Notes

|

Topics to be Learn :

|

Meaning, Importance and Utilities of Accounting Documents :

Introduction :

Accounting documents contain all the basic details of a financial transaction. They show:

- The amount of the transaction

- The person to whom the payment was made

- The purpose of the transaction

- The date of the transaction

These documents are important in bookkeeping because they provide proof that a financial transaction has taken place.

Today, internet banking and mobile banking generate instant records of payments and receipts. However, many people still visit banks personally for transactions. Therefore, bank documents such as cheques, drafts, and deposit slips continue to be important.

Types of Bank Documents :

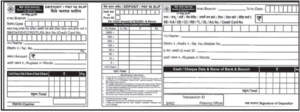

(1) Pay-in-Slip (Deposit Slip) : A pay-in-slip, also called a deposit slip, is used when an account holder deposits cash or a cheque into a bank account.

When depositing cash, the account holder fills in:

- Account number

- Date of deposit

- Details of the cash deposited

When depositing a cheque, the account holder fills in:

- Account number

- Details of the cheque

- Name of the drawee bank

- Amount of the cheque

A pay-in-slip has two parts:

- The right-hand side is kept by the bank for its records.

- The left-hand side, called the counterfoil, is stamped, signed, and dated by the bank officer and returned to the account holder as an acknowledgement.

Importance and Utilities :

- It helps the account holder deposit cash or cheques into the bank account.

- Entries of cash or cheque deposits are recorded in the books of accounts based on the pay-in-slip.

- The counterfoil or acknowledgement serves as legal proof of the deposit.

Contents: (same contents appear on the left hand side and right hand side of the pay-in-slip)

- (i) Name of Bank, branch and address.

- (ii) Date of transaction.

- (iii) Amount deposited in figures and words. (Cash/cheque)

- (iv) Name of account holder.

- (v) Account Number.

- (vi) Type of account.

- (vii) Details of denomination, i.e. number of ₹ 100, ₹ 200, ₹500, notes etc. deposited.

- (viii) Details of cheque.

- (ix) Details of drawee bank.

- (x) PAN card number if the amount of deposit is more than ₹ 50,000.

Format : Pay-in-slip

| Tip: In modern banking, a cheque with a duly filled pay-in-slip can be dropped into the bank's drop box for collection. |

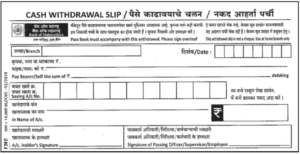

(2) Withdrawal Slip : A form filled for withdrawing money from a bank account.

Importance :

- Used only within the bank to withdraw money.

- Account holder's signature is matched against the bank's specimen signature to prevent fraud.

- A copy is not available to the account holder for recording in books; it only reflects in the Pass Book.

Key Contents :

- Name of bank, branch, date

- Account holder's name, account number and type

- Amount in figures and words

- Signature of account holder

- PAN card photocopy required if withdrawal exceeds ₹50,000

Format :

| Note: A cheque can also be used by the account holder to withdraw cash from the bank. |

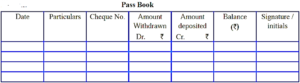

(3) Bank Pass Book : A copy/extract of the ledger account of the account holder as maintained in the books of the bank.

Importance :

- Shows balance of an account on any particular date.

- Acts as documentary evidence that can be produced in court.

- Confirms all transactions routed through the bank.

Key Contents :

- Bank name, branch, address, telephone number

- Account holder's full name, address, photo

- Account type, number, and customer ID

- IFSC Code (Indian Financial System Code) — alphanumeric code for IMPS, NEFT, RTGS

- Columns: Date, Particulars, Cheque No., Amount Withdrawn (Dr.), Amount Deposited (Cr.), Balance, Signature

Format :

| Historical Fact: Pass Books appeared in the 18th century, giving customers their own transaction records for the first time. Today, bank statements can be viewed online. |

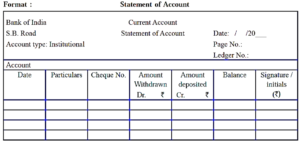

(4) Bank Statement : A summary of financial transactions over a given period on a bank account, issued by the bank to current account holders.

Importance :

- Enables the account holder to know bank balance.

- Helps in planning timely payments.

- Provides information on cheque clearance time.

- Essential for preparing the Bank Reconciliation Statement.

Key Contents :

- Bank and branch details, date, particulars, Cheque number, withdrawals, deposits, balance

| Modern banking: Bank statements are now available as electronic statements — viewable, downloadable, and printable online — reducing paper and postage costs. |

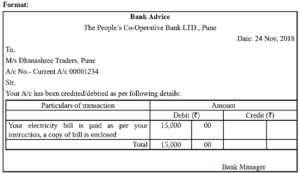

(5) Bank Advice : A letter sent by the bank to the account holder informing them of specific banking transactions.

When is Bank Advice issued?

- Dishonour of cheques deposited for collection

- Bank charges debited to account

- Dishonour of Bills Receivable discounted

- Bills sent for collection

- Interest charged or allowed by bank

- Dividend or interest collected by bank

- Any payment made by bank per standing instruction

Importance :

- Helps the businessman update records from time to time.

- Creates evidence for transactions made through bank.

| Today's Practice: SMS alerts and app notifications have largely replaced Bank Advice for routine transactions. |

Electronic Fund Transfer — Quick Reference

| Method | Full Form | Key Feature |

| IMPS | Immediate Payment Service | Instant, 24×7, any amount |

| NEFT | National Electronic Funds Transfer | Small transfers (< ₹2 Lakhs) |

| RTGS | Real Time Gross Settlement | Large transfers (> ₹2 Lakhs) |

Meaning, Definition, Need and Importance of Bank Reconciliation Statement. :

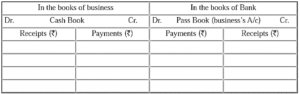

Meaning : A businessman records all banking transactions in the bank column of his Cash Book. The bank records the same in the account holder's ledger, which forms the Pass Book. Ideally, the balances in both should match (with opposite signs — Debit in Cash Book = Credit in Pass Book).

However, in practice, the balances often differ. A Bank Reconciliation Statement explains and reconciles these differences.

| Key Relationship: • Deposit recorded in Cash Book (Dr. side) → Recorded in Pass Book (Cr. side) • Payment recorded in Cash Book (Cr. side) → Recorded in Pass Book (Dr. side) |

Definitions : "A statement which reconciles the Bank balance as per Cash Book and the balance as per Pass Book, showing all causes of difference between the two."

"A statement showing the causes of disagreement between the balance shown by the bank Pass Book and the balance shown by the Cash Book under the bank column at the end of a specific period or month."

Need and Importance of BRS :

- Explains and clarifies causes of disagreement between Cash Book and Pass Book balances.

- Helps detect errors and omissions in both books.

- Reduces chances of fraud by staff dealing in cash.

- Helps verify that the bank makes proper entries for all transactions.

- Acts as a moral check on business staff to keep the Cash Book up to date.

- Serves as an important mechanism of internal control, tracking cash inflow and outflow.

Reasons for difference between Cash Book balance and Pass Book balance :

The common reasons for the difference between the balance as per cash book (bank) column and corresponding pass book balance are as shown below :

Two Main Categories :

| I. Time Difference | II. Errors & Omissions |

| In Cash Book but NOT in Pass Book:

• Cheque issued but not presented for payment • Cheque deposited but not yet collected/cleared In Pass Book but NOT in Cash Book: • Interest credited by bank • Direct collection on behalf of customer • Direct payment by bank (ECS, standing instructions) • Bank charges, interest on overdraft, commission • Dishonour of cheques or Bills of Exchange • Amount directly deposited by debtor in bank |

Committed by businessman or bank:

• Entry recorded on wrong side • Recording wrong amount • Wrong balancing or totalling (overcast / undercast) • Double recording (entry made twice) • Omission (entry not recorded at all) |

Detailed Explanation of Each Cause :

(A) Cheque Issued but Not Presented : When a cheque is issued, it is immediately credited in the Cash Book. But the bank records it only when the cheque is physically presented. Until then, the Pass Book shows a HIGHER balance than the Cash Book.

(B) Cheque Deposited but Not Cleared : When cheques are received and deposited, they are debited in the Cash Book immediately. But the bank only credits them after clearing. Until then, the Cash Book shows a HIGHER balance than the Pass Book.

(C) Interest Credited by Bank : Bank credits interest to the customer's account and it appears in the Pass Book. The businessman records it in the Cash Book only after receiving intimation. Until then, the Pass Book balance is HIGHER.

(D) Direct Collection on Behalf of Customer : Bank collects interest, dividend, rent etc. as per standing instructions and credits the Pass Book. This appears in the Cash Book only after the customer receives intimation — until then, Pass Book balance is HIGHER.

(E) Direct Payment by Bank : Bank pays insurance premiums, electricity bills, loan instalments etc. per standing instructions. The Pass Book is debited immediately. The Cash Book is updated only after intimation — until then, Cash Book balance is HIGHER.

(F) Bank Charges, Overdraft Interest, Commission : Bank debits these charges periodically to the customer's account. The businessman comes to know only on reviewing the Pass Book. Until then, Cash Book balance is HIGHER than Pass Book.

(G) Dishonour of Cheque or Bill of Exchange : When a cheque or bill discounted with the bank is dishonoured, the bank debits the Pass Book immediately. The Cash Book is updated only after intimation — creating a difference.

(H) Direct Deposit by Debtor : Debtors sometimes deposit money directly into the bank account. The bank credits the Pass Book, but the businessman is unaware until the bank statement arrives — Pass Book balance is HIGHER than Cash Book.

Specimen of Bank Reconciliation statement :

| Particulars | Amount (₹) | Amount (₹) |

| Bank Balance / Overdraft as per Cash Book / Pass Book | XXX | |

| Add: Reasons which INCREASE the balance of the other book | ||

| 1. _______________ | xxx | |

| 2. _______________ | xxx | xxx |

| Less: Reasons which DECREASE the balance of the other book | ||

| 1. _______________ | xxx | |

| 2. _______________ | xxx | xxx |

| Bank Balance / Overdraft as per Pass Book / Cash Book | XXX |

| Remember: When you start with Cash Book balance, you arrive at Pass Book balance — and vice versa. The answer with a negative sign means OVERDRAFT. |

Preparation of Bank Reconciliation Statement (BRS) :

Procedure for Finding the Causes of Difference and Their Effects :

When there is a difference between the balances shown in the Cash Book and the Pass Book, the following steps are followed to find the reasons:

(1) Compare Deposits : Compare the entries on the debit side of the Cash Book with the entries on the credit side (deposit column) of the Pass Book. Put a tick (✓) against the entries that appear in both books.

(2) Compare Withdrawals : Compare the entries on the credit side of the Cash Book with the entries on the debit side (withdrawal column) of the Pass Book. Put a tick (✓) against the matching entries.

(3) List Unticked Items : Prepare a list of all the entries that remain unticked in either book. These entries are the reasons for the difference between the balances of the Cash Book and the Pass Book.

(4) Analyse the Causes : Examine the unticked items and identify the reasons for the difference in balances.

(5) Select the Date : Choose a date for preparing the Bank Reconciliation Statement. It is usually prepared on the last day of the month because the balances of both the Cash Book and Pass Book are easily available on that date.

(6) Start Preparing the BRS : Begin the Bank Reconciliation Statement with either:

- Balance as per Cash Book, or

- Balance as per Pass Book

(7) Adjust the Balance :

- Add or subtract the unticked items to the starting balance.

- If the Cash Book balance is taken as the starting point, adjust it according to the entries appearing in the Pass Book.

- If the Pass Book balance is taken as the starting point, adjust it according to the entries appearing in the Cash Book.

This process helps reconcile the balances shown by the Cash Book and the Pass Book.

(8) Apply the rule of plus and minus.

(a) When balance as per Cash Book is given

- Add credits in Cash Book or in Pass Book.

- Less debits in Cash Book or in Pass Book.

(b) When balance as per Pass Book is given

- Add debits in Cash Book or in Pass Book.

- Less credits in Cash Book or in Pass Book.

(c) When overdraft as per Cash Book is given

- Add debits in Cash Book or in Pass Book.

- Less credits in Cash Book or in Pass Book.

(d) When overdraft as per Pass Book is given

- Add credits in Cash Book or in Pass Book.

- Less debits in Cash Book or in Pass Book.

| Reason | Cash Book Dr. Bal (+) | Pass Book Cr. Bal (+) | Overdraft Cash Book (−) | Overdraft Pass Book (−) |

| Cheque deposited but NOT collected by bank | − | + | + | − |

| Cheque issued but NOT presented for payment | + | − | − | + |

| Bank charges debited in Pass Book only | − | + | + | − |

| Interest credited in Pass Book only | + | − | − | + |

| Interest debited in Pass Book only | − | + | + | − |

| Direct payment by bank (Pass Book only) | − | + | + | − |

| Direct deposit by customer in bank (Pass Book only) | + | − | − | + |

| Bill discounted — dishonoured (Pass Book only) | − | + | + | − |

| Cheque deposited — dishonoured (not in Cash Book) | − | + | + | − |

The Golden Rule — Simplified :

| Starting Balance Type | Rule |

| Cash Book Dr. Balance (Favourable) | Add: Credits in CB or PB

Less: Debits in CB or PB |

| Pass Book Cr. Balance (Favourable) | Add: Debits in CB or PB

Less: Credits in CB or PB |

| Cash Book Cr. Balance (Overdraft) | Add: Debits in CB or PB

Less: Credits in CB or PB |

| Pass Book Dr. Balance (Overdraft) | Add: Credits in CB or PB

Less: Debits in CB or PB |

Pro forma of Cash Book with bank column:

Dr. Cr.

| Particulars | Amount. (₹) |

Particulars | Amount (₹) |

| (1) Balance as per cash book | XXX | (1) Overdraft as per cash book | XXX |

| (2) Cheques/Cash deposited | XXX | (2) Cheques issued | XXX |

| (3) Dividend or interest collected by the bank | XXX | (3) Insurance premium or electricity charges paid by the bank |

XXX |

| (4) Any other income collected by the bank | XXX | (4) Any other expenses paid by the bank | XXX |

| (5) Transfer of amount from Fixed Deposit A/c or Savings A/c to Current A/c | XXX | (5) Transfer of amount from Current A/c to Fixed Deposit A/c or Savings A/c |

XXX |

| (6) Undercast of debit side of cash book or overcast of credit side of cash book | XXX | (6) Undercast of credit side of cash book or overcast of debit side of cash book | XXX |

| (7) Cheques issued and dishonoured | XXX | (7) Cheques deposited and dishonoured | XXX |

| XXXX | XXXX |

Pro forma of Pass Book :

Dr. Cr.

| Particulars | Amount. (₹) |

Particulars | Amount (₹) |

| (1) Overdraft as per pass book | XXX | (1) Balance as per pass book | XXX |

| (2) Cheques issued | XXX | (2) Cheques/Cash deposited | XXX |

| (3) Insurance premium or electricity charges paid by the bank | XXX | (3) Dividend or Interest collected by the bank | XXX |

| (4) Any other expenses paid by the bank | XXX | (4) Any other income collected by the bank | XXX |

| (5) Transfer of amount from Current A/c to Fixed Deposit A/c or Savings A/c | XXX | (5) Transfer of amount from Fixed Deposit A/c or Saving A/c to Current A/c |

XXX |

| (6) Undercast of credit side of cash book or overcast of debit side of cash book | XXX | (6) Undercast of debit side of cash book or overcast of credit side of cash book | XXX |

| (7) Cheques deposited and dishonoured | XXX | (7) Cheques issued and dishonoured. | XXX |

| XXXX | XXXX |

When Cash Book and Pass Book Extracts are for the Same Period :

When the extracts of the Cash Book and Pass Book relate to the same period (usually the same month), consider:

- The opening balances of the Cash Book and Pass Book.

- The uncommon (unticked) items.

Meaning of Uncommon Items :

- Compare the entries in both books and put a tick (✓) against matching entries.

Match:

- Debit side of the Pass Book with the Credit side of the Cash Book.

- Credit side of the Pass Book with the Debit side of the Cash Book.

- The common (ticked) items do not cause any difference and are therefore ignored.

- The unticked items are called uncommon items.

- These uncommon items are the reasons for the difference between the balances of the Cash Book and Pass Book and must be added or subtracted in the Bank Reconciliation Statement.

When Cash Book and Pass Book Extracts are for Different Periods

When the extracts of the Cash Book and Pass Book relate to different periods (usually consecutive months):

- Consider only the common items.

- These common items create differences between the balances shown in the Cash Book and Pass Book.

- Therefore, they need to be adjusted while preparing the Bank Reconciliation Statement.

Key Point :

- Same period → Consider uncommon (unticked) items.

- Different periods → Consider common items.

Note : In the Bank Reconciliation Statement, when we start with the cash book balance, we arrive at balance as per pass book and vice versa.

Reconciliation of Debtors and Creditors : Just as a Bank Reconciliation Statement is prepared to reconcile differences between the Cash Book and Pass Book, reconciliation statements can also be prepared for debtors (customers) and creditors (suppliers/vendors).

In this process, the Debtor's or Creditor's ledger in our books is compared with our account as recorded in the Debtor's or Creditor's books. Any differences found are identified and reconciled.

Procedure

- Obtain the Ledger Account : Request the debtor or creditor to provide a copy of our account as it appears in their books.

- Compare the Entries : Compare the entries in:

- Our ledger account, and

- The ledger account maintained by the debtor or creditor.

- Match the Entries : Tick (✓) the entries that appear in both accounts.

- Identify Differences : Prepare a list of entries that do not match in the two accounts.

- Prepare a Reconciliation Statement : Use the unmatched entries to prepare a reconciliation statement and identify the reasons for the differences.

Importance :

- Helps identify errors and omissions in accounting records.

- Ensures the accuracy of debtor and creditor balances.

- Helps maintain correct records with customers and suppliers.

- Assists in resolving disputes regarding payments and balances.

Key Point :

- Debtor Reconciliation compares our records with the customer's records.

- Creditor Reconciliation compares our records with the supplier's records.

- Any unmatched entries are analyzed and adjusted through a reconciliation statement.

Special Situations — How to Treat Them :

| Special Case | Treatment |

| Common period extracts given | Consider UNCOMMON items only (common items already match) |

| Different period extracts given | Consider COMMON items only (these appear in both books) |

| Overcast on debit/receipt side | Means balance is overstated — REDUCE the balance |

| Undercast on debit/receipt side | Means balance is understated — ADD to the balance |

| Overcast on credit/payment side | Means balance is understated — ADD to balance |

| Undercast on credit/payment side | Means balance is overstated — REDUCE balance |

| Wrong amount recorded (less than actual) | Add the difference to arrive at correct balance |

| Wrong amount recorded (more than actual) | Subtract the difference |

| Entry recorded twice (double entry) | Subtract the extra amount once |

| Entry recorded in cash column instead of bank column | Not recorded in bank column → may not affect BRS |

We reply to valid query.