Solutions Part-2

| Part -1 - Theoretical Questions

Part - 2 - Practical Problems |

Practical Problems

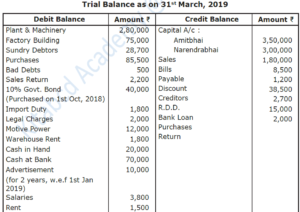

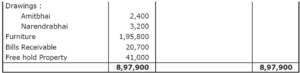

(1) Amitbhai and Narendrabhai are in Partnership Sharing Profits and Losses equally. From the following Trial Balance and Adjustments given below, you are required to prepare Trading and Profit and Loss Account for the year ended 31st March, 2019 and Balance Sheet as on that date.

Trial Balance as on 31st March, 2019

Adjustments :

- Stock on hand on 31st March 2019 was valued at ₹ 43,000.

- Uninsured Goods worth ₹ 8,000 were

- Create D.D at 2% on Sundry debtors.

- Patil, our customer become insolvent and could not pay his debts of ` 500.

- Outstanding Expenses - Rent ₹ 800 and Salaries ₹ 300

- Depreciate Factory Building by ` 2,500 and Furniture by ₹ 1,800

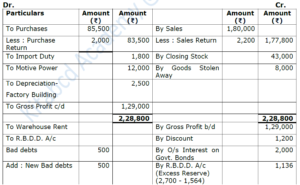

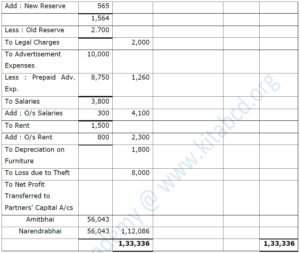

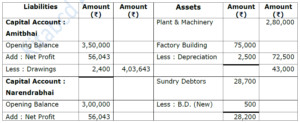

In the books of Amitbhai and Narendrabhai

Trading and Profit and Loss Account for the year ended on 31st March, 2019

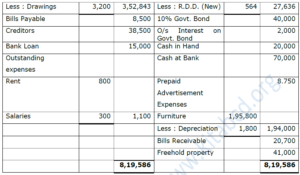

Balance Sheet as on 31st March, 2019

Notes :

(1) Import duty, Motive power and Depreciation on Factory Building are recorded on the Debit side of Trading A/c.

(2) 10% Govt. bond is an investment. It was purchased on 1-10-2018.

∴ Interest is calculated for six months. [i.e. from 01-10-2018 to 31-03-2019]

Interest on Govt. Bond = 40,000 x \(\frac{6}{12}\) × \(\frac{10}{100}\) = ₹2,000

(3) Advertisement Expenses paid for 2 years from 01-01-2019. Up to 31-3-2019, 3 months Advertisement Expenses is calculated and written off to Profit and Loss A/c. It is calculated as below :

10,000 x \(\frac{3}{24}\) = ₹ 1,250

∴ Prepaid Advertisement Expenses = 10,000 - 1,250 = ₹ 8,750

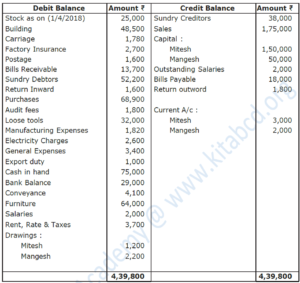

(2) From the following Trial Balance of M/S Mitesh and Mangesh, you are required to prepare Trading and Profit and Loss Account for the year ended 31st March, 2019 and Balance Sheet as on that date.

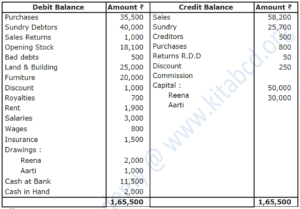

Trial Balance as on 31st March, 2019

Adjustments :

- Mitesh and Mangesh are sharing Profit and losses in the ratio 3:1.

- Partners are entitled to get Commission @ 1% each on Gross

- The closing stock is valued at ₹ 23,700.

- Outstanding Expenses - Audit fees ₹ 400; carriage ₹

- Building is valued at ₹ 46,500.

- Furniture is depreciated by 5%.

- Provide Interest on Partner's capital at 5% pa.

- Goods of ₹ 900 were taken by Mangesh for his personal

- Write off ₹ 1,000 as Bad Debts and maintain D.D at 3% on Sundry Debtors.

In the books of M/S Mitesh and Mangesh

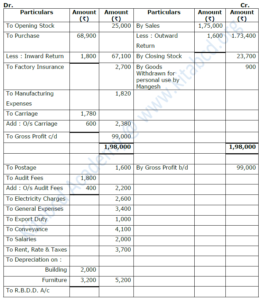

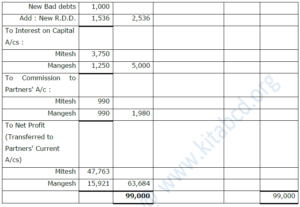

Trading and Profit and Loss Account for the year ended on 31st March, 2019

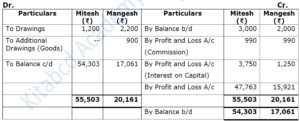

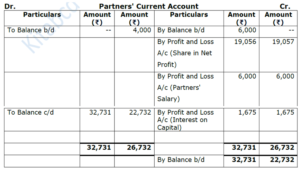

Partner's Current A/cs

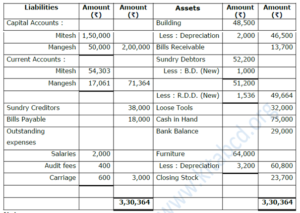

Balance Sheet as on 31st March, 2019

Notes :

Notes :

(1) In this question,

- The balances of the Current Accounts are already given. So, the total fixed capital is directly shown on the Liabilities side of the Balance Sheet.

- The adjustments like commission to partners, interest on capital, and goods withdrawn by Mangesh are recorded in the Current Accounts.

- The closing credit balances of the Current Accounts are shown separately on the Liabilities side of the Balance Sheet.

(2) Building is valued at ₹ 46,500 whereas opening balance of Building given is ₹ 48,500. Therefore, difference of amount of ₹ 2,000 (48,500 - 46,500) is nothing but Depreciation charged on Building.

(3) Return Inward = Sales Return

Return Outward = Purchase Return

(4) Commission payable to partners :

Mitesh = 1% on Gross Profit = \(\frac{1}{100}\) x 99,000 = 990

Mangesh = 1% on Gross Profit = \(\frac{1}{100}\) x 99,000 = 990

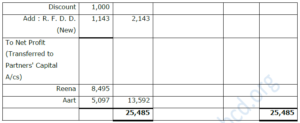

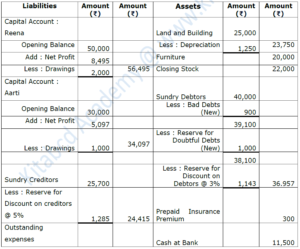

(3) From the following Trial Balance and adjustments given below of Reena and Aarti, you are required to prepare Trading and Profit and Loss Account for the year ended 31st March, 2019 and Balance Sheet as on that date.

Trial Balance as on 31st March, 2019

Adjustments :

- Closing Stock valued at ₹ 22,000.

- Write off ₹ 900 for Bad & doubtful debts and create a provision for Reserve for doubtful debts

₹ 1,000.

- Create a provision for Discount on Debtors @ 3% and creditors @ 5%.

- Outstanding Expenses - Wages ₹ 700 and Salaries ₹

- Insurance is paid for 15 months, e.f. 1st April 2018

- Depreciate Land and Building @ 5%

- Reena & Aarti are Sharing Profits & Losses in their Capital

In the books of Reena and Aarti

Trading and Profit and Loss Account for the year ended on 31st March, 2019

Balance Sheet as on 31st March, 2019

Notes :

(1) Insurance premium ₹ 1,500 is paid for 15 months. i.e. prepaid insurance premium for 3 months = ₹ 300.

(2) Reserve for Discount on Debtors = 3% on [Debtors - New Bad debts - New Reserve)

= \(\frac{3}{100}\) x (40,000 – 900 - 1,000) = \(\frac{3}{100}\) x 38,100 = ₹ 1,143

(3) Reserve for Discount on Creditors = 5% on (Value of Creditors) x 25,700 = ₹ 1,285

(4) Profit and Loss ratio = Capital ratio = 50,000 : 30,000 = 5:3

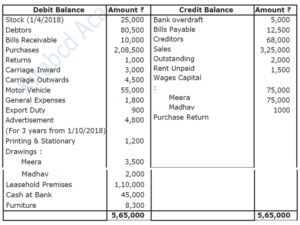

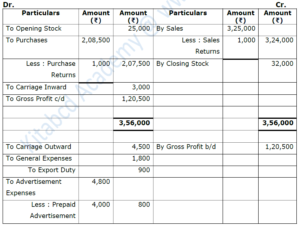

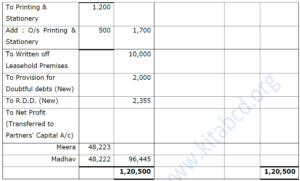

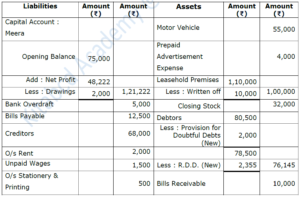

(4) From the following Trial Balance of M/S Meera and Madhav. Prepare Trading and Profit and Loss Account for the year ended 31st March, 2019 and Balance Sheet as on that date.

Trial Balance as on 31st March, 2019

Adjustments :

- Closing Stock is valued at ₹ 32,000.

- Provide Provision for Doubtful Debts ₹ 2,000.

- Create reserve for Discount on Debtors @ 3%.

- Valued of Leasehold Premises on 31st March 2019 ₹ 1,00,000.

- Out standing Expenses Printing & Stationary ₹

In the books of M/S Meera and Madhav

Trading and Profit and Loss Account for the year ended on 31st March, 2019

Balance Sheet as on 31st March, 2019 :

Notes :

Notes :

(1) Advertisement expenses written off to Profit and Loss account during the year 2018-19 for six months i.e. from 1/10/18 to 31/03/19.

Advertisement expenses written off = (Advertisement bill paid) x \(\frac{1}{3}\) x \(\frac{6}{12}\)

= 4,800 x \(\frac{1}{3}\) x \(\frac{6}{12}\) = ₹ 800

Prepaid Advertisement = 4,800 – 800 = ₹ 4,000.

(2) Reserve for Discount on Debtors = 3% (Balance in debtors)

= \(\frac{3}{100}\) × (80,500 - 2,000) = \(\frac{3}{100}\) x 78,500 = ₹ 2,355.

(3) Difference of opening balance (₹ 1,10,000) and closing balance (₹ 1,00,000) for leasehold premises is to be considered as written off on leasehold premises.

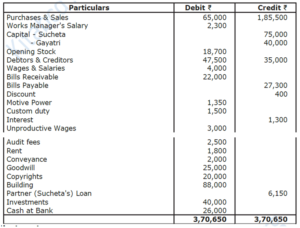

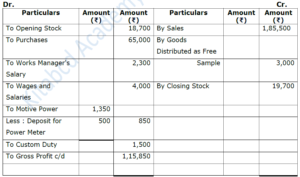

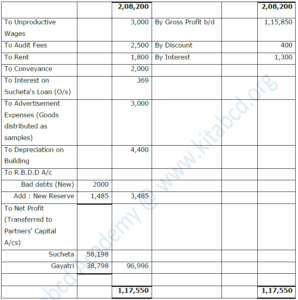

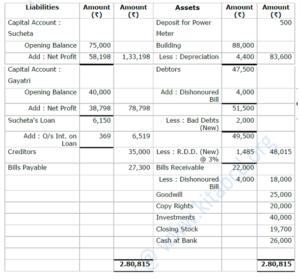

(5) Sucheta & Gayatri are Partners sharing Profit and Losses in the ratio 3:2. From the following Trial Balance and additional information you are required to prepare Trading and Profit and Loss Account for the year year ended 31st March 2019 and Balance Sheet as on that date.

Trial Balance as on 31st March, 2019

Adjustments :

- Stock on 31st March 2019 was valued at ₹ 19,700.

- Goods costing ₹ 3,000 distributed as free

- Motive Power includes ₹ 500 paid for deposit of Power

- Depreciate Building @ 5%.

- Write of ₹ 2,000 for Bad debts and maintain D.D at 3% on Debtors.

- Bills Receivable included dishonoured of Bill of ₹ 4,000.

In the books of Sucheta & Gayatri

Trading and Profit and Loss Account for the year ended on 31st March, 2019

Balance Sheet as on 31st March, 2019

Notes :

(1) Rate of interest on partner's loan is not mentioned, therefore interest on loan is calculated at 6% p.a.

∴ Interest on Sucheta's Loan = 6,150 x 1 x \(\frac{6}{100}\) = ₹ 69.

(2) Add dishonoured bill amount to debtors amount and then calculate B.D. and R.D.D.

(3) Subtract dishonoured bill amount from Bills Receivable amount.

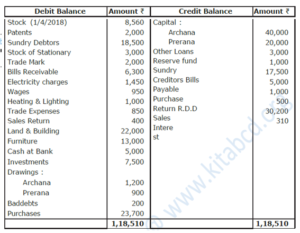

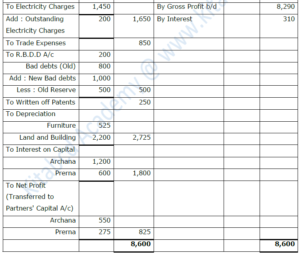

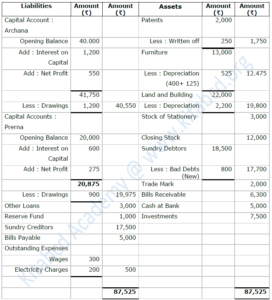

(6) Archana and Prerana are partners, sharing Profits and Losses in the ratio 2:1 with the help of following Trial Balance and Adjustments given below. You are required to prepare Trading and Profit and Loss Account for the year ended 31st March 2019 and Balance Sheet as on that date.

Trial Balance as on 31st March, 2019

Adjustments :

- Stock on 31st March 2019 is valued at Cost Price ₹ 12,000 and Markct Price ` 17,000.

- Our customer Shekhar failed to pay his dues of ` 800.

- 1/8th of Patents are to be written

- A part of Furniture ₹ 5,000 is purchased on 1st Oct

- Depreciation on Land & Building 10% and on Furniture 5%.

- Outstanding Expenses Wages ₹ 300 and Electricity Charges ₹

- Allow Interest on Capital 3%.

In the books of Archana and Prerana

Trading and Profit and Loss Account for the year ended on 31st March, 2019

Balance Sheet as on 31st March, 2019:

Notes :

(1) Stationery stock is an asset.

(2) Depreciation on furniture :

13,000 = 8,000 (Op. Bal.) + 5,000 (Pur. on 01/10/18)

8,000 x \(\frac{5}{100}\) (Depr. for full year) = ₹ 400

5,000 x \(\frac{6}{12}\) x \(\frac{3}{100}\) (Depr. for six months) = ₹ 125

∴ Total depr. = 400 + 125 = ₹525

(3) \(\frac{1}{8}\)th patents to be written off = 2,000 x \(\frac{1}{8}\) = ₹ 250.

(4) As no other expenses are given, Trade Expense is recorded in Profit and Loss Account.

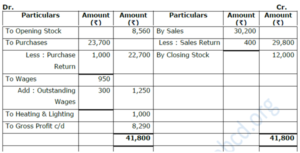

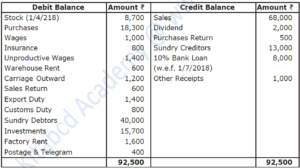

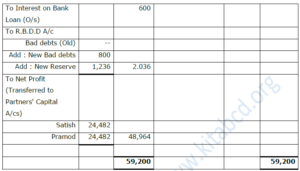

(7) Satish and Pramod are Partners. Prepare Trading Account and Profit and Loss Account for the year 31st March, 2019. You have to find out Gross Profit and Net Profit only.

Trial Balance as on 31st March, 2019

Adjustments :

- The Closing Stock is valued at ₹ 15,400.

- Outstanding Wages ₹

- Create provision for Bad debts ₹ 800 and maintain D.D 3% on Sundry Debtors.

- Goods of ₹ 1,800 distributed as a free

- Goods of ₹ 2,000 were sold and delivered on 31st March 2019 but no entry is passed in the Books of Account.

In the books of Satish and Pramod

Trading and Profit and Loss Account for the year ended on 31st March, 2019

Notes :

(1) Here only gross profit and net profit is to be find out. Therefore, Balance Sheet is not prepared.

(2) Interest on 10% bank loan is calculated for 9 months (From 1/7/2018 to 31/3/2019)

I = \(\frac{PRN}{100}\) = 8,000 × \(\frac{10}{100}\) x \(\frac{9}{12}\) = ₹600

(3) Goods distributed as free samples is an advertisement expense for business.

(4)

Sundry Debtors ₹ 40,000

Add : Unrecorded Sales ₹ 2,000

Less : Provision for Bad Debts (New) ₹ 800

Total 41,200

Less : R.D.D. (New) (3% of 41,200) ₹ 1,236

₹ 39,964

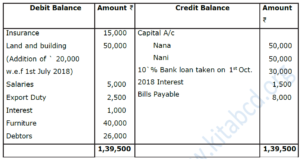

(8) Nana and Nani are Partners in Partnership Firm sharing Profits and Losses equally. You are required to give effects of Adjustments in Profit & Loss A/c and Balance Sheet with the help of following information.

Trial Balance as on 31st March, 2019

Adjustments :

- Gross profit amounted to ₹ 34,500.

- Insurance Paid for 15 months e.f. 1.4.2018.

- Depreciate Land and Building at 10% a. and Furniture at 5% p.a.

- Write off ₹ 1,000 for Bad Debts and maintain D.D at 5% on Sundry Debtors.

- Closing Stock is valued at ₹ 34,500.

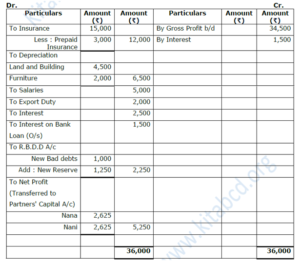

In the books of Nana and Nani

Trading and Profit and Loss Account for the year ended on 31st March, 2019

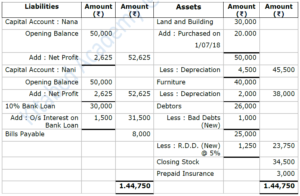

Balance Sheet as on 31st March, 2019

Balance Sheet as on 31st March, 2019

Notes :

(1) Here, Profit and Loss Account and Balance Sheet are to be prepared. Therefore, Trading Account is not prepared. Gross profit (given) is recorded on Credit side of Profit and Loss Account.

(2) Land and Building

(i) 30,000 (Op. Bal.)

Depr. = 30.000 × \(\frac{10}{100}\) = ₹ 3.000

(For whole year)

(ii) 20,000 (Add on 1/7/2018)

Depr. = 20.000 × \(\frac{10}{100}\) × \(\frac{9}{12}\) = ₹ 1,500

(For nine months)

(3) Interest on 10% bank loan is calculated for 6 months. (From 1/10/2018 to 31/3/2019)

I = \(\frac{PRN}{100}\) = 30.000 × \(\frac{10}{100}\) × \(\frac{6}{12}\) = ₹ 1,500

(4) Prepaid insurance = \(\frac{3}{15}\) x (Insurance Amount) = \(\frac{3}{15}\) x 15,000 = ₹ 3,000

(5) RDD = 5% on (Debtors-New Bad debts)

= \(\frac{5}{100}\) x (26,000 - 1,000)

= \(\frac{5}{100}\) x 25,000 = ₹ 1,250

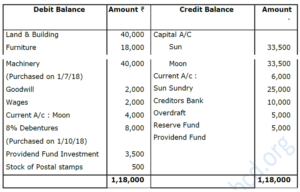

(9) Sun and Moon are Partners in Partnership Firm sharing Profits and Losses equally. You are required to give effects of Adjustments with the help of following information.

Trial Balance as on 31st March, 2019

Adjustments :

- Partners are entitled to get salary ₹ 6,000 a. in addition to their profit & loss sharing.

- Depreciation on Land & Building, Furniture & Machinery @ 10%, 5% and 3%

- Interest on Capital 5% a.

- Closing Stock ₹ 60,743.

- Wages included ₹ 1,000 as advance given to

- Interest due but not paid ₹

- Total Net Profit amounted to ₹ 38,113.

In the books of Sun and Moon

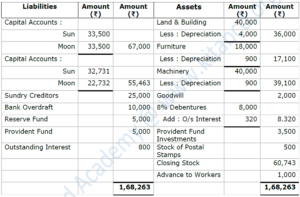

Balance Sheet as on 31st March, 2019 :

Balance Sheet as on 31st March, 2019 :

Notes :

(1) Depreciation on machinery is calculated for 9 months. (i.e. from 1/7/18 to 31/3/19)

Depreciation = 40,000 x \(\frac{3}{100}\) x \(\frac{9}{12}\) = ₹900

(2) Interest on 8% debentures, calculated for 6 months, (i.e. from 1/10/18 to 31/3/19)

I = \(\frac{PRN}{100}\) = 8,000 x \(\frac{8}{100}\) x \(\frac{6}{12}\) = ₹320

(3) Advance given to workers (by firm) ₹ 1,000 is an asset for firm, so, it is shown on Assets side.

(4) Interest due but not paid is a liability for firm, so, it is shown on Liabilities side.

(10) Kshipra and Manisha are Partners sharing Profit and Losses in their Capital Ratio. You are required to prepare Trading Account and Profit and Loss Account for the year ended 31st March, 2019 and Balance Sheet as on that date.

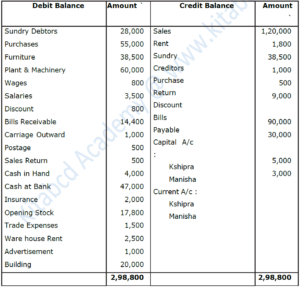

Trial Balance as on 31st March, 2019

Adjustments :

- Stock on 31st March 2019 was at ₹ 37,000.

- Sales includes, sale of machinery of ` 2,000, which is sold on 1st April

- Depreciation on fixed assets @ 5%.

- Each Partners is entitled to get Commission at 1% of Gross Profit and Interest on Capital 5% a.

- Outstanding Expenses Wages ₹ 200 & Salaries ₹

- Create provision for doubtful debts @ 3% on Sundry

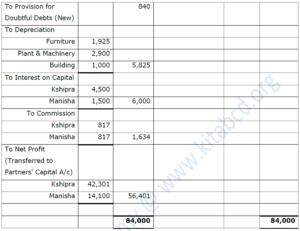

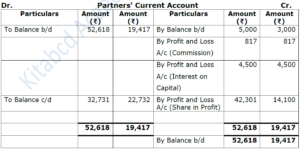

In the books of Kshipra and Manisha

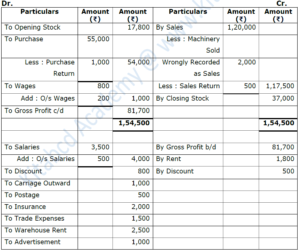

Trading and Profit and Loss Account for the year ended on 31st March, 2019

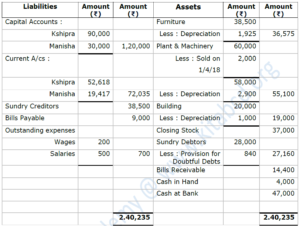

Balance Sheet as on 31st March, 2019

Notes :

(1) Depreciation on fixed assets means depreciation on Furniture, Plant and Machinery and Building.

(2) Sales includes sale of Machinery of ₹ 2,000 is substracted from sales and from Plant and Machinery. On balance amount of Plant and Machinery ₹ 58,000, calculate 5% depreciation i.e. 60,000 - 2,000 = ₹ 58,000 × 5% = ₹2,900.

(3) Here, on gross profit calculate 1% commission for partners and record it to Profit and Loss A/c and in Current A/cs. Commission payable to each partner = \(\frac{1}{100}\) x Gross profit = \(\frac{1}{100}\) x 81,700 = ₹ 817.

We reply to valid query.