Notes

|

Topics to be Learn :

Additional Information :

Important Terms :

|

Introduction and Meaning of Not for Profit Concerns :

Types of Organisations :

In society, there are two types of organisations: Trading organisations and Non-trading organisations.

Trading Organisation (Profit-making) :

- The main aim of a trading organisation is to earn maximum profit.

- It earns profit by manufacturing goods or buying and selling goods.

- It may also earn income by providing services to customers.

- Trading organisations prepare Trading Account, Profit and Loss Account, and Balance Sheet.

- These accounts help to find the profit or loss of the business.

- They also show the financial position of the business.

- Examples include sole proprietorship, partnership firms, companies, and co-operative organisations.

Non-Trading Organisation (Not-for-profit) :

- The main aim of a non-trading organisation is not to earn profit.

- It works to provide services to its members or society.

- Examples include sports clubs, charitable hospitals, schools, colleges, professional institutions, and religious concerns.

- These organisations prepare a Receipts and Payments Account to record cash transactions.

- They prepare an Income and Expenditure Account to check whether income is enough to meet expenses.

- They also prepare a Balance Sheet to know their financial position on a particular date.

Meaning of Not for Profit Concerns:

- A Not for Profit concern is an entity started to give qualitative service at minimum charges.

- Their primary focus is promoting social welfare, art, culture, and education.

- Instead of trading, they collect income through subscriptions, admission fees, donations, and government grants.

Features of Not-for-Profit Organisation :

- The main objective of a not-for-profit organisation is to provide services without earning profit in areas like education, health, sports, charity, art, and culture.

- A not-for-profit organisation does not pay any dividend to its members.

- Any person interested can become a member by paying entrance fees, life membership fees, or subscriptions.

- The organisation is managed in a democratic way by elected members. These members form a managing committee and choose office bearers like chairman, secretary, and treasurer.

- The organisation prepares an Income and Expenditure Account to record income and expenses and to find out surplus or deficit.

- Every not-for-profit organisation has a capital fund, which includes entrance fees, donations, legacies, and surplus. The excess of assets over liabilities is also called capital fund.

- The organisation may create special funds like prize fund or building fund from specific donations or grants received for a particular purpose.

Distinction Between Profit and Not for Profit Organizations :

| Point of Distinction | Profit Organization | Not for Profit Organization |

| Meaning | These engage in trading or manufacturing activities with the primary objective of earning profit | These aim to provide services to members or the public. |

| Primary Objective | To earn profit. | To provide service. |

| Trial Balance | Prepared to check accuracy. | Not prepared; Receipts and Payments Account used instead. |

| Accounting Statements | Trading A/c, Profit & Loss A/c, Balance Sheet. | Receipts & Payments A/c, Income & Expenditure A/c, Balance Sheet. |

| Net Result | Net Profit or Net Loss. | Surplus or Deficit. |

| Capital Base | Owner’s Fund (Investment + Reserves). | Capital Fund (Surplus + Subscriptions + Donations). |

Need for Maintaining Books of Accounts and Preparing Final Accounts :

- A not-for-profit organisation does not work to earn profit.

- It deals with public money like subscriptions, donations, and government grants.

- Therefore, it is answerable to society and the public.

- It maintains books of accounts to control cash transactions, including inflow and outflow of cash.

- It helps to know the sources of funds and how the money is used.

- It is necessary to follow legal rules and regulations applicable to the organisation.

- It helps to find out surplus or deficit for a particular period.

- It shows the financial position and net worth of the organisation on a specific date.

- It helps to prevent misuse, fraud, and wrong practices related to funds and assets.

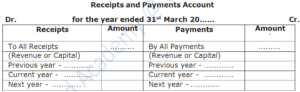

Meaning of Receipts and Payments Account :

- A Receipts and Payments Account is prepared by a not-for-profit organisation.

- It records a summary of all cash receipts and cash payments, including bank transactions.

- It shows the sources of cash (inflows) and the uses of cash (outflows).

- It is similar to a cash book of trading organisations.

- It has two sides – debit side and credit side.

- All cash receipts are recorded on the debit side.

- All cash payments are recorded on the credit side.

- The opening balance of cash and bank is shown on the debit side.

- Bank overdraft is shown on the credit side.

- The account is closed by showing the closing balance of cash and bank or overdraft.

- It records all receipts and payments, whether they are capital or revenue in nature.

- It also includes transactions of previous year, current year, and next year.

Features of Receipts and Payments Account :

- Receipts and Payments Account is a Real Account.

- It is similar to a Cash Book and shows a summary of cash and bank transactions.

- It records all types of receipts and payments, whether capital or revenue.

- It includes transactions of past, current, and future years, if they are received or paid in the current year.

- It records only the actual cash received and paid during the year.

- It does not record outstanding amounts (receivable or payable).

- It helps as a base for preparing final accounts like Income and Expenditure Account and Balance Sheet.

- The opening balance of cash and bank is taken from the previous Balance Sheet.

- The closing balance of cash and bank is shown in the Balance Sheet at the end of the year.

- Non-cash items like depreciation, bad debts, and reserve for doubtful debts are not recorded in this account.

Types of Receipts :

Receipts are of two types: (i) Capital Receipts (ii) Revenue Receipts

(i) Capital Receipts :

- Capital receipts are non-recurring in nature.

- They are not part of regular income of the organisation.

- These receipts are received occasionally.

Examples of capital receipts are:

- Sale of fixed assets

- Life membership fees

- Donations for building construction

Capital receipts are either added to capital fund or shown on the liabilities side of the Balance Sheet.

(ii) Revenue Receipts :

- Revenue receipts are recurring in nature.

- They are part of the regular income of the organisation.

- These receipts are received regularly.

Examples of revenue receipts are:

- Subscriptions from members

- Interest on investments

- Rent received

- Entrance or admission fees

Types of Payments :

Payments are classified into three types: (i) Capital Expenditure (ii) Revenue Expenditure (iii) Deferred Revenue Expenditure

(i) Capital Expenditure :

- Capital expenditure is non-recurring in nature.

- Its benefits are received for a long period of time.

- It is spent to purchase or increase fixed assets.

- It helps to increase earning capacity, efficiency, and life of assets.

Examples of capital expenditure are:

- Purchase of land

- Building

- Machinery

- Furniture

(ii) Revenue Expenditure :

- Revenue expenditure is incurred for day-to-day activities.

- It is used to maintain fixed assets in working condition.

- It is recurring in nature.

- Its benefits are received immediately.

Examples of revenue expenditure are:

- Wages and salaries

- Rent

- Taxes

- Insurance premium

- Commission

(iii) Deferred Revenue Expenditure

- Deferred revenue expenditure is large expenditure of revenue nature.

- Its benefits are spread over more than one year.

- It is a large expense, so it is not charged fully in one year.

- It is spread over several years.

Example: Heavy advertisement expenses.

- Advertisement expense of ₹40,000 for 4 years.

- In this case, ₹10,000 (1/4th) is charged to the Income and Expenditure Account in the current year.

- The remaining ₹30,000 is shown on the Assets side of the Balance Sheet.

Specimen of Receipts and Payments Account :

Meaning of Income and Expenditure Account :

- Income and Expenditure Account is prepared by a not-for-profit organisation.

- It records incomes and expenses of revenue nature only.

- It helps to find whether the organisation has enough income to meet its expenses.

- It is similar to the Profit and Loss Account of trading organisations.

Other Important Points :

- Only revenue incomes of the current year are recorded on the credit side.

- Examples of income include: Subscriptions received, Entrance fees, Sundry receipts, General donations

- Income of the current year is recorded whether received or not.

- Only revenue expenses of the current year are recorded on the debit side.

- Expenses are recorded whether paid or not.

- A debit balance shows a deficit. A credit balance shows a surplus.

- Deficit is deducted from the capital fund. Surplus is added to the capital fund.

- Capital receipts and capital expenditure are not recorded in this account.

- They are directly shown in the Balance Sheet.

Features of Income and Expenditure Account :

- Income and Expenditure Account is a Nominal Account.

- It records only revenue incomes and revenue expenses of the current year.

- It is similar to a Profit and Loss Account.

- It shows the result of the organisation’s activities.

- It is prepared to find out surplus or deficit for a particular year.

- It is a part of the final accounts of a not-for-profit organisation.

- It is always prepared along with the Balance Sheet.

- It does not have any opening balance.

- A debit balance shows deficit. A credit balance shows surplus.

- It includes both cash and non-cash items.

- Cash items include salaries, rent, etc. Non-cash items include outstanding expenses, depreciation, bad debts, provisions, and discounts.

Specimen Income and Expenditure Account :

Distinguish between Receipts and Payments Account and Income and Expenditure Account :

| Point | Receipts & Payments Account | Income and Expenditure Account |

| 1) Type of Account | It is a Real Account. | It is a Nominal Account. |

| 2) Nature | It is similar to cash Book. | It is like a Profit and Loss Account. |

| 3) Object | It is prepared to present a summary of cash transactions | It is prepared to ascertain the net results of all Income and Expenditure transactions |

| 4) Opening Balance | It starts with opening cash balance and Bank balance or Bank over draft. | It has no opening balance. |

| 5) Closing Balance | The closing balance represents cash in hand and cash of Bank at the end of the given period. | The closing balance represents either surplus or deficit. |

| 6) Receipts and Payments | All receipts and payments during the current period are recorded in this account (Revenue or capital) | only Revenue - Receipts and Revenue Expenses are related to current period are recorded in this account. |

| 7) Non - cash items | Non - cash items are not recorded in this account. | In this account non - cash items like bad - debts, Dep. outstanding expenses etc. are also included. |

| 8) All Accounts | All transections related to personal Accounts, Real Accounts and Nominal Accounts. | This Account contains only transections related to Nominal Accounts. |

| 9) Period | It includes amounts received or amount paid for any period like previous year, current on next year. | In this accounts amount related to current year only are included. |

| 10) Balance Sheet | It need not be necessarily accompanied by a Balance Sheet. | It is always accompanied by a Balance Sheet. |

Preparation of Income and Expenditure Account :

- Income and Expenditure Account is prepared from the Receipts and Payments Account and additional information.

- It is a Nominal Account.

- All revenue expenses and losses are debited to this account.

- All revenue incomes and gains are credited to this account.

- Its method of preparation is similar to Profit and Loss Account.

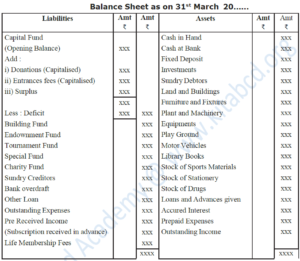

Preparation of Balance Sheet :

- The Balance Sheet of a not-for-profit organisation is similar to that of a sole trading concern.

- It is prepared to know the financial position of the organisation on a particular date.

- It includes capital receipts and capital expenditures.

- The excess of assets over liabilities is called Capital Fund.

- If the capital fund is not given, it can be calculated by preparing an opening Balance Sheet.

Capital Fund : Capital Fund is the excess of total assets over total liabilities.

- It is shown on the liabilities side of the Balance Sheet.

- It is created from capital incomes.

- It also includes capitalised funds like donations, entrance fees, and admission fees.

- The surplus from the Income and Expenditure Account is added to the Capital Fund.

- The deficit from the Income and Expenditure Account is deducted from the Capital Fund.

Specimen of Balance Sheet :

Some times instead of adding surplus into Capital Fund, it is accumulated as a credit Balance to Income and Expenditure Account. such balance is shown separate in Balance Sheet. On the Liabilities side making there of may be as under.

Adjustments in Not-for-Profit Organisations

Adjustments are made to show correct income and expenses for a particular period.

Expenses-Related Adjustments :

- Outstanding Expenses are expenses incurred but not yet paid : They are added to expenses in Income & Expenditure A/c. They are shown as a liability in Balance Sheet.

- Prepaid Expenses are expenses paid in advance : They are subtracted from expenses. They are shown as an asset in Balance Sheet.

- Closing Stock of Stationery means unused stationery at the end : It is deducted from stationery expense. It is shown as an asset in Balance Sheet.

Income-Related Adjustments :

- Accrued Income is income earned but not received : It is added to income. It is shown as an asset in Balance Sheet.

- Income Received in Advance is income received for future period : It is subtracted from income. It is shown as a liability in Balance Sheet.

- Outstanding Subscriptions are subscriptions not yet received : They are added to subscription income. They are shown as an asset in Balance Sheet.

- Subscriptions Received in Advance are received for future years : They are deducted from current income. They are shown as a liability.

Assets and Fund Adjustments :

- Depreciation is the decrease in value of fixed assets : It is shown as an expense. It is deducted from asset value in Balance Sheet.

- Capitalisation of Entrance Fees means treating entrance fees as capital : It is removed from income. It is added to Capital Fund.

- Special Funds from Donations are for specific purposes : They are not treated as general income. They are shown as a separate fund on liabilities side.

Implied adjustments :

Implied adjustments are "hidden" adjustments found within the Trial Balance or Receipts and Payments account. Even if there are no separate instructions, you must account for them based on the information provided (like dates or percentages).

(1) Payments for Less Than 12 Months (e.g., Salaries for 10 months) :

- Since an accounting year has 12 months, if you only paid for 10, 2 months are still "outstanding."

- Treatment: Add the 2 months' cost to your expenses and show it as a liability in the Balance Sheet.

(2) Insurance Paid in Advance

- If you pay for a full year of insurance in June, but your accounting year ends in March, you have paid for 3 months (April, May, June) too early.

- Treatment: Subtract those 3 months from your expenses and show them as Prepaid Insurance (Asset).

(3) Multi-Year Expenses (e.g., 4-year Advertisement) :

- If you pay for 4 years at once, only 1 year belongs to the current period.

- Treatment: Show 1/4th as an expense. The remaining 3/4th is shown as an asset to be used in future years.

(4) Income for Less Than 12 Months (e.g., Rent received for 11 months) :

- If you only received 11 months of rent, 1 month is still owed to you.

- Treatment: Add the 1 month's rent to your income and show it as an asset (Accrued Income).

(5) Interest on Loans or Investments (Percentage-based) :

- If a loan or investment has a percentage (like "10% Loan" or "9% Bonds"), you must calculate the interest based on how long you held it during the year.

- Interest on Loan: Show as an expense and add to the loan liabilities.

- Interest on Investment/Bonds: Show as income and add to the assets.

(6) Leasehold Land Depreciation :

- If land is leased for a fixed period (e.g., 10 years), a portion of its value “expires” each year.

- Treatment: Divide the total cost by the number of years. Show that annual amount as an expense and subtract it from the land’s value in the Balance Sheet.

(7) Profit or Loss on Sale of Assets

- When you sell part of your furniture or machinery, you compare the Book Value (what it's worth on your books) to the Sale Price.

- If sold for MORE (Profit): Show the profit as income.

- If sold for LESS (Loss): Show the loss as an expense.

- Asset Change: In both cases, subtract the original book value of the sold item from your total assets.

Important Accounting Terms :

(1) Entrance Fees / Admission Fees (Not-for-Profit Organisations) :

Meaning: Entrance fees (or admission fees) are the amounts received from new members when they join a Not-for-Profit organisation.

- It is paid only once at the time of admission.

- It is different from annual subscription, which is paid every year.

Nature of Entrance Fees (Confusion) :

There are two views:

(i) Capital Receipt View :

- Received only once from each member

- Non-recurring in nature

- Helps build the Capital Fund

(ii) Revenue Receipt View :

- Though paid once per member, it is received regularly as new members join

- Hence treated as income

Accounting Treatment :

General Rule (Very Important):

(i) If no specific instruction is given → Treat entrance fees as Revenue Receipt. Show it in Income and Expenditure Account (Income side)

(ii) If specific instruction is given:

Example:

If 60% is to be capitalised →

- 60% → Add to Capital Fund (Balance Sheet – Liabilities side)

- 40% → Show in Income and Expenditure Account

(2) Subscriptions :

Meaning: Subscription is the amount paid by members regularly (usually yearly) for the services or objectives of a Not-for-Profit organisation.

- It is the main source of income for such organisations.

Important Points:

It may relate to:

- Past year

- Current year

- Future year

- It is a revenue receipt

Accounting Treatment:

Receipts and Payments Account : Record total subscription received on the debit side

Income and Expenditure Account : Record only current year subscription on the credit side

(3) Legacy

Meaning: Legacy is the amount or property received by a Not-for-Profit organisation through a will after the death of a donor.

Important Points:

- It is not regular (non-recurring)

- It is usually a large amount

- Treated as capital receipt

Accounting Treatment:

- Receipts and Payments Account : Record on the debit side when received

- Balance Sheet : Show on Liabilities side (Capital Fund)

(4) Life Membership Fees :

Meaning: Life membership fees are the lump sum amount paid by a member to become a lifetime member of a Not-for-Profit organisation.

Important Points:

- Paid only once in a lifetime

- Member does not need to pay subscription again

- It is non-recurring

- Treated as capital receipt

Accounting Treatment:

- Balance Sheet : Added to Capital Fund (Liabilities side)

- Not shown in Income and Expenditure Account (because it is capital)

(5) Sale of Old Assets :

Meaning: Not-for-Profit organisations sell old or outdated assets like:

- Furniture

- Machinery

- Equipment

Profit or Loss Calculation:

- Profit on Sale = Sale Proceeds – Book Value (Cost of asset at time of sale)

- Loss on Sale = Book Value – Sale Proceeds

Accounting Treatment:

- Receipts and Payments Account : Record sale proceeds on receipt (debit) side

- Income and Expenditure Account : Profit → Credit side (income), Loss → Debit side (expense)

(6) Scrap :

Meaning: Scrap includes: Small leftover pieces, Old machine parts, Waste materials (like metal, etc.)

Important Points:

- Sold occasionally

- Generates small income

- Treated as miscellaneous income

Accounting Treatment:

- Receipts and Payments Account : Shown on debit (receipts) side

- Income and Expenditure Account : Shown on credit side (income)

(7) Newspapers (Old Newspapers, Magazines, etc.) :

Meaning: Amount received from selling: Old newspapers, Magazines, Periodicals

Important Points:

- Regular small income

- Treated as miscellaneous income

Accounting Treatment:

- Receipts and Payments Account : Debit side

- Income and Expenditure Account : Credit side

(8) Specific Donations :

Meaning: Donation received for a specific purpose, such as: Building fund, Charity, Special project

Important Points:

- Used only for the given purpose

- Not part of normal income

- Treated as capital receipt

Accounting Treatment:

- Balance Sheet : Shown as Specific Fund (Liabilities side)

- Expenses related to it : Deducted from the same fund (not shown in I&E A/c)

(9) General Donations :

Meaning: Donations received for general purposes like: Welfare of members, General activities

Important Points:

- No specific restriction

- May be received regularly

- Treated as revenue receipt

Accounting Treatment:

- Income and Expenditure Account : Shown on credit side (income)

Special Note:

- If no instruction is given in a problem,

- Treat donation as general donation (revenue)

(10) Specific Fund :

Meaning: A Specific Fund is a fund created for a particular purpose, such as:

- Building construction

- Swimming pool

- Prizes

- Operation theatre

Important Points:

- Used only for that specific purpose

- Separate accounting is maintained

- Not part of normal income/expenses

Accounting Treatment:

- All related incomes : Added to the Specific Fund

- All related expenses : Deducted from the Specific Fund

- Income and Expenditure Account : Not affected

- Balance Sheet : Shown on Liabilities side

(11) Endowment Fund :

Meaning: An Endowment Fund is a fund created from:

- Donation / Will (bequest)

- Its income (interest) is used for a specific purpose

Example:

- Prize distribution

- Scholarships

- Welfare activities

Important Points:

- It is a permanent fund

- The main amount is invested

- Only income (interest) is used

- Provides regular income source

Accounting Treatment:

- Fund Amount Received : Recorded in Receipts and Payments A/c (debit side). Shown in Balance Sheet (Liabilities side)

- Interest / Income from Investment : Added to Endowment Fund (not to I&E A/c)

- Expenses related to it : Deducted from the Endowment Fund

We reply to valid query.