, General Reserve and Accumulated Profit or Loss :

- At the time of retirement of a partner, the balance of General Reserve and past accumulated profits of the firm are distributed among all partners.

- These amounts are transferred to the partners’ Capital Accounts or Current Accounts in their old profit-sharing ratio.

- Similarly, accumulated losses of the firm are also distributed among all partners in the old profit-sharing ratio.

Adjustment by Continuing Partners :

- Sometimes, the continuing partners may decide to transfer only the retiring partner’s share of reserve or accumulated profit/loss.

- In such a case, only the retiring partner’s Capital Account or Current Account is adjusted.

Purpose of Adjustment :

- These adjustments are made so that the retiring partner gets his correct share of profits, reserves, or losses before leaving the firm.

(1) Transfer of general reserve, accumulated profits, etc. :

General Reserve A/c Dr. xxx

Reserve Fund A/c Dr. xxx

Profit and Loss A/c. Dr. xxx

To All Partners' Capital/Current A/cs

(Being general reserve, accumulated profit transferred)

(2) Transfer of accumulated losses :

All Partners' Capital/Current A/cs Dr. xxx

To Profit and Loss A/c

(Being accumulated losses transferred and debited to all partners' capital/current A/cs in old ratio)

Revaluation of Assets and Re-assessment of Liabilities :

- At the time of retirement of a partner, the firm usually revalues all assets and liabilities.

- This is done to show their correct and current values.

- The changes in values are recorded in the Revaluation Account or Profit and Loss Adjustment Account.

Rules for Revaluation :

- Decrease in the value of assets is debited to the Revaluation Account.

- Increase in liabilities is also debited to the Revaluation Account.

- Increase in the value of assets is credited to the Revaluation Account.

- Decrease in liabilities is also credited to the Revaluation Account.

Distribution of Profit or Loss :

- The profit or loss from revaluation is transferred to all partners’ Capital Accounts or Current Accounts.

- It is shared in their old profit-sharing ratio.

Adjustment of Capitals :

After retirement, the continuing partners may adjust their capitals according to the new profit-sharing ratio.

This adjustment may be made:

- Through Current Accounts

- Through Loan Accounts

- By bringing in or withdrawing cash

Steps for Capital Adjustment :

(i) The total capital of the new firm is decided.

(ii) The capital required from each continuing partner is calculated according to the new profit-sharing ratio.

(iii) The new capital balance is compared with the existing balance in each partner’s Capital Account.

(iv) The surplus or deficit in each partner’s capital is determined.

(v) The surplus or deficit is adjusted by:

- Bringing in cash, or

- Withdrawing cash, or

- Transferring the amount to Current Account or Loan Account according to the partnership deed or agreement.

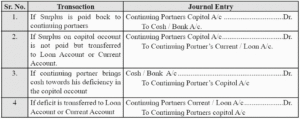

Pro forma Journal entries of adjustment of deficit or surplus :

Ascertainment of Retiring Partner’s Share of Profit on Retirement :

- When a partner retires during the accounting year, it becomes necessary to calculate the profit earned from the date of the last Balance Sheet up to the date of retirement.

- The profit of the current year is usually estimated on:

- The basis of the previous year’s profit, or

- The average profit of past years.

- After estimating the yearly profit, the proportionate profit for the period up to the retirement date is calculated.

- The retiring partner’s share of profit is then determined on the basis of this proportionate profit.

For transfer of such Profit or Loss following journal entries are drafted in the books of the firm.

Transfer of Profit to Retiring Partner’s Capital / Current A/c

Profit and Loss Suspense A/c.................................................Dr.

To Retiring Partner’s Capital /Current A/c. Transfer of

Retiring Partner’s Capital / Current A/c................................Dr.

To Profit and Loss Suspense A/c

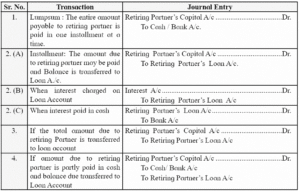

Total payable amount to Retiring Partner :

- The total amount payable to the retiring partner is paid according to:

- The terms of the Partnership Deed, or

- Mutual agreement among the partners.

- The firm may pay:

- The full amount immediately, or

- Only a part of the amount at the time of retirement.

- If any amount remains unpaid, it is transferred to the retiring partner’s Loan Account.

- The balance in the Loan Account is paid later according to the agreement between the partners.

The various types of repayment of retiring partners' dues are explained as follows :

Accounting Steps for Recording Retirement of a Partner

Step 1 : Prepare Necessary Ledger Accounts

- Prepare ledger accounts such as:

- Partners’ Capital Accounts

- Current Accounts

- Revaluation or Profit and Loss Adjustment Account

- Cash/Bank Account

- Goodwill Account, etc.

Step 2 : Transfer Opening Balances

- Transfer the opening balances from the last Balance Sheet to the respective ledger accounts.

Step 3 : Transfer Reserves and Accumulated Profits/Losses

- Transfer balances of:

- General Reserve

- Profit and Loss Account

- Other accumulated profits or losses

- These are transferred to all partners’ Capital or Current Accounts in their old profit-sharing ratio.

Step 4 : Give Treatment to Goodwill

- Pass necessary journal entries for goodwill adjustment among partners.

Step 5 : Revalue Assets and Liabilities

- Revalue assets and liabilities of the firm.

- Transfer the resulting profit or loss to all partners’ Capital or Current Accounts, including the retiring partner, in the old profit-sharing ratio.

Step 6 : Record Payment to Retiring Partner

- Pass journal entry for the amount paid to the retiring partner.

Step 7 : Transfer Unpaid Amount to Loan Account

- If any amount remains unpaid, transfer it from the Retiring Partner’s Capital Account to his Loan Account.

Step 8 : Balance Capital Accounts and Prepare Balance Sheet

- Balance the Capital Accounts of continuing partners.

- Prepare the new Balance Sheet of the firm after the retirement of the partner.

We reply to valid query.