Solutions

Question 1. (A) Answer in one sentence.

(1) What is Journal ?

A journal is a book of original entry where business transactions are first recorded in chronological order (date-wise) as they occur.

(2) What is Narration ?

Narration is a brief explanation of a journal entry written in brackets immediately below the entry, usually starting with the word "Being".

(3) What is GST ?

GST stands for Goods and Service Tax, a unified "One nation, One tax, One market" system that includes various previous taxes like Excise Duty, VAT, and Service Tax.

(4) In which year GST was imposed by the Central Government of India ?

GST was imposed and started by the Central Government of India on 1st July 2017.

(5) What is meant by simple entry ?

A simple entry is a journal entry in which only two accounts are affected—one account is debited and the other is credited.

(6) What is the meaning of combined entry ?

A combined (or compound) entry is a journal entry that contains more than one debit, more than one credit, or both.

(7) Which account is debited, when rent is paid by Debit card ?

When rent is paid, the Rent Account is debited because it is an expense.

(8) Which discount is not recorded in the books of account ?

Trade discount, which is an allowance on the printed list price, is not recorded in the books of accounts.

(9) In which order monthly transactions are recorded in a Journal ?

Transactions are recorded in the journal in chronological order, meaning they are entered date-wise in the order in which they take place.

(10) Which account is credited, when goods are sold on credit ?

When goods are sold on credit, the Sales Account is credited.

Question 2. Give one word/term or phrase for each of the following statements:

(1) A book of prime entry.

(2) The tax imposed by Central Government on Goods and Services

(3) Brief explanation of an entry.

(4) The process of recording transactions in the Journal.

(5) The French word from which the word Journal is derived.

(6) Concession given for immediate payment.

(7) Entry in which more than one accounts are to debited or credited.

(8) Anything taken by proprietor from business for his private use.

(9) Tax payable to the Government on purchase of goods.

(10) Page number of the ledger.

(1) A book of prime entry: Journal,

(2) The tax imposed by Central Government on Goods and Services: GST (Goods and Service Tax)

(3) Brief explanation of an entry: Narration,

(4) The process of recording transactions in the Journal: Journalising

(5) The French word from which the word Journal is derived: JOUR

(6) Concession given for immediate payment: Cash Discount

(7) Entry in which more than one accounts are to debited or credited: Combined Entry (or Compound Entry),

(8) Anything taken by proprietor from business for his private use: Drawings

(9) Tax payable to the Government on purchase of goods: Input GST,

(10) Page number of the ledger: Ledger Folio (L.F.)

Q.3 Select the most appropriate alternative from the alternatives given below and rewrite

(1) ……… means explanation of the transactions recorded in the Journal.

(a) Narration (b) Journalising (c) posting (d) Casting

(a) Narration

(2) ……… discount is not recorded in the books of accounts.

(a) Trade (b) Cash (c) GST (d) VAT

(a) Trade

(3) Recording of transaction in Journal is called ……

(a) posting (b) journalising (c) narration (d) prime entry

(b) journalizing

(4) Every Journal entry require ……

(a) casting (b) posting (c) narration (d) journalising

(b) posting

(5) The ……… column of the Journal is not recorded at the time of journalising.

(a) date (b) particulars (c) ledger folio (d) amount

(c) ledger folio

(6) Goods sold on credit should be debited to ………

(a) purchase A/c (b) customer A/c

(c) sales A/c (d) cash A/c

(b) customer A/c

(7) Wages paid for installation of Machinery should be debited to ……

(a) wages A/c (b) machinery A/c

(c) cash A/c (d) Installation A/c

(b) machinery A/c

(8) The commission paid to the agent should be debited to ………

(a) drawing A/c (b) cash A/c

(c) commission A/c (d) Agent A/c

(c) commission A/c

(9) Loan taken from Dena Bank should be credited to ……

(a) Capital A/c (b) Dena Bank A/c

(c) Cash A/c (d) Dena Bank Loan A/c

(b) Dena Bank A/c

(10) Purchase of animals for cash should be debited to ……

(a) Live stock A/c (b) Goods A/c

(c) Cash A/c (d) Bank A/c

(a) Live stock A/c

Question 4 State whether the following statements are True or False with reasons.

(1) Narration is not required for each and every entry.

False. A brief explanation of the transaction, known as a narration, is required for every journal entry to provide clarity and help understand the nature of the transaction.

(2) A journal voucher is must for all transactions recorded in the Journal.

True. A journal voucher is the basic or original documentary evidence upon which business transactions are journalised.

(3) Cash discount allowed should be debited to discount A/c.

True. Cash discount allowed is a loss to the person receiving the payment. According to the rules of nominal accounts, all expenses and losses must be debited.

(4) Journal is a book of prime entry.

True. The journal is the book of original or primary entry where business transactions are first recorded in chronological order as they occur.

(5) Trade discount is recorded in the books of accounts.

False. Trade discount is not recorded in the books of accounts; it is simply deducted from the printed list price, and the entry is made for the net amount.

(6) Goods lost by theft is debited to goods A/c.

False. When goods are lost by theft, the Loss by Theft Account is debited because it is a loss, while the Goods Lost Account (or Purchases Account) is credited because goods are going out of the business.

(7) If rent is paid to landlord, landlord's A/c should be debited.

False. Rent is an expense for the business. Therefore, the Rent Account should be debited (as per the rule "Debit all expenses and losses"), and the Cash/Bank account is credited.

(8) Book Keeping records monetary and non-monetory transactions.

False. Bookkeeping and the journal only keep records of daily financial (monetary) transactions; non-monetary events that cannot be measured in terms of money are not recorded.

(9) Drawings made by the proprietor increases his capital.

False. Drawings represent the value of cash or goods withdrawn by the proprietor for personal use, which reduces the total capital invested in the business.

(10) GST paid on purchase of goods Input tax A/c should be debited.

True. When goods are purchased, the tax paid is called Input Tax, and the respective Input CGST/SGST/IGST accounts are debited along with the purchase.

Question 5. Fill in the blanks.

(1) The first book of original entry is the ………

Journal

(2) The process of recording transaction into journal is called ……

Journalizing

(3) An explanation of the transaction recorded in the journal ……

Narration

(4) …… discount is not recorded in the books of accounts.

Trade

(5) …… is concession allowed for bulk purchase of goods or for immediate payment.

Cash discount

(6) Every Journal Entry requires ……

Narration

(7) …… discount is always recorded in the books of accounts.

Cash

(8) …… is the document on the basis of which the entry is recorded in journal.

Voucher

(9) There are …… parties to a cheque.

Three

(10) The …… cheque is more safe than other cheques as it cannot be encashed on the counter of the bank.

Crossed.

Question 6.

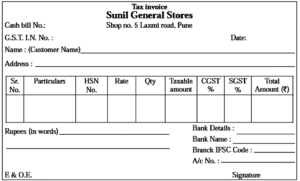

(1) Prepare specimen of Tax Invoice

Specimen of Tax Invoice :

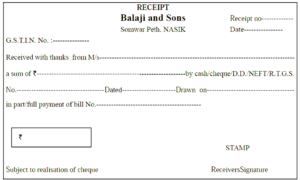

(2) Prepare specimen of Receipt

Specimen of Receipt :

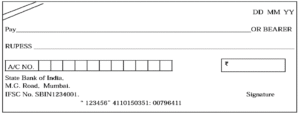

(3) Prepare specimen of Crossed cheque

Specimen of Crossed cheque :

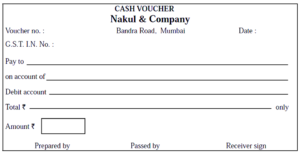

(4) Prepare specimen of Cash voucher.

Specimen of Cash voucher :

Question 7. Correct the following statements and rewrite the statements.

(1) All business transactions are recorded in the Journal.

Only monetary transactions are recorded in the journal.

(2) Cash discount is not recorded in the books of accounts.

Cash discount is recorded in the books of accounts.

(3) Journal is a book of Secondary entry.

Journal is a book of prime entry.

(4) GST is imposed by the Government of India from 1st July 2018.

GST is imposed by the Government of India from 1st July, 2017.

(5) Machinery purchased by the Proprietor decreases his capital.

Machinery purchased by the proprietor for the business increases his capital.

Question 8. Do you agree or disagree with following statements.

(1) Narration is required for every entry.

Agree

(2) GST stands for Goods and Sales Tax.

Disagree

(3) Trade discount is not recorded in the books of accounts.

Agree

(4) Wages paid for installation of Machinery is debited to Wages Account.

Disagree

(5) The process of entering or recording the transactions in a Journal is called as Journalising.

Agree

Question 9. Calculate the following :

(1) Purchased Motor Car from Tata & Company worth ₹ 2,00,000 at 18% GST. Find out GST amount.

To find the GST amount for a Motor Car purchased for ₹ 2,00,000 at 18% GST, calculate both the Central GST (CGST) and State GST (SGST).

Calculation Steps:

- Cost of Motor Car: ₹ 2,00,000

- CGST Amount (9% of ₹ 2,00,000) = ₹ 18,000

- SGST Amount (9% of ₹ 2,00,000) = ₹ 18,000

Total GST Amount: ₹ 18,000 (CGST) + ₹ 18,000 (SGST) = ₹ 36,000

(Alternatively, you can calculate it directly: ₹ 2,00,000 × 18% = ₹ 36,000).

(2) Paid Transport charges ₹ 10,000 @ 5% GST. Calculate CGST & SGST.

At 5% rate, GST for ₹ 10,000 will be ₹ 500 which includes ₹ 250 for CGST and ₹ 250 for SGST.

(3) Bought goods from Ranjan ₹ 10,000 @ 5% GST and 10% cash discount. Calculate cash discount.

GST on goods purchased = Cost of goods x GST @ 5% = 10,000 × \(\frac{5}{100}\) = ₹ 500

Value of good's purchased = Cost of goods + GST = 10,000 + 500 = ₹ 10,500

Cash discount = Value of goods x Cash discount @ 10% = 10,500 × \(\frac{10}{100}\) = ₹ 1,050

Cash discount = ₹ 1,050.

(4) Received cheque of ₹ 90,000 from Kiran in full settlement of his account ₹ 1,00,000/-. Calculate discount rate.

To calculate the discount rate for the transaction with Kiran, we first need to determine the amount of the cash discount provided.

Step 1: Calculate the Discount Amount :

In accounting, "full settlement" means the entire debt is cleared by paying a lesser amount, with the difference being treated as a cash discount.

Total Amount Due (Account Balance) = ₹ 1,00,000

Amount Received by Cheque = ₹ 90,000

Discount Amount = Total Due - Amount Received

Discount Amount = ₹ 1,00,000 - ₹ 90,000 = ₹ 10,000

Step 2: Calculate the Discount Rate

The discount rate is calculated as a percentage of the total amount that was originally due,.

Discount Rate = \(\frac{Discount\,amount}{Total\,amount\,due}\) × 100 = \(\frac{10000}{100000}\) × 100 = 10%

Answer: The discount rate is 10%.

(5) Sold goods of ₹ 1,00,000 at 10%. Trade Discount and 10% cash discount to Ram and received 50% amount by cheque. Calculate the amount of cheque received.

Trade discount is always deducted first from the list price and is not recorded in the books of accounts.

List Price = ₹ 1,00,000

Less: 10% Trade Discount (10% of ₹ 1,00,000) = – ₹ 10,000

Invoice Price = ₹ 90,000

50% of the amount is received by cheque.

∴ Cash Portion (50% of ₹ 90,000) = ₹ 45,000

∴ Credit Portion (50% of ₹ 90,000) = ₹ 45,000

Cash discount is a concession for prompt payment and is calculated only on the portion of the amount that is being paid immediately (the cash portion).

Cash Portion = ₹ 45,000

10% Cash Discount (10% of ₹ 45,000) = ₹ 4,500.

Cheque Amount = Cash Portion - Cash Discount = ₹ 45,000 - ₹ 4,500 = ₹ 40,500

Answer: The total amount of the cheque received is ₹ 40,500.

Q.10 Complete the following table.

| Sr. No. | Transactions | Debit Amount (₹) |

Credit Amount (₹) |

| 1 | Paid Income Tax ₹ 5,000 by cheque | ? | |

| - | Bank A/c | ||

| 2 | Received from Sonali ₹ 20,000 by RTGS. | Bank a/c | |

| - | ? | ||

| 3 | Sanjay became insolvent and not received ₹ 500 | ? | |

| - | Sanjay A/c | ||

| 4 | Purchased Horse for ₹ 10,000 | ? | |

| - | Cash A/c | ||

| 5 | Transferred from Fixed deposit A/c of proprietor to business Bank A/c ₹ 50,000 | Bank A/c | - |

| - | ? |

| Sr. No. | Transactions | Debit Amount (₹) |

Credit Amount (₹) |

| 1 | Paid Income Tax ₹ 5,000 by cheque | Drawings A/c | |

| - | Bank A/c | ||

| 2 | Received from Sonali ₹ 20,000 by RTGS. | Bank a/c | |

| - | Sonali's A/c | ||

| 3 | Sanjay became insolvent and not received ₹ 500 | Bad debts A/c | |

| - | Sanjay A/c | ||

| 4 | Purchased Horse for ₹ 10,000 | Live stock A/c | |

| - | Cash A/c | ||

| 5 | Transferred from Fixed deposit A/c of proprietor to business Bank A/c ₹ 50,000 | Bank A/c | - |

| - | Capital A/c |

**Buy Solutions PDF for Full Exercise Solutions (Theoretical + Practical Problem Solutions)

We reply to valid query.