Solutions Part-1

Question 1. Objective Questions :

(A) Select the most appropriate alternatives from the following & rewrite the sentences :

(1) When there is no partnership agreement between partners, the division of Profits take place in ..................... ratio.

(a) Equal

(b) capital ratio

(c) initial contribution

(d) experience and tenrue of partners.

When there is no partnership agreement between partners, the division of Profits take place in Equal ratio.

(2) To find out Net Profit or Net Loss of the business ..................... account is prepared.

(a) Trading

(b) Capital

(c) Current

(d) Profit & Loss

To find out Net Profit or Net Loss of the business Profit & Loss account is prepared.

(3) A ..................... is an Intangible Asset.

(a) Goodwill

(b) Stock

(c) Cash

(d) Furniture

A Goodwill is an Intangible Asset.

(4) In the absence of an agreement, interest on loan advanced by the partner to the firm is allowed at the rate of .....................

(a) 5%

(b) 6%

(c) 10%

(d) 9%

In the absence of an agreement, interest on loan advanced by the partner to the firm is allowed at the rate of 6%

(5) Liability of partners in a partnership business is ..................... .

(a) Limited

(b) Unlimited

(c) Limited and Unlimited

(d) None of the above

Liability of partners in a partnership business is Unlimited

(6) The Indian Partnership act is in force since .....................

(a) 1932

(b) 1881

(c) 1956

(d) 1984

The Indian Partnership act is in force since 1932

(7) Maximum number of Partners in a firm are ..................... according to Companies Act 2013.

(a) 10

(b) 25

(c) 20

(d) 50

Maximum number of Partners in a firm are 50 according to Companies Act 2013.

(B) Write the word/phrase/term, which can substitute each of the following sentences.

(1) Persons who form the partnership firm.

Partners

(2) Amount of cash or goods withdrawn by partners from the business from time to time.

Drawings

(3) An association of two or more persons according to Indian partnership Act 1932.

Partnership firm

(4) Act under which partnership firms are regulated.

Indian Partnership Act, 1932

(5) Process of entering the name of partnership firm in the register of Registrar.

Registration

(6) Partnership agreement in written form.

Partnership Deed

(7) Under this method capital balances of partners remains constant.

Fixed Capital Method

(8) Proportion in which partners share profits.

Profit Sharing Ratio

(9) Such capital method in which only capital account is maintained for each partner.

Fluctuating Capital Method

(10) The account to which all adjustment are made when capital is fixed.

Current Account

(11) Expenses which are paid before they are due.

Prepaid expenses

(12) The accounts that are prepared at the end of each accounting year.

Final Accounts

(13) An asset which can be converted into cash easily.

Current Assets or Liquid Assets

(14) Order in which fixed assets are recorded first in Balance sheet.

Order of liquidation

(15) The account in which selling expenses of business are recorded.

Profit and Loss Account

(16) Debit balance of Trading Account.

Gross loss

(17) Credit balance of profit & loss account.

Net profit

(C) State whether the following statements are True of False with reasons :

(1) Partnership firm is a Non Trading Concern.

Statement is False

Reason:

- A Partnership firm is generally a profit-oriented business organization formed by two or more persons who agree to share profits and losses. It carries out trading, manufacturing, or service activities to earn profit.

- A Non-Trading Concern, on the other hand, is an organization like a club, charity, or society that is formed not for earning profit but for social, cultural, or charitable purposes.

- Since a partnership firm is established to earn profit, it is not a Non-Trading Concern.

(2) Profit and Loss Account is a Real Account.

Statement is False

Reason:

A Profit and Loss Account is a Nominal Account, not a Real Account.

- Real Accounts relate to assets (like Cash, Building, Furniture).

- Nominal Accounts relate to expenses, losses, incomes, and gains.

The Profit and Loss Account records expenses and incomes to determine the net profit or loss of a business. Since it deals with expenses and incomes, it is classified as a Nominal Account.

(3) Carriage Inward is carriage on purchases.

Statement is True

Reason:

- Carriage Inward refers to the transportation charges paid for bringing goods purchased to the business premises. It is directly related to the purchase of goods and is therefore treated as a direct expense.

- It is added to the cost of purchases and shown on the debit side of the Trading Account.

(4) Adjustments are recorded in Partners Current Account in Fixed Capital Method.

Statement is True

Reason:

Under the Fixed Capital Method, the partners’ capital accounts remain unchanged (fixed) except when additional capital is introduced or capital is withdrawn permanently.

All other adjustments such as:

- Interest on Capital

- Interest on Drawings

- Salary or Commission to Partners

- Share of Profit or Loss

are recorded in the Partners’ Current Account, not in the Capital Account.

Therefore, the statement is True.

(5) Prepaid expenses are treated as liabilities.

Statement is False

Reason:

- Prepaid expenses are amounts paid in advance for expenses that relate to the next accounting period (for example, prepaid rent or prepaid insurance).

- They are considered an asset, not a liability, because they represent a future benefit to the business.

- Prepaid expenses are shown on the Assets side of the Balance Sheet

(6) If Partnership Deed is silent partners share profits and losses in proportion to their capital.

Statement is False

Reason:

According to the Indian Partnership Act, 1932, if the Partnership Deed does not specify the profit-sharing ratio, the partners will share profits and losses equally, regardless of the amount of capital contributed by each partner.

Therefore, the statement is False.

(7) Balance sheet is an Account.

Statement is False

Reason:

A Balance Sheet is not an account. It is a statement that shows the financial position of a business on a particular date.

It lists:

- Assets

- Liabilities

- Capital

Unlike other accounts (like Cash Account or Profit and Loss Account), the Balance Sheet does not follow the debit and credit rule. Therefore, it is a financial statement, not an account.

(8) Wages paid for installation of Machinery is a Revenue expenditure.

Statement is False

Reason:

Wages paid for the installation of machinery are considered a Capital Expenditure, not a Revenue Expenditure.

This is because:

- The expense is incurred to bring the machinery into working condition.

- It increases the value of the asset.

- It provides long-term benefit to the business.

Therefore, such wages are added to the cost of machinery and shown on the Assets side of the Balance Sheet, not treated as a normal expense in the Profit and Loss Account.

(9) Income received in advance is a liability.

Statement is True

Reason:

- Income received in advance means money has been received for services or goods that are yet to be provided. Since the business still has an obligation to deliver the service or goods in the future, it is considered a liability.

- It is shown on the Liabilities side of the Balance Sheet as it represents an amount owed by the business in terms of future service or performance.

(10) R.D.D is created on creditors.

Statement is False

Reason:

- D.D (Reserve for Doubtful Debts) is created on debtors, not on creditors.

- It is made to cover the possible loss that may arise if some debtors fail to pay the amount due to the business. Since debtors are assets, R.D.D is created as a provision against debtors.

- Creditors are liabilities, so no R.D.D is created on them.

(11) Depreciation is not calculated on Current Assets.

Statement is True

Reason:

- Depreciation is charged only on Fixed Assets like machinery, building, furniture, etc., because these assets are used for a long period and lose value due to wear and tear.

- Current Assets (such as cash, stock, debtors, prepaid expenses) are short-term assets that are expected to be converted into cash within one year. They do not suffer wear and tear in the same way as fixed assets.

- Therefore, depreciation is not calculated on Current Assets.

(12) Goodwill is an intangible asset.

Statement is True

Reason:

- Goodwill is an intangible asset because it cannot be seen or touched, but it has value.

- It represents the reputation, customer loyalty, brand name, and other advantages of a business that help it earn higher profits.

- Since it has value but no physical form, it is classified as an intangible asset and shown on the Assets side of the Balance Sheet.

(13) Indirect expenses are debited to Trading Account.

Statement is False

Reason:

- Indirect expenses (such as office salary, rent, insurance, advertising, etc.) are not directly related to the purchase or production of goods.

- They are debited to the Profit and Loss Account, not the Trading Account.

- The Trading Account includes only direct expenses (like wages, carriage inward, etc.) that are directly connected with buying or producing goods.

(14) Bank Loan is a current liability.

Statement is False

Reason:

- A Bank Loan is usually a Long-Term Liability because it is taken for more than one year.

- However, if the loan is repayable within one year, then it is treated as a Current Liability.

- So, in general accounting terms, a bank loan is considered a Long-Term Liability, unless specifically stated otherwise.

(15) Net profit is debit balance of Profit & Loss Account.

Statement is False

Reason:

In the Profit and Loss Account:

- If expenses exceed incomes, there is a debit balance, which means net loss.

- If incomes exceed expenses, there is a credit balance, which means net profit.

Therefore, net profit is a credit balance, not a debit balance.

(D) Find odd one

(1) Wages, Salary, Royalty, Import Duty.

Odd One: Salary

Reason:

- Wages, Royalty, and Import Duty are generally treated as direct expenses when they are related to production or purchase of goods. These are debited to the Trading Account.

- Salary (office salary) is usually an indirect expense and is debited to the Profit and Loss Account.

Therefore, Salary is the odd one out.

(2) Postage, Stationery Advertising, Purchases.

Odd One: Purchases

Reason:

- Postage, Stationery, and Advertising are indirect expenses and are debited to the Profit and Loss Account.

- Purchases is a direct expense related to buying goods for resale and is debited to the Trading Account.

Therefore, Purchases is the odd one out.

(3) Capital, Bills Receivable, Reseve Fund, Bank overdraft

Odd One: Bills Receivable

Reason:

- Capital, Reserve Fund, and Bank Overdraft are shown on the Liabilities side of the Balance Sheet.

- Capital → Owner’s liability

- Reserve Fund → Internal liability

- Bank Overdraft → Current liability

- Bills Receivable is an Asset and is shown on the Assets side of the Balance Sheet.

Therefore, Bills Receivable is the odd one out.

(4) Building, Machinery, Furniture, Bills payable.

Odd One: Bills Payable

Reason:

- Building, Machinery, and Furniture are Fixed Assets and are shown on the Assets side of the Balance Sheet.

- Bills Payable is a Liability and is shown on the Liabilities side of the Balance Sheet.

Therefore, Bills Payable is the odd one out.

(5) Discount received, Dividend received, Interest received, Depreciation.

Odd One: Depreciation

Reason:

- Discount Received, Dividend Received, and Interest Received are incomes and are credited to the Profit and Loss Account.

- Depreciation is an expense and is debited to the Profit and Loss Account.

Therefore, Depreciation is the odd one out.

(E) Complete the Sentences

(1) Partners share profit & losses in .................... ratio in the absence of partnership deed.

Partners share profit & losses in equal ratio in the absence of partnership deed.

(2) Registration of Partnership is .................... in India.

Registration of Partnership is optional in India.

(3) Partnership business must be ....................

Partnership business must be lawful

(4) Liabilities of Partners in Partnership firm is ....................

Liabilities of Partners in Partnership firm is unlimited

(5) The balance of Drawings Account of a partner is transferred to his .................... account under the Fixed Capital Method.

The balance of Drawings Account of a partner is transferred to his Current account under the Fixed Capital Method.

(6) The interest on capital of a partner is debited to .................... account.

The interest on capital of a partner is debited to Profit and Loss account.

(7) Partners are .................... liable for the debts of the firm.

Partners are joint and several liable for the debts of the firm.

(8) Partnership Deed is an .................... of Partnership.

Partnership Deed is an Article of Partnership.

(9) The withdrawal by partner for personal use from the firm is .................... to his account.

The withdrawal by partner for personal use from the firm is debited to his account.

(10) Commission payable to partner is .................... to the firm.

Commission payable to partner is liability/outstanding expense to the firm.

(11) When partners adopt Fixed Capital Method then they have to operate ......................... Account.

When partners adopt Fixed Capital Method then they have to operate Partner's Current Account.

(12) If partners Current Account shows .................... balance it is shown to the liability side of Balance sheet.

If partners Current Account shows credit balance it is shown to the liability side of Balance sheet.

(13) The expenses paid for trading purpose are known as .................... expenses.

The expenses paid for trading purpose are known as trade expenses.

(14) Cash receipts which are recurring in nature are called as .................... Receipts.

Cash receipts which are recurring in nature are called as Revenue Receipts.

(15) Return outward are deducted from ....................

Return outward are deducted from purchases

(16) Expenses which are paid before due date are called as ....................

Expenses which are paid before due date are called as Prepaid Expenses

(17) Assets which are held in the business for a long period are called ....................

Assets which are held in the business for a long period are called Fixed Assets

(18) Trading Account is prepared on the basis of is .................... expenses.

Answer :

Trading Account is prepared on the basis of is direct expenses.

[/spoiler](19) When commission is allowed to any partner, it is .................... of the business.

When commission is allowed to any partner, it is expenditure of the business.

(20) When goods are distributed as free samples, it is treated as .................... of the business.

When goods are distributed as free samples, it is treated as advertisement expense of the business.

(F) Answer in one sentence only :

(1) What is fluctuating capital?

Fluctuating capital is a method of maintaining partners’ capital accounts in which the capital balance changes every year due to profit, loss, drawings, interest, salary, etc.

(2) Why is Partnership Deed necessary?

A Partnership Deed is necessary to clearly define the rights, duties, profit-sharing ratio, and responsibilities of partners, so as to avoid misunderstandings and disputes in future.

(3) If the Partnership Deed is silent, in which ratio the partners will share the profit or loss?

If the Partnership Deed is silent, the partners will share the profit or loss equally, as per the provisions of the Indian Partnership Act, 1932.

(4) What is the Fixed Capital Method?

The Fixed Capital Method is a method of maintaining partners’ accounts in which the capital of each partner remains fixed and all adjustments like interest, salary, drawings, and share of profit or loss are recorded in a separate Current Account.

(5) How many partners are required to form a Partnership Firm?

A minimum of two partners are required to form a Partnership Firm.

(6) What is Partnership Deed?

A Partnership Deed is a written agreement between partners that states the terms and conditions of the partnership, including profit-sharing ratio, duties, rights, and responsibilities of each partner.

(7) What are the objectives of the Partnership firm?

The main objective of a Partnership firm is to carry on a lawful business and earn profit, which is shared among the partners according to the agreed ratio.

(8) What rate of interest is allowed on partner's loan in the absence of an agreement?

In the absence of an agreement, interest on partner’s loan is allowed at the rate of 6% per annum, as per the Indian Partnership Act, 1932.

(9) What is the minimum number of Partners in a Partnership firm according to Indian Partneship Act, 1932.

According to the Indian Partnership Act, 1932, the minimum number of partners required to form a Partnership Firm is two.

(10) What is liability of a partner?

The liability of a partner is unlimited, meaning each partner is personally responsible for the debts and obligations of the firm, even to the extent of using their personal assets if necessary.

(11) In the absence of Partnership Deed what is the rate of interest on loan advanced by partner to the firm is allowed?

In the absence of a Partnership Deed, interest on a loan advanced by a partner to the firm is allowed at 6% per annum, as per the Indian Partnership Act, 1932.

(12) What do you mean by pre-received income?

Pre-received income (or income received in advance) means the amount received for goods or services that are yet to be provided, and it is treated as a liability until the service is rendered.

(13) What is the effect of the adjustment of provision for discount on debtors in the final accounts of partnership?

The adjustment of Provision for Discount on Debtors reduces the value of debtors in the Balance Sheet and the amount of provision created or adjusted is debited or credited to the Profit and Loss Account accordingly.

(14) When is partners Current Account opened ?

Partners’ Current Account is opened when the firm follows the Fixed Capital Method, to record adjustments like interest, salary, drawings, and share of profit or loss separately from the capital account.

(15) As per which principle of accounting closing stock is valued at cost price or at market price whichever is less?

Closing stock is valued at cost price or market price, whichever is less according to the Principle of Conservatism (Prudence) in accounting.

(16) What is the provision of Indian Partnership Act with regard to Interest on capital ?

According to the Indian Partnership Act, 1932, in the absence of an agreement, no interest on capital is allowed to partners.

(17) Why is Balance Sheet prepared?

A Balance Sheet is prepared to show the financial position of a business on a particular date by presenting its assets, liabilities, and capital.

(18) Why wages paid for installation of Machinery are not shown in Trading Account?

Wages paid for installation of machinery are not shown in the Trading Account because they are a capital expenditure (added to the cost of the machinery) and not a direct expense related to the purchase or production of goods.

(19) What do you mean by indirect incomes?

Indirect incomes are incomes that are not earned from the main business activities but arise from other sources, such as discount received, interest received, or commission received, and they are credited to the Profit and Loss Account.

(20) Why partners capital is treated as long term liability of business?

Partners’ capital is treated as a long-term liability because it represents the amount owed by the business to the partners and is generally invested for a long period, not repayable in the ordinary course of business.

(G) Do you agree/disagree with the following statements.

(1) When Partnership Deed is silent, Partners share profits of the firm according to capital ratio.

Disagree

(2) Current account always shows a debit balance.

Disagree

(3) It is compulsory to have a partnership agreement in writing.

Disagree

(4) Partnership Firm is a trading concern.

Agree

(5) An interest on capital is an expenditure for the partnership firm.

Agree

(6) Partnership is an association of two or more persons.

Agree

(7) Partners are entitled to get Salary or Commission.

Disagree

(8) The balance of Capital Account remains constant under Fixed Capital Method.

Agree

(9) The Indian Partnership Act, came into existence in the year 1945.

Disagree

(10) Profit and Loss Account reflects the true Financial position.

Disagree

(11) Amount borrowed by partner from his business will be debited to Current Account.

Agree

(12) Sold but undispatched goods must be part of valuation of closing stock.

Disagree

(13) Carriage Inward is a selling and distribution overhead

Disagree

(14) Gross profit is an operation profit

Disagree

(15) All financial expenditures are debited to profit and loss account.

Agree

(16) Free distribution of goods is debited to trading account.

Disagree

(H) Calculate the following:

(1) Undervaluation of Closing Stock by 10%. Closing Stock was ₹ 30,000 find out the value of Closing Stock

Undervaluation of closing stock by 10%

Revised value = \(\frac{\text{Book Value}}{\text{100 - %of undervaluation}}×100\) = \(\frac{3000}{100-10}\) x 100 = ₹ 33,333.

∴ Value of closing stock = ₹ 33,333.

(2) Calculate 12.5% P. A. depreciation on Furniture -

(a) on ₹ 220,000 for 1 year

(b) on ₹ 10,000 for 6 months

Depreciation=Amount of asset x Period x %

(a) Depreciation on furniture = 2,20,000x1 x = ₹ 27,500

∴ Deprecation on furniture for 1 year = ₹ 27,500

(b) Depreciation on furniture = 10,000 x \(\frac{6}{12}\) x \(\frac{12.5}{100}\) = ₹ 625

∴ Depreciation on furniture for 6 months = ₹ 625

(3) Insurance Premium is paid for the year ending 1st September 2019 Amounted to ₹ 1,500. Calculate prepaid insurance assuming that the year ending is 31st March 2019.

Insurance period: 1st September 2018 to 1st September 2019 (1 year)

Accounting year ends: 31st March 2019

Prepaid period = 1st April 2019 to 1st September 2019 = 5 months

Premium paid for 12 months = ₹1,500

Prepaid Insurance = ₹1,500 ×\(\frac{5}{12}\) = ₹625

Prepaid Insurance = ₹625

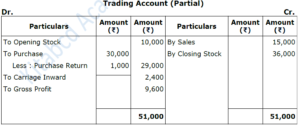

(4) Find out Gross profit / Gross Loss Purchases ₹ 30,000, Sales ₹ 15,000, Carriage Inward ₹2,400, Opening Stock ₹ 10,000, Purchase Returns ₹1,000, Closing Stock ₹ 36,000.

(5) Borrowed Loan from Bank of Maharashtra ₹ 2,00,000 on 1st October 2019 at rate of 15% p.a. Calculate Interest on Bank Loan for the year 2019-20 assuming that the financial year ends on 31st March, every year.

Loan borrowed = ₹ 2,00,000

Rate of interest = 15% P.a.

Duration = 1st October 2019 to 31st March 2020 i.e. 6 Month

Interest amount = Loan amount x Rate of interest x Duration

= 2,00,000 × \(\frac{15}{100}\) x \(\frac{6}{12}\) = ₹ 15,000

We reply to valid query.