Notes

Question 1. Answer in one sentence.

(1) Who prepares a bank Pass Book?

The bank prepares the bank Pass Book, which is an extract of the account holder's ledger account in the bank's own books.

(2) What is pay-in-slip?

A pay-in-slip is a document filled by an account holder to deposit cash or cheques into their bank account.

(3) What is bank overdraft?

A bank overdraft is a facility provided to current account holders that allows them to withdraw more money than is available in their account.

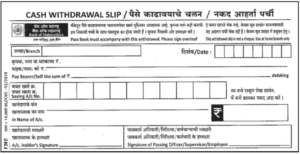

(4) What is withdrawal slip?

A withdrawal slip is a form filled by an account holder to remove funds from their bank account while at the bank.

(5) Who sends the bank statement?

The bank sends the bank statement to provide a summary of financial transactions to the account holder.

(6) What does a debit balance in Cash Book represent?

A debit balance in the Cash Book represents a favourable bank balance, indicating that deposits exceed withdrawals.

(7) Who prepares the Bank Reconciliation Statement?

The businessman or account holder prepares the Bank Reconciliation Statement.

(8) What does debit balance in Pass Book represent?

A debit balance in the Pass Book represents an unfavourable balance or a bank overdraft.

(9) On which side is interest on bank deposit recorded in Pass Book?

Interest on a bank deposit is recorded on the credit side of the Pass Book.

(10) Why is Bank Reconciliation Statement prepared?

The Bank Reconciliation Statement is prepared to detect errors and identify the causes of disagreement between the Cash Book and Pass Book balances.

Question 2. Give one word / term / phrase which can substitute each of the following statement:

(1) The account on which overdraft facility is allowed by bank.

(2) Extract of ledger account of account holder in the books of bank.

(3) Alphanumeric code that facilitates electronic funds transfer in India.

(4) Statement showing the causes of disagreement between balance of Cash Book and Pass Book.

(5) Debit balance in Pass Book.

(6) A form which is filled for depositing cash or cheque into bank.

(7) Left hand side of Pay-in-slip.

(8) Credit balance in Cash Book.

(9) A book maintained by trader to record banking transactions.

(10) Excess of bank deposits over withdrawals by businessman in bank current account.

(1) Current Account: The account on which a bank allows an overdraft facility.

(2) Bank Pass Book: An extract or copy of the account holder's ledger account as it appears in the bank's books.

(3) IFSC (Indian Financial System Code): The alphanumeric code that facilitates electronic funds transfers such as NEFT, RTGS, and IMPS in India.

(4) Bank Reconciliation Statement: A statement prepared to show the causes of disagreement between the balances of the Cash Book and the Pass Book.

(5) Bank Overdraft: A debit balance in the Pass Book, indicating an unfavourable balance where withdrawals exceed deposits.

(6) Pay-in-slip: The form filled out by an account holder when depositing cash or cheques into a bank account.

(7) Counterfoil: The left-hand side of a pay-in-slip that is stamped, signed, and returned to the depositor as an acknowledgement.

(8) Bank Overdraft: A credit balance in the bank column of the Cash Book, representing an unfavourable balance.

(9) Cash Book: The book maintained by a trader or businessman to record all banking transactions in a specific bank column.

(10) Favourable Balance: The condition where bank deposits exceed withdrawals in a current account, also known as a bank balance.

Question 3. Do you agree or disagree with the following statements:

(1) The bank column of Cash Book represents bank account.

Agree.

(2) Bank statement enables account holder to prepare Bank Reconciliation Statement.

Agree.

(3) Cheques issued for payment but not presented to bank appears in Cash Book only.

Agree.

(4) Bank Reconciliation Statement is prepared only during the year end.

Disagree: (While it is often prepared at the end of a month for convenience, a Bank Reconciliation Statement can be prepared on any date.)

(5) Bank Reconciliation Statement is similar to bank statement.

Disagree. (A bank statement is a summary of financial transactions provided by the bank, while a Bank Reconciliation Statement is a separate document prepared to explain the causes of disagreement between the balances of the Cash Book and Pass Book.)

(6) Bank balance as per Cash Book is always equal to bank balance as per Pass Book.

Disagree. (Although they should ideally be the same, in practice, the balances are often different due to time gaps in recording and potential errors.)

(7) Bank advice is sent by the businessman to bank.

Disagree. (A bank advice is a letter sent by the bank to the customer to inform them of specific transactions like dishonoured cheques or debited charges.)

(8) Pay-in-slip is used for depositing cheque into bank.

Agree.

(9) Difference in Cash Book balance and Pass Book balance may arise due to errors committed while recording.

Agree.

(10) Payment and receipt of cash through internet banking generates automatic proof.

Agree.

Question 4. Select the most appropriate alternative from those given and rewrite the following statements:

(1) Overdraft means _______ balance of Cash Book.

(a) closing (b) debit (c) opening (d) credit

(d) credit

(2) When a cheque is deposited and collected by bank Pass Book is _________ .

(a) dishonoured (b) debited (c) credited (d) written.

(c) credited

(3) A __________ is a summary of financial transactions that take place over a period of time on a bank account.

(a) withdrawal slip (b) bank advice

(c) bank statement (d) Pay-in-slip.

(c) bank statement

(4) Debiting an entry in Cash Book ___________ cash balance.

(a) increases (b) decreases (c) nullifies (d) none of the above.

(a) increases

(5) Bank Reconciliation Statement is prepared by _________ .

(a) student (b) businessman (c) bank (d) none of the above.

(b) businessman

(6) Bank balance as per Pass Book means ___________ balance of Pass Book.

(a) credit (b) opening (c) debit (d) closing.

(a) credit

(7) Bank gives overdraft facility to __________ account holder.

(a) savings (b) recurring (c) current (d) fixed.

(c) current

(8) Debit balance as per Cash Book is also known as ___________ balance.

(a) favourable (b) overdraft (c) abnormal (d) unfavourable.

(a) favourable

(9) When extracts of Cash Book and Pass Book are given for uncommon periods, only ________ items are considered for preparation of Bank Reconciliation Statement.

(a) uncommon (b) normal (c) favourable (d) common.

(d) common

(10) When extract of Cash Book and Pass Book are given for common period, only _________ items are considered for preparation of Bank Reconciliation Statement.

(a) uncommon (b) common (c) favourable (d) unfavourable.

(a) uncommon

Question 5. Complete the following statements :

(1) Payments credited in Cash Book are __________ in Pass Book.

Payments credited in the Cash Book are debited in the Pass Book.

(2) While preparing Bank Reconciliation Statement only __________ column of Cash Book is considered.

While preparing a Bank Reconciliation Statement, only the bank column of the Cash Book is considered.

(3) Cheques issued to creditors appear first in ____________ book.

Cheques issued to creditors appear first in the Cash book.

(4) A statement showing the reasons for difference in Cash Book balance and Pass Book balance is known as ___________ .

A statement showing the reasons for the difference in the Cash Book balance and Pass Book balance is known as a Bank Reconciliation Statement.

(5) Overcast on receipt side of Pass Book means _________ in Pass Book balance.

Overcast on the receipt side of the Pass Book means an increase in the Pass Book balance.

(6) Online transfer made to our creditors appear on the _________ side of Cash Book.

Online transfers made to creditors appear on the credit side of the Cash Book.

(7) Interest on overdraft charged by bank is ____________ in Pass Book.

Interest on overdraft charged by the bank is debited in the Pass Book.

(8) Normally the Cash Book shows debit balance and Pass Book shows ________ balance.

Normally the Cash Book shows a debit balance and the Pass Book shows a credit balance.

(9) The form filled for withdrawing cash from bank is known as __________ .

The form filled for withdrawing cash from the bank is known as a withdrawal slip.

(10) A businessman can update his records on receiving __________ .

A businessman can update his records on receiving a bank advice.

Question 6. State whether the following statements are True or False with reasons :

(1) Cheques deposited into bank but not yet cleared appears in the Pass Book only.

False. (When a businessman deposits a cheque, he immediately records it on the debit side of his Cash Book; the bank only records it in the Pass Book once the amount is actually collected.)

(2) Direct deposit made by debtors into businessman's bank account is recorded on the credit side of Pass Book.

True.

(3) Businessman can prepare Bank Reconciliation statement only with Cash Book Balance.

False. (A Bank Reconciliation Statement can be prepared using either the Cash Book balance or the Pass Book balance as the starting point.)

(4) When overdraft as per Cash Book is given, bank charges debited in Pass Book only, is to be added.

True.

(5) Bank Statement is sent by Bank to businessman.

True.

Question 7. Draft the following specimen with imaginary Name, Account number, Amount.

(1) Bank Statement

A bank statement is a summary of financial transactions over a given period.

(2) Pay-in-slip

This document is used to deposit cash or cheques into a bank account.

(3) Withdrawal slip

This form is used by the account holder to remove funds while physically at the bank.

(4) Bank Advice

A letter sent by the bank to inform the customer about specific debits or credits, such as automated payments.

(5) Pass Book

The Pass Book is a copy of the account holder's ledger as it appears in the bank's books.

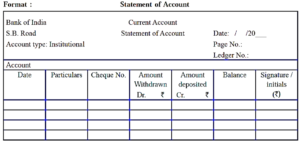

| A/c Holder: Mr. Aryan Sharma | A/c No.: 12345678901 | IFSC: MAHB0001234 |

| Date | Particulars | Cheque No. | Amount Withdrawn

Dr. (₹) |

Amount Deposited

Cr. (₹) |

Balance

(₹) |

Initials |

| 01/05/23 | Balance b/d | — | — | — | 50,000 | — |

| 10/05/23 | By Cash | — | — | 5,000 | 55,000 | (B.M.) |

| 15/05/23 | To Withdrawal | — | 2,000 | — | 53,000 | (B.M.) |

Question 8. Correct and rewrite the following statements.

(1) The form filled for depositing cash or cheque into bank is known as Pass Book.

The form filled for depositing cash or cheque into bank is known as a Pay-in-slip.

(The Pass Book is actually a copy of the account holder's ledger account in the bank's books).

(2) Bank Reconciliation Statement is prepared by Bank.

Bank Reconciliation Statement is prepared by the businessman.

(It is prepared by the account holder, while the bank provides the bank statement or Pass Book).

(3) Debit balance as per Pass Book is known as favourable balance.

Debit balance as per Pass Book is known as an unfavourable balance (or bank overdraft).

(A credit balance in the Pass Book represents a favourable balance).

(4) When a cheque is deposited into Bank it is credited in Cash Book.

When a cheque is deposited into the Bank it is debited in the Cash Book.

(Deposits are recorded on the debit or receipt side of the Cash Book).

(5) When extracts are given for common period only common items are to be considered.

When extracts are given for a common period only uncommon items are to be considered.

(Common items appearing in both books are ignored because they do not create a difference in the balances).

Question 9. Complete the following table.

| Reasons | When Normal balance as per Cash Book is given Add/Less | When Normal balance as per Pass Book is given Add/Less | |

| (1) | Interest debited in Pass Book only. | ||

| (2) | Direct deposit made by customer in bank recorded in Pass Book | (+) | |

| (3) | Cheque deposited into bank but not yet collected by bank | ||

| (4) | Cheque deposited into bank is dishonoured | (+) | |

| (5) | Cheque issued but not presented for payment. | (-) |

| Reasons | When Normal balance as per Cash Book is given Add/Less | When Normal balance as per Pass Book is given Add/Less |

| 1) Interest debited in Pass Book only. | Less (-) | Add (+) |

| 2) Direct deposit made by customer in bank recorded in Pass Book | (+) | Less (-) |

| 3) Cheque deposited into bank but not yet collected by bank | Less (-) | Add (+) |

| 4) Cheque deposited into bank is dishonoured | Less (-) | (+) |

| 5) Cheque issued but not presented for payment. | Add (+) | (-) |

We reply to valid query.