Notes

|

Topics to be Learn : (A) Introduction to Partnership Accounts Topics to be Learn :

(B) Partnership Final Accounts

Profit and Loss Account and Balance Sheet with following adjustments. (1) Closing Stock (2) Outstanding expenses (3) Prepaid expenses (4) Income received in advance (5) Income receivable (6) Bad debts (7) Provision for doubtful debts (8) Reserve for discount on Debtors and Creditors (9) Depreciation (10) Interest on capital, drawings and loan. (11) Interest on Investments and loans given (12) Goods destroyed by fire/accident (Insured & Uninsured) (13) Goods stolen (14) Goods distributed as free samples (15) Goods withdrawn by partners (16) Unrecorded purchases and sales (17) Capital expenditure included in revenue expenses and vice versa (18) Bills Receivable dishonoured (19) Bills Payable dishonoured (20) Deferred expenses (21) Capital receipts included in revenue receipts and vice versa (22) Commission to working partners on the basis of Gross Profit, Net Profit/Sales etc. |

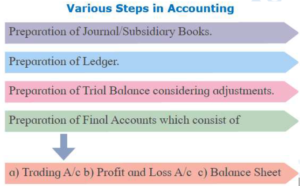

Introduction and necessity of preparation of Final Accounts :

Introduction :

- Every trading organisation prepares Final Accounts at the end of every financial year to find out the profit or loss (net result) of the business and to know its financial position.

- According to the Income Tax Act, 1961, the financial (accounting) year in India is of 12 months, starting from 1st April and ending on 31st March of the next year.

- Final Accounts are prepared with the help of the Trial Balance and some additional information or adjustments.

- Thus, preparation of Final Accounts is the last step in the accounting process.

The various steps of accounting are shown in the following diagram :

Necessity of preparation of Final Accounts :

- To find Gross Profit or Gross Loss : It helps to know the gross profit earned or gross loss suffered during a financial year.

- To find Net Profit or Net Loss : It shows the actual profit or loss of the business after deducting all expenses for the year.

- To know the Financial Position : It shows the assets (what the business owns), liabilities (what the business owes), and capital invested by the owner.

- For Future Planning : It helps in preparing financial statements useful for planning and decision-making.

- To know Amounts due from Debtors and to Creditors : It shows how much money is to be received from customers and how much is to be paid to suppliers.

- To know Sources and Uses of Funds : It shows where the money comes from and how it is used in the business.

- To Calculate Accounting Ratios : It helps in calculating different ratios to analyse the performance of the business.

- To Obtain Loans : Banks and financial institutions require final accounts to give loans.

- To Find Goodwill of a Partnership Firm : It helps to calculate goodwill at the time of admission, retirement, death of a partner, or dissolution of the firm.

- To Calculate Taxes : It helps in computing income tax, sales tax, and other taxes payable to the government.

Preparation of Partnership Final Accounts :

In partnership firms, Final Accounts include two types of statements:

(i) Income Statements :

These include:

- Trading Account (to find gross profit or gross loss)

- Profit and Loss Account (to find net profit or net loss)

(ii) Statement of Financial Position :

- Balance Sheet (shows assets and liabilities of the firm)

Trial Balance

- A Trial Balance is a list of balances of all ledger accounts.

- It is prepared at the end of the accounting year.

- It contains all closing balances of ledger accounts maintained in the books of the firm.

- Trial Balance is not an account, but a statement showing balances of all accounts.

When the Trial Balance tallies (agrees), it shows that the accounts are arithmetically correct.

Final Accounts are prepared on the basis of the agreed Trial Balance.

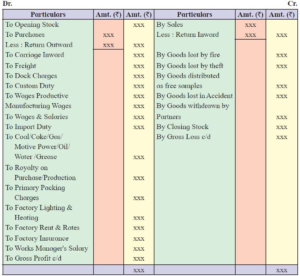

(1) Trading Account :

- A Trading Account is a nominal account and a part of the Income Statement.

- It is prepared to calculate the Gross Profit or Gross Loss of a business for a specific period.

- It includes only direct incomes and direct expenses related to buying and selling of goods.

Debit Side of Trading Account :

It generally includes:

- Opening Stock

- Purchases (less purchase returns)

- Direct expenses such as:

- Wages

- Carriage Inwards

- Factory expenses

- Freight on purchases

- Royalties on purchases

Credit Side of Trading Account :

It generally includes:

- Sales (less sales returns)

- Closing Stock

- Goods lost by fire or theft

- Goods withdrawn by partners

- Goods given as free samples

Result of the Account :

- If the credit side is more, it shows Gross Profit.

- If the debit side is more, it shows Gross Loss.

The balance of Trading Account is transferred to the Profit and Loss Account:

- Gross Profit → Credited to Profit and Loss Account

- Gross Loss → Debited to Profit and Loss Account

According to J. R. Batliboi, the Trading Account shows the result of buying and selling goods. It includes only transactions related to goods and ignores general office or establishment expenses.

Pro forma of Trading Account :

In the books of …………. and ………

Trading Account for the year ended 31st March, 20……

Notes on Trading Account :

(i) Treatment of ‘Wages and Salaries’

- If the term is “Wages and Salaries” (wages written first), it is transferred to the Debit side of Trading Account.

- If the term is “Salaries and Wages” (salaries written first), it is transferred to the Debit side of Profit and Loss Account.

(ii) Valuation of Closing Stock

- If closing stock is given at cost price and market price, it should be shown at whichever is lower (Cost or Market Price, whichever is less).

(iii) Treatment of Trade Expenses

- If Trade Expenses are given along with items like Sundry Expenses, General Expenses, or Office Expenses, then Trade Expenses should be shown on the Debit side of Trading Account.

- If only Trade Expenses are given and no other expenses like Sundry or General Expenses are mentioned, then they should be debited to the Profit and Loss Account.

(iv) Treatment of Royalty

- If nothing is mentioned about Royalty, it should be recorded on the Debit side of Trading Account (as a direct expense).

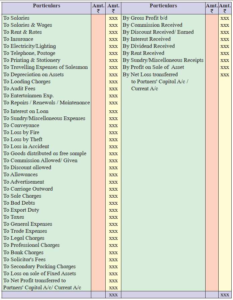

(2) Profit and Loss Account :

- Profit and Loss Account is prepared to find out the net profit or net loss of a business during an accounting year. It is a nominal account.

- It is prepared after the Trading Account. The Gross Profit or Gross Loss from the Trading Account is transferred to the Profit and Loss Account.

Debit Side (Expenses) : All indirect expenses are shown on the debit side. These include: Office and administrative expenses, Selling and distribution expenses, Other revenue expenses

Credit Side (Incomes) : All indirect incomes are shown on the credit side. These include: Commission received, Discount received, Interest received, Rent received, Other sundry incomes

Result of the Account : If the credit side is more, it shows Net Profit. If the debit side is more, it shows Net Loss.

The Net Profit is transferred to the credit side of Partners’ Capital Accounts in their profit-sharing ratio.

The Net Loss is transferred to the debit side of Partners’ Capital Accounts.

Definition : According to Prof. R. N. Carter, “A Profit and Loss Account is an account into which all gains and losses are considered in order to ascertain the excess of gains over losses or vice versa.”

Pro forma of Profit and Loss Account :

Profit and Loss Account for the year ended, 31st March, 20 ….

Dr. Cr.

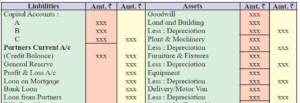

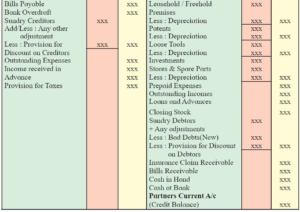

(3) Balance Sheet :

A Balance Sheet is not an account. It is a statement that shows the financial position of a business on a particular date. It shows what the business owns (Assets) and what the business owes (Liabilities).

Left-Hand Side – Liabilities : All closing balances of liabilities are shown on the left side. Liabilities mean the amounts the business has to pay, such as:

- Capital

- Loans

- Creditors

- Outstanding expenses

Right-Hand Side – Assets : All closing balances of assets are shown on the right side. Assets mean the properties and resources owned by the business, such as:

- Cash

- Bank balance

- Furniture

- Machinery

- Debtors

According to A. Palmer, "a statement on a particular date showing on one stde the trader's property and possessions and on the other side the liabiltttes."

Pro forma of Balance Sheet :

Balance Sheet as on 31st March,….

Adjustments :

(1) Closing Stock :

- It is shown on the credit side of Trading Account.

- It is also shown on the asset side of Balance Sheet.

(2) Outstanding Expenses :

- Add outstanding amount to the concerned expense in Trading Account or Profit and Loss Account.

- Show the outstanding amount on the liabilities side of the Balance Sheet.

(3) Prepaid Expenses :

- Deduct the prepaid amount from the concerned expense in the Trading Account or Profit and Loss Account.

- Show the prepaid amount on the asset side of the Balance Sheet.

(4) Income received in advance (Pre-received Income) :

- Deduct the advance amount from the concerned income in the Profit and Loss Account.

- Show the advance amount on the liabilities side of the Balance Sheet.

(5) Income receivable :

- Add the receivable amount to the concerned income in the Profit and Loss Account.

- Show the receivable amount on the asset side of the Balance Sheet.

(6) Additional (New) Bad Debts :

- Show the additional bad debts on the debit side of the Profit and Loss Account.

- Deduct the amount of additional bad debts from Sundry Debtors on the asset side of the Balance Sheet.

(7) Provision for Doubtful Debts (New R.D.D.) :

- Show the amount of new provision on the debit side of the Profit and Loss Account.

- Deduct the amount of provision from Sundry Debtors on the asset side of the Balance Sheet.

(8) Reserve for Discount on Debtors :

- Show the amount of new reserve on the debit side of the Profit and Loss Account.

- Deduct the amount of reserve from Sundry Debtors (after deducting Bad Debts and Provision for Doubtful Debts) on the asset side of the Balance Sheet.

(9) Depreciation :

- Show the amount of depreciation on the debit side of the Profit and Loss Account.

- Deduct the amount of depreciation from the concerned asset on the asset side of the Balance Sheet.

(10) (i) Interest on Capital :

- Show Interest on Capital on the debit side of the Profit and Loss Account.

- Add Interest on Capital to the Partners’ Capital Accounts on the liabilities side of the Balance Sheet.

(ii) Interest on Drawings :

- Show Interest on Drawings on the credit side of the Profit and Loss Account.

- Deduct Interest on Drawings from the Partners’ Capital Accounts on the liabilities side of the Balance Sheet.

(iii) Interest on Loan Taken :

- Show Interest on Loan on the debit side of the Profit and Loss Account.

- If unpaid, show it on the liabilities side of the Balance Sheet as Outstanding Interest.

(11) (i) Interest on Investment :

- Show Interest on Investment on the credit side of the Profit and Loss Account.

- If outstanding, show it on the asset side of the Balance Sheet as Interest Accrued.

(ii) Interest on Loan Given :

- Show Interest on Loan Given on the credit side of the Profit and Loss Account.

- If outstanding, show it on the asset side of the Balance Sheet as Interest Receivable.

(12) (i) Insured Goods Destroyed by Fire/Accident :

- Deduct the value of goods destroyed from Purchases in the Trading Account.

- Show the insurance claim receivable on the asset side of the Balance Sheet.

- If there is any loss (not compensated by insurance), show it on the debit side of the Profit and Loss Account.

(ii) Uninsured Goods Destroyed by Fire/Accident :

- Deduct the value of goods destroyed from Purchases in the Trading Account.

- Show the total loss on the debit side of the Profit and Loss Account.

(13) Goods Stolen :

- Deduct the value of goods stolen from Purchases in the Trading Account.

- Show the loss on the debit side of the Profit and Loss Account.

(14) Goods Distributed as Free Samples :

- Deduct the value of goods distributed as free samples from Purchases in the Trading Account.

- Show the value on the debit side of the Profit and Loss Account as Advertisement or Sales Promotion Expenses.

(15) Goods Withdrawn by Partners for Personal Use :

- Deduct the value of goods withdrawn from Purchases in the Trading Account.

- Deduct the value from the Partners’ Capital Accounts on the liabilities side of the Balance Sheet.

(16) (i) Unrecorded Purchases :

- Add the amount of unrecorded purchases to Purchases in the Trading Account.

- Show the amount on the liabilities side of the Balance Sheet as Creditors, if unpaid.

(ii) Unrecorded Sales :

- Add the amount of unrecorded sales to Sales in the Trading Account.

- Show the amount on the asset side of the Balance Sheet as Debtors, if not yet received.

(17) (i) Capital Expenditure Included in Revenue Expenditure :

- Deduct the capital amount from the concerned expense in the Trading Account or Profit and Loss Account.

- Add the capital amount to the concerned asset on the asset side of the Balance Sheet.

(ii) Revenue Expenditure Included in Capital Expenditure :

- Deduct the revenue amount from the concerned asset on the asset side of the Balance Sheet.

- Show the revenue amount on the debit side of the Trading Account or Profit and Loss Account.

(18) Bills Receivable Dishonoured :

- Add the amount of dishonoured bill to Sundry Debtors on the asset side of the Balance Sheet.

- If any noting charges are paid, show them on the debit side of the Profit and Loss Account.

(19) Bills Payable Dishonoured :

- Add the amount of dishonoured bill to Sundry Creditors on the liabilities side of the Balance Sheet.

- If any noting charges are paid, show them on the debit side of the Profit and Loss Account.

(20) Deferred Advertisement Expenses (Paid for 5 Years) :

- Show 1 year’s advertisement expense on the debit side of the Profit and Loss Account.

- Show the remaining amount (unexpired portion) on the asset side of the Balance Sheet as Deferred Advertisement Expense.

(21) Revenue Receipts Included in Capital Receipts :

(Example: Sale of goods included in Sale of Furniture)

- Deduct the revenue amount from the concerned capital receipt (e.g., Furniture Account).

- Add the revenue amount to Sales in the Trading Account.

(22) Commission to Partners (on Gross Profit / Sales) :

- Show the commission on the debit side of the Profit and Loss Account.

- Add the commission to the Partners’ Capital or Current Accounts on the liabilities side of the Balance Sheet.

Hidden Adjustment Given in Trial Balance :

(1) Salaries/Rent Paid for 10 Months :

- Add the amount of 2 months’ outstanding Salaries/Rent to the concerned expense in the Trading Account or Profit and Loss Account.

- Show the 2 months’ outstanding amount on the liabilities side of the Balance Sheet.

(2) Insurance Paid for One Year (Up to 30th June, Year Ends 31st March) :

- Deduct 3 months’ prepaid insurance from Insurance on the debit side of the Profit and Loss Account.

- Show the 3 months’ prepaid insurance on the assets side of the Balance Sheet.

(3) Advertisement Expenses for 4 Years :

- Show only 1/4th of the advertisement expense on the debit side of the Profit and Loss Account.

- Show the remaining 3/4th (not written off) on the assets side of the Balance Sheet as Deferred Advertisement Expense.

(4) Rent Received for 11 Months :

- Add 1 month’s outstanding rent to Rent Received on the credit side of the Profit and Loss Account.

- Show the same amount as Rent Receivable on the assets side of the Balance Sheet.

(5) 10% Loan Borrowed on 1st January (Year Ends 31st March) :

- Show 3 months’ interest on loan on the debit side of the Profit and Loss Account.

- Show the outstanding interest on the liabilities side of the Balance Sheet.

(6) 16% Investment Purchased on 1st January (Year Ends 31st March) :

- Show 3 months’ Interest Receivable on Investment on the credit side of the Profit and Loss Account.

- Show the same amount as Interest Receivable on the assets side of the Balance Sheet.

(7) 10% Government Bonds :

- Show the Interest Receivable on the credit side of the Profit and Loss Account.

- Add the Interest Receivable to Government Bonds or show it separately on the assets side of the Balance Sheet.

Important Points/Notes :

(1) Every item in the trial balance must be shown only once and in just one part of the final accounts.

(2) Give at least two effects of every adjustments.

(3) Debit balances of Trial Balance will appear on the Debit side of Trading A/c or on the Debit side of Profit and Loss A/c or on the Assets side of Balance Sheet.

(4) Credit balances of Trial Balance will appear on the Credit side of Trading A/c or on the Credit side of Profit and Loss A/c or on the Liabilities side of Balance Sheet.

(5) Pass the effects of the adjustments for Bad debts, Provision for Bad and Doubtful debts and Reserve for discount on debtors, after other adjustments of Debtors are given effected.

(6) After giving effects of concerning creditors, pass the effect for Reserve for discount on creditors.

(7) Hidden or self explanatory adjustments are to be given effect even if there is no special instruction in the problem related to this is mentioned.

(8) When the date of drawings is not given, interest on drawings should be calculated on average basis or for the period of six months,

Interest on drawings = Amount of drawings x \(\frac{\text{Amount of drawing}}{100}×\frac{6}{12}\) [I = \(\frac{PRN}{100}\)]

(9) If a manager or a partner is allowed commission at a certain percentage on Net profit such commission should be calculated as follows :

(a) If it is on Net profit before charging such commission :

Commission amount = \(\frac{\text{Rate of commission × Net profit}}{100}\)

(b) If it is on Net profit after charging such commissions

Commission amount = \(\frac{\text{Rate of commission × Net profit}}{100}\)

Treatment of some important Items appearing in Trial Balance only :

| i) | Any outstanding expenses | Liability Side of Balance Sheet |

| ii) | Any Prepaid Expenses | Asset Side of Balance Sheet |

| iii) | Any outstanding income | Asset Side of Balance Sheet |

| iv) | Income Received in Advance | Liability Side of Balance Sheet |

| v) | Depreciation | Debit Side of Profit & Loss A/c |

| vi) | Loss on Sale of any Asset | Debit Side of Profit & Loss A/c |

| vii) | Goods withdrawn by partner | Debit Side of Capital/Current A/c |

| viii) | General Reserve / Reserve Fund | Liability Side of Balance Sheet |

| ix) | Deposit from Public | Liability Side of Balance Sheet |

| x) | Goods distributed as free samples | Debit side of Profit & Loss A/C |

| xi) | Suspense Account:

a) If it is on Debit Side b) If it is on Credit Side |

Show the same figure on Asset Side Show the same figure on Liability Side |

| xii) | Bank for Collection of Bills | Asset Side of Balance Sheet |

We reply to valid query.