Notes

|

Topics to be Learn : (A) Introduction to Partnership Accounts Topics to be Learn :

(B) Partnership Final Accounts

Profit and Loss Account and Balance Sheet with following adjustments. (1) Closing Stock (2) Outstanding expenses (3) Prepaid expenses (4) Income received in advance (5) Income receivable (6) Bad debts (7) Provision for doubtful debts (8) Reserve for discount on Debtors and Creditors (9) Depreciation (10) Interest on capital, drawings and loan. (11) Interest on Investments and loans given (12) Goods destroyed by fire/accident (Insured & Uninsured) (13) Goods stolen (14) Goods distributed as free samples (15) Goods withdrawn by partners (16) Unrecorded purchases and sales (17) Capital expenditure included in revenue expenses and vice versa (18) Bills Receivable dishonoured (19) Bills Payable dishonoured (20) Deferred expenses (21) Capital receipts included in revenue receipts and vice versa (22) Commission to working partners on the basis of Gross Profit, Net Profit/Sales etc. |

Introduction :

- A sole proprietorship has many limitations. It has limited capital, limited managerial ability, unlimited liability, no stability, and no specialization. Because of these problems, it is not suitable for large businesses that need more money and involve more risk.

- So, when a business needs more capital and has higher risk, two or more people come together to run it. They agree to share the capital, management, risk, and profits of the business.

- This type of relationship, which is based on an agreement between two or more persons, is called Partnership. The persons who enter into partnership are called Partners, and together they are known as a Firm.

Meaning and Definition of Partnership :

Meaning of Partnership : Partnership is a form of business organization in which two or more persons come together to run a business. They agree to share the profits and losses of the business.

Definition of Partnership :

- According to Indian Partnership Act, 1932, Section 4: “Partnership is the relation between persons who have agreed to share the profits of a business carried on by all or any one of them acting for all.”

- According to Handy: “Partnership is the relation between persons competent to make a contract, who agree to carry on a lawful business in common with a view to earn private gain.”

The features of a partnership firm :

- Agreement : Partnership is formed by an agreement between partners. The agreement may be oral or written, but a written agreement is preferred. The written agreement is called a Partnership Deed and it acts as legal proof.

- Number of Partners : At least two persons are required to form a partnership. According to the Companies Act, 2013, the maximum number of partners is 50.

- Lawful Business : The partnership must carry on a lawful business. Illegal activities are not allowed under law.

- Sharing of Profits and Losses : Partners share profits and losses according to the ratio mentioned in the agreement. If no ratio is mentioned, profits and losses are shared equally.

- Unlimited Liability : The liability of partners is unlimited, joint and several. If the firm’s assets are not enough to pay debts, partners must pay from their personal property. If one partner becomes insolvent, the remaining partners bear the liability.

- Registration : Under the Indian Partnership Act, 1932, registration of a partnership firm is optional. However, in Maharashtra, registration has been compulsory since April 1, 2005. Registration records the firm’s name with the Registrar.

- Joint Ownership and Management : All partners are joint owners of the firm’s property and cannot use it for personal purposes. Every partner has the right to take part in management.

- Principal and Agent Relationship : A partner acts in a dual role —

- As a principal when dealing with outsiders.

- As an agent when dealing with other partners.

- Dissolution : A partnership firm can be dissolved by mutual agreement. It can also be dissolved due to death, retirement, insolvency, insanity of a partner, or by giving notice as per agreement.

Partnership Deed :

- A Partnership Deed is a written document that contains the agreement between partners. It includes all the terms and conditions decided by the partners for running the business.

- An agreement can be oral or written, but when it is written, it is called a Partnership Deed. According to the Indian Partnership Act, 1932, having a written deed is not compulsory. However, it is always better to have a written and signed deed to avoid disputes in the future.

- The Partnership Deed contains the rules and regulations for the internal management of the firm. It is also called the Articles of Partnership.

Contents of Partnership Deed :

A Partnership Deed generally includes the following points:

- Name and address of the firm and its main business.

- Name and address of all partners and duration of the partnership.

- Capital contribution of each partner.

- Profit and loss sharing ratio.

- Rights, duties, and liabilities of partners.

- Rules regarding admission, retirement, and death of a partner.

- Rate of interest on capital, loan, drawings, etc.

- Salary or commission payable to partners (if any).

- Method of settlement of accounts at the time of dissolution.

- Method of solving disputes among partners.

- Any other matter related to the conduct of business.

Importance of Partnership Deed :

The Partnership Deed is very important because:

- It is a written proof of the agreement.

- It clearly defines the rights, duties, and liabilities of partners.

- It forms the basis of the mutual relationship among partners.

- It helps to avoid misunderstandings and disputes in the future.

Thus, a Partnership Deed ensures smooth and proper functioning of the partnership firm.

Indian Partnership act 1932:

At the time of forming a partnership firm, a Partnership Deed is prepared which contains all the terms and conditions. But if the deed is silent on any point, then the provisions of the Act (especially Sections 12 and 17) are applied to decide the matter.

Provisions Applicable When Deed is Silent :

- Distribution of Profit : If the profit-sharing ratio is not mentioned in the deed, profits and losses are shared equally among partners.

- Interest on Drawings : If the rate of interest on drawings is not given, interest is charged at the average of six months on the drawings.

- Interest on Partner’s Loan : If a partner gives an additional loan to the firm and the rate of interest is not mentioned, then 6% per annum interest is allowed.

- Interest on Capital : If the deed does not mention interest on capital, then no interest is allowed on capital.

- Salary or Commission to Partners : No partner is entitled to salary, commission, or remuneration for extra work done for the firm unless it is clearly mentioned in the deed.

- Admission of a New Partner : No new partner can be admitted into the firm without the consent of all existing partners.

These rules help in solving disputes when the partnership deed does not clearly mention certain terms.

Methods of Capital Accounts :

The amount of money or assets brought by a partner to run the business is called Capital.

Capital may be brought:

- In cash, or

- In the form of assets like goods, machinery, land, building, furniture, etc.

The capital contributed by partners may be:

- In profit-sharing ratio,

- In equal ratio, or

- In any proportion agreed upon by the partners.

There are two methods of maintaining partners’ capital accounts:

(1) Fixed Capital Method : Under this method, the capital of partners remains fixed.

- Changes like drawings, interest on capital, salary, profit, etc., are recorded in a separate Current Account.

- The Capital Account does not change unless additional capital is introduced or withdrawn permanently.

(2) Fluctuating Capital Method : Under this method, the Capital Account changes every year.

- All items like drawings, interest, salary, and share of profit or loss are recorded directly in the Capital Account.

According to the Indian Partnership Act, 1932, there is no specific rule about which method to adopt. The partners can decide the method and mention it in the Partnership Deed.

If the deed is silent, then the firm should follow the Fluctuating Capital Method.

(1) Fixed Capital Method :

Under the Fixed Capital Method, the opening capital of a partner remains the same throughout the financial year.

The capital balance changes only when:

- The partner introduces additional capital, or

- The partner withdraws a part of capital permanently.

In this method, along with the Capital Account, a separate account called Current Account is opened for each partner. The Current Account records all other transactions like drawings, interest, salary, share of profit or loss, etc.

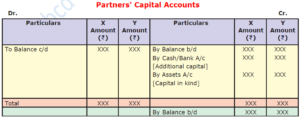

(i) Partner’s Capital Account : Under this account, the following entries are recorded:

- Opening Capital – The amount contributed by the partner at the beginning of the business (or the opening balance if the firm is already existing).

- Additional Capital – Any extra capital introduced during the accounting year.

- Withdrawal of Capital – Any part of capital withdrawn permanently during the year.

Usually, the Partner’s Capital Account shows a credit balance and it is shown on the Liabilities side of the Balance Sheet.

Pro forma of Partners' Capital Accounts : The pro forma of Partners' Capital Accounts prepared under Fixed Capital Method is shown below : It is assumed that there are two partners, viz. X and Y.

Partners' Capital Accounts

Journal Entries :

(1) When additional capital is introduced by a partners

Cash / Bank A/c ...... Dr. xxx

To Partners Capital A/c xxx

(Being additional capital introduced into the business)

(2) When capital amount is brought in by a Partner in form of Assets

Assets A/c ..... Dr. xxx

To Partners Capital A/c xxx

(Being additional capital brought in kind)

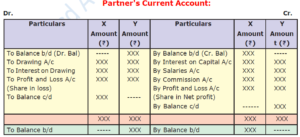

(ii) Partners' Current Accounts : If Fixed Capital Method is adopted by the firm, then Current Account for each partner is opened and operated. In Current Account, following transactions are recorded :

(1) Drawings (if any) made by the partner in the current accounting year.

(2) Cash or goods or any other asset taken over by the partner.

(3) Interest on Partners' Capital allowed by the firm.

(4) Interest on Partner's Drawings charged by the firm.

(5) Salary, Commission, Rent, Interest on loan, Allowance, etc. payable to the partner.

(6) Distribution of net divisible profit or net divisible loss of the firm.

Pro forma of Partners' Current Accounts : The pro forma of Partners' Current Accounts prepared under Fixed Method is shown below : In the following pro forma ledger accounts, it is assumed that X's Current A/c showed a credit balance and Y's Current A/c showed a debit balance at the beginning of the year.

Partner's Current Account:

Journal Entries :

(1) Interest allowed on partner's capital

(a) Interest on Capital A/c.......................................... Dr. XXX

To Partners Capital A/c/ Current Account XXX

(Being interest due on capital)

(b) Profit and Loss A/C............................................ Dr XXX

To interest on Capital A/C XXX

(Being interest on Capital transferred to profit and loss account)

(2) Salary or Commission allowed to partners

(a) Salary or Commission in Partner A/c.............................Dr. XXX

To Partners Current A/c / Capital Account ..................... XXX

(Being Salary or Commission due for payment)

(b) Profit and Loss A/C.............................................. Dr XXX

To Salaries/ Commission A/C.......................................... XXX

(Being Salary/ Commission transferred to Profit and Loss A/C)

(3) Cash or Goods taken over by the partners for their personal use.

(a) Drawing A/c................................................ Dr. XXX

To Cash or Goods A/C XXX

(Being cash or goods withdrawn for personal use)

(b) Partners Current A/c / Capital A/c............................ Dr XXX

To Drawing A/c XXX

(Being balance on account transferred to current A/c)

(4) Interest charged on drawing of the partners

(a) Partners Current A/c / Capital A/c....... Dr. XXX

To Interest on Drawing account XXX

(Being interest charged on Drawing)

(b) Interest on Drawings A/C...........Dr XXX

To Profit and Loss A/C XXX

(Being interest on Drawings transferred to profit and loss account)

(5) Transfer of Net Profit

Profit and loss A/c ...........Dr. XXX

To Partners Current A/c / Capital A/c XXX

(Being profit transferred to Partner's Current / Capital Account)

(6) Distribution of Net loss :

Partners Current A/c / Capital A/c....... Dr. XXX

To Profit and Loss A/c XXX

(Being loss adjusted to Partners Current / Capital Account)

Partners' Current Accounts may either show debit balance or credit balance.

- Credit balances of Partners' Current Accounts are transferred to Liabilities side of Balance Sheet.

- Similarly, Debit balances of Partners' Current Accounts are transferred to Assets side of Balance Sheet.

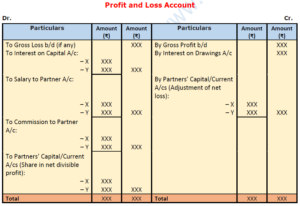

Effects of above entries in Profit and Loss A/c is as follow :

Pro forma of Profit and Loss Account :

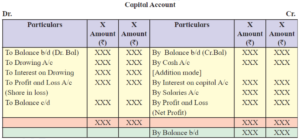

Fluctuating Capital Method :

In the Fluctuating Capital Method, balances on capital accounts changes every year. Under this method, to record partners dealings with partnership firm, only one account 'Capital Account' is opened and following transactions are recorded in it :

(1) Initial or opening balances of capital

(2) Additional capital brought in by partners in form of cash or its kind (Assets)

(3) Salary/Commission payable to partners

(4) Interest payable on capital balance to partners

(5) Drawings made during the year and interest payable on drawings by the partners

(6) Withdrawal of part of the capital by the partners

(7) Division and transfer of net divisible profit or net adjustable loss of the firm.

The credit balances of fluctuating capital accounts of the partners are recorded separately on the Liabilities side of the Balance Sheet.

Pro forma under Fluctuating Capital Method :

Examples :

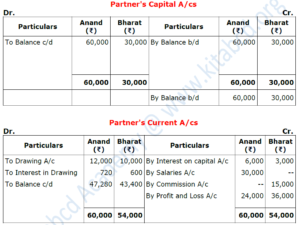

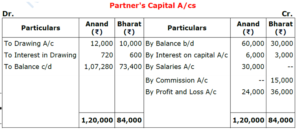

Q.1. Anand and Bharat are partners sharing profits and losses in the ratio 2 : 3. On 1.4.2019 the capital balance are Anand ₹ 60,000 and Bharat ₹ 30,000 their drawings are ₹ 12,000 and ₹ 10,000 respectively. As per the agreement partners are allowed 10% interest on capital and interest on Drawings is to be charged at 12% p.a. Anand gets salary of ₹ 2,500 per month and Bharat is entitled to get commission @ 3% on net sales which is ₹ 5,00,000. The firm's profit is ₹ 60,000. Prepare partners capital account for the year ended 31st March 2019 under :

(1) Fixed Capital Method (2) Fluctuating Capital Method

Solution :

(1) Fixed Capital Method :

(2) Fluctuating Capital Method

Partner's Capital A/cs

Working Notes :

(1) Interest on Capital = Amount of capital x Period x Rate of interest

Interest on Anand’s capital = 60,000 × 1 x \(\frac{10}{100}\) = ₹ 6,000

Interest on Bharat’s capital = 30,000 × 1 x \(\frac{10}{100}\) = ₹ 3,000

(2) Interest on Drawings = Amount of drawings x Period x Rate of interest

Interest on Anand’s drawings = 12,000 × \(\frac{6}{12}\) x \(\frac{12}{100}\) = ₹ 720

Interest on Bharat’s drawings = 10,000 × \(\frac{6}{12}\) x \(\frac{12}{100}\) = ₹ 600

(Interest on Drawing always to be taken for 6 months In case date on Drawings in not mentioned)

(3) Salary payable to Anand = 2500 x 12 = ₹ 30,000

(4) Commission to Anand = 3% on net sales = 5,00,000 × = ₹ 15,000

(5) Distribution of Profit ₹ 60,000 in 2:3 ratio

Anand’s share in profit = 60,000 × \(\frac{2}{5}\) = ₹ 24,000

Bharat’s share in profit = 60,000 × \(\frac{3}{5}\) = ₹ 36,000

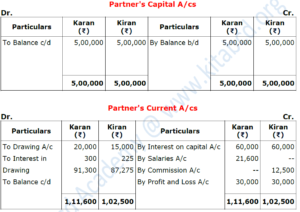

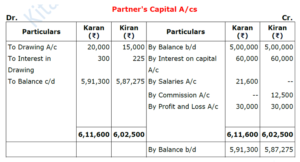

Q.2. Karan and Kiran are partners in M/s Mehta Enterprises. They have started business of ready made garments on 1st April 2019 on which date they contribute ₹ 5,00,000 each as their initial capitals. Karan has withdrawn ₹ 20,000 and Kiran has withdrawn ₹ 15,000 for their personal use. Interest on capital is allowed @ 12% and interest on drawing is charged @ 3% p.a. Karan is entitled to get salary, ₹ 1800 per month, Kiran is allowed to get commission @ 5% on net sales. During the year net sales is ₹ 2,50,000 and net profit earned during the year is ₹ 60,000.

Prepare partners capital accounts under i) Fixed capital Method ii) Fluctuating Capital Method

Solution :

(1) Fixed Capital Method :

(2) Fluctuating Capital Method

Working Notes :

Working Notes :

(1) Interest on capital is calculated as follows :

Interest on Capital = Amount of capital x Period x Rate of interest

Karan : On Opening balance i.e. ₹ 5,00,000 for 1 year

12% p.a. interest = ₹ 5,00,000 ×1 × \(\frac{12}{100}\) = ₹ 60,000

Kiran : On Opening balance i.e. ₹ 5,00,000 for 1 year

12% p.a. interest = ₹ 5,00,000 ×1 × \(\frac{12}{100}\) = ₹ 60,000

(2) Interest on Drawing is charged @3%

Interest on Drawings = Amount of drawings x Period x Rate of interest

Interest on Karan’s Drawings = 20,000 × \(\frac{6}{12}\) x \(\frac{3}{100}\) = ₹ 300

Interest on Kiran’s Drawings = 15,000 × \(\frac{6}{12}\) x \(\frac{3}{100}\) = ₹ 225

(3) Commission paid to Karan = 2,50,000 × \(\frac{5}{100}\) = ₹ 12,500

(4) Profit of ₹ 60,000 is distributed equally between Karan and Kiran

Karan = 60,000 × 12 = ₹ 30,000

Kiran = 60,000 × 12 = ₹ 30,000

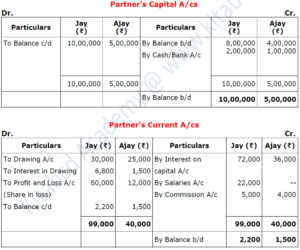

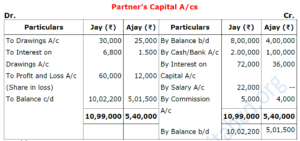

Q.3. Jay and Ajay are partners of a firm with capital balances ₹ 8,00,000 and ₹ 4,00,000 respectively. They share profits and losses in the ratio 5 :1. Additional capital brought in by both the partners are ₹ 2,00,000 and ₹ 1,00,000 respectively on 1st October, 2022. Following transactions are to be recorded in Capital Accounts of Partners under : (i) Fixed Capital Method and (ii) Fluctuating Capital Method.

| Particulars | Jay (₹) | Ajay (₹) |

| Interest on Capital | 8% | 8% |

| Drawing (During the year) | 30,000 | 25,000 |

| Interest on Drawings | 6,800 | 1,500 |

| Salaries | 22,000 | - |

| Commission | 5,000 | 4,000 |

| Share in Loss [For the year 2022-2023] | 60,000 | 12,000 |

Solution :

In the books of Jay and Ajay

(1) Fixed Capital Method :

(2) Fluctuating Capital Method

Working Notes :

(1) Interest on Capital = Amount of capital x Period x Rate of interest

Interest on Jay’s capital = 8,00,000 × 1 x \(\frac{8}{100}\) = ₹ 64,000

= 2,00,000 × \(\frac{6}{12}\) x \(\frac{8}{100}\) = ₹ 8,000

Total Interest = ₹ 72,000

Interest on Ajay’s capital = 4,00,000 × 1 x \(\frac{8}{100}\) = ₹ 32,000

= 1,00,000 × \(\frac{6}{12}\) x \(\frac{8}{100}\) = ₹ 4,000

Total Interest = ₹ 36,000

Next : Part B : Partnership Final Accounts :

- Understand the meaning of Final Accounts.

- Know the need and importance of Final Accounts.

- Know the effects of adjustments in Final Accounts.

- Know the meaning of Trading Account, Profit and Loss Account and Balance Sheet.

- Know how to find out financial results of the business.

We reply to valid query.