Notes

|

Topics to be Learn :

|

Introduction to Book Keeping and Accounting Documents :

- Book Keeping means recording all day-to-day business transactions.

- These transactions are recorded on the basis of supporting documents.

Meaning, Importance and Utility of Accounting Documents :

Meaning of Document :

- A document is a piece of paper that provides detailed information of a transaction.

- It acts as a legal proof of the transaction.

- Example : When we purchase a computer for cash of Rs. 30,000, we receive a cash memo. This cash memo is called a source document.

Role of Documents in Accounting :

- The accountant first checks the reliability and legal proof of transactions.

- Every entry in the books of accounts is supported by proper documents.

- These documents are called Accounting Documents.

- Accounting documents form the base for recording transactions in the books.

Importance and Utility of Accounting Documents :

- Accounting documents are necessary for recording all transactions in the books of accounts.

- They help in recording transactions properly, whether manually or on computers.

- These documents are stored safely in physical files or accounting software.

- They serve as legal evidence in court matters.

- They are required for work related to the Charity Commissioner’s office.

- They are needed for payments and dealings with state government and local authorities.

The most important accounting documents for recording transactions in journal are as follows :

(1) Voucher (2) Cash Voucher (3) Tax Invoice (4) Credit Memo (5) Receipt and (6) Cheque.

(1) Voucher :

- A voucher is a document that supports a payment made by a businessman.

- It is a legal proof that a certain amount of money has been paid to a specific person or party.

Examples of Vouchers : Cash voucher, Bank voucher, Purchase voucher, Sales voucher, Travel bills, Wages bill, Salaries bill etc.

Types of Vouchers :

(a) Internal Voucher :

- Internal vouchers are prepared within the organisation.

- They are created by the business itself and signed by the payee.

- These are used when no external receipt is available.

- Examples: Taxi fare, bus fare, auto fare, etc.

(b) External Voucher :

- External vouchers are received from outside the business.

- They are issued by other parties or agencies for business transactions.

Examples:

- Tax invoice from seller for purchase of goods or stationery,

- Electricity bill receipt,

- Debit note,

- Credit note,

- Cash memo.

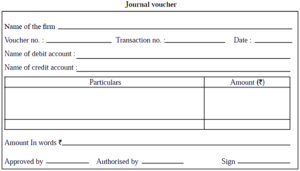

(c) Journal Voucher

- A journal voucher is the original or basic voucher.

- It is used for recording transactions in the journal book.

- All transactions are first supported by journal vouchers before being recorded.

Specimen of Journal voucher :

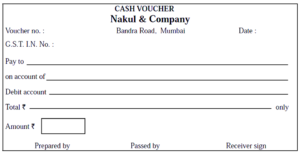

(2) Cash Voucher :

Meaning : A cash voucher is a document that shows proof of cash payments and cash receipts. Whenever money is paid in cash, a cash voucher should be prepared.

- If a receipt or document is received from the payee, it can be used as a voucher.

- The business may also prepare its own voucher and attach the external document to it.

- It serves as the basis for recording entries in the Cash Book.

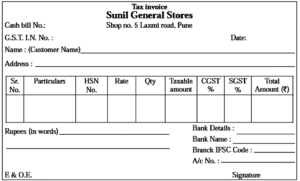

(3) Tax Invoice:

- Prepared by the seller to inform the buyer of the quantity, rates, GST (CGST/SGST), and total amount payable.

- It is viewed as an "Inward Invoice" (Purchase Invoice) by the buyer and an "Outward Invoice" (Sales Invoice) by the seller.

Specimen of Tax Invoice :

(4) Credit Memo:

- Also known as an invoice or bill, this is specifically issued when goods are purchased or sold on credit.

- It provides the details of goods for which an amount has become due.

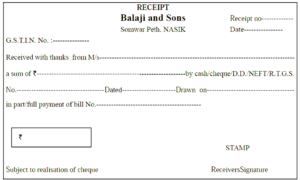

(5) Receipt :

- Document prepared by receiver of amount as an acknowledgement of the payment, is known as Receipt.

- On the basis of Receipt, entries will be made in the cash book.

(6) Cheque :

Meaning : A cheque is a written order given by an account holder to the bank.

- It instructs the bank to pay a certain amount of money on demand.

- The payment is made to a specified person or to the holder of the cheque.

Parties to a Cheque :

- Drawer : The person who writes (draws) the cheque. The account holder is always the drawer.

- Drawee : The bank on which the cheque is drawn. The drawee is always a bank.

- Payee : The person in whose favour the cheque is issued. The payee receives the payment.

Contents of a Cheque

- Name of the bank and branch address

- Date of issuing the cheque

- Name of the payee

- Amount in words and figures

- Name and signature of the account holder

- Cheque number

- MICR number

- IFSC code

- Account number

Types of Cheques :

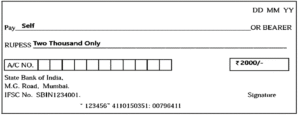

(i) Bearer Cheque :

- Used for immediate withdrawal of cash from the bank.

- It can be encashed by anyone during banking hours.

- The word “self” is written as payee and “bearer” is not cancelled.

Specimen of an Bearer Cheque

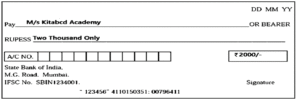

(ii) Order Cheque :

- Payment is made only to the person named on the cheque.

- The word “Bearer” is cancelled (struck off).

Specimen of an Order Cheque

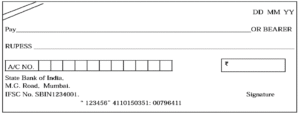

(iii) Crossed Cheque :

- Two parallel lines are drawn on the top left corner of the cheque.

- It cannot be encashed directly.

- It must be deposited into a bank account.

Specimen of a Crossed Cheque

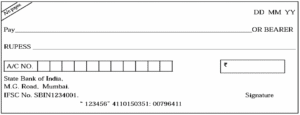

(iv) Account Payee Cheque :

- Words “Account Payee” are written between two parallel lines.

- The amount is credited only to the payee’s bank account.

- It is the safest type of cheque.

- It cannot be transferred to another person.

Specimen of a Crossed Account Payee Cheque

Meaning, Definition, Importance and Utility of Journal :

Introduction :

- A Journal is used to record daily financial transactions.

- It is known as the Book of Original Entry.

- Transactions are recorded first in the Journal before posting to the Ledger.

- Each record is called a Journal Entry.

- A journal entry includes debit, credit, and a short explanation (narration).

- Transactions are recorded in chronological order (date-wise).

Types of Books of Accounts

- Primary Books: Journal Proper, Special Journals (Purchase Book, Sales Book, Purchase Return Book, Sales Return Book, Bills Receivable Book, Bills Payable Book)

- Secondary Books: Ledger

Meaning :

- The word “Journal” comes from the French word “Jour”, meaning “Day”.

- So, Journal means a daily record of transactions.

- It records transactions as soon as they occur.

- It is the book of original or primary entry.

Definition :

- According to L.C. Cropper: A Journal is a book used to classify transactions for easy posting into the Ledger.

- According to Eric Kohler: A Journal is the book of original entry where transactions not recorded in special journals are entered.

Importance and Utility of Journal :

- Journal is the main book in which a complete and permanent record of all business transactions is kept with full details.

- It is easy to find and refer to transactions because records are maintained in date-wise (chronological) order.

- The nature and details of transactions can be clearly understood through a short explanation called narration.

- Entries in the journal are made using source documents, so they are accepted as legal evidence in court in case of disputes.

- Journal helps in detecting and preventing errors.

- Accuracy of accounts is ensured because total debit and credit amounts can be checked and matched.

- With the help of journal (and ledger), preparation of final accounts becomes easy.

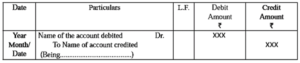

Specimen/ Format/ Ruling/ Proforma of Journal :

Journal of ----------------------------------------------

Explanation of Columns in Journal :

(i) Date : This column records the year, month, and date of each transaction.

- The year is written at the top.

- The month and date are written below it for each entry.

(ii) Particulars : This column is used to record the journal entry in three parts:

- Debit Account : It shows the name of the account to be debited. It is always written first. The word “Dr.” is written next to the debited account.

- Credit Account : It shows the name of the account to be credited. It is written on the next line. It begins with the word “To” after leaving some space.

- Debit and credit accounts are decided by applying rules of debit and credit.

- Narration : Narration is a short explanation of the transaction. It is written below the entry in brackets. It usually begins with the word “Being”.

(iii) Ledger Folio (L.F.) Number : It indicates the page number of the Ledger. It is written when entries are posted to the Ledger. It may be written in red ink to distinguish it from amounts.

(iv) Debit Amount : This column shows the amount of the debited account.

(v) Credit Amount : This column shows the amount of the credited account.

Casting of Journal :

- Casting of Journal means checking the arithmetical accuracy of the journal.

- The total of debit column and total of credit column is calculated on every page.

- On the last page, a Grand Total is prepared.

- This process is called Casting of Journal.

Journalising :

- Journalising is the process of recording business transactions in a systematic and summarised form in the journal.

Steps for Journalising :

- Identify the accounts involved and their types in the transaction.

- Apply the rules of debit and credit to decide which account to debit and credit.

- Record the date of transaction in the Date column.

- Write the name of the account to be debited on the first line and the credited account on the next line in the Particulars column.

- Write “Dr.” after the debited account and “To” before the credited account.

- Enter the amount in debit column for debited account and in credit column for credited account.

- Write a brief explanation (narration) below the entry starting with the word “Being”.

- Draw a line below the narration to separate one entry from another.

- Write the ledger page number in the L.F. column after posting to the ledger.

Recording of Journal Entries with GST (Goods and Services Tax) :

- Earlier, different taxes were charged by state and central governments at various stages of trade.

- To simplify the tax system, the Government of India introduced GST (Goods and Services Tax) on 1st July 2017.

- GST is known as “One Nation, One Tax, One Market”.

Codes Used in GST :

- HSN Code (Harmonized System of Nomenclature): Used for goods.

- SAC Code (Service Accounting Code): Used for services.

These codes help in proper classification of goods and services and in applying correct tax rates.

GST Rates (Slabs) : GST is charged at different rates depending on the type of goods or services: 0%, 5%, 12%, 18%, 28% (For the detailed list, please refer textbook:)

Note : The rates and types of GST are as prescribed by the government. GST rates are subject to change. Electricity, petrol, diesel etc are not under purview of GST.

Types of GST :

When GST is charged, it is divided into two parts:

- CGST (Central Goods and Services Tax) : Collected by the Central Government

- SGST (State Goods and Services Tax) : Collected by the State Government

Example of GST Calculation : If GST rate is 28% on goods:

- 14% is CGST

- 14% is SGST

Both CGST and SGST are charged equally on the value of goods.

Recording in Journal :

- While recording transactions, GST is shown separately in the journal entries.

- Purchase or sale amount and GST amount are recorded in different accounts.

- This helps in proper calculation and payment of tax.

Example 1: Purchased Laptop from Jalaram and Company worth ₹ 50,000 at 18% GST and amount paid by cheque

Cost of Laptop = ₹ 50,000

Add : CGST 9% = ₹ 4,500

SGST 9% = ₹ 4,500

Net value = ₹ 59,000

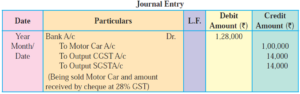

Example 2: Sold Motor Car for ₹ 1,00,000 at 28% GST and amount received by cheque

Cost of Motor Car = ₹ 1,00,000

Add : CGST 14% = ₹ 14,000

SGST 14% = ₹ 14,000

Net value = ₹ 1,28,000

Recording of Journal Entries :

Goods Account : Goods refer to items or commodities purchased by a businessman for resale. These are not for personal use but for business purposes.

Classification of Goods Account :

- Purchase Account : Records goods bought for resale.

- Sales Account : Records goods sold to customers.

- Return Outward Account (Purchase Return) : Records goods returned to the supplier.

- Return Inward Account (Sales Return) : Records goods returned by customers.

- Goods Withdrawn by Proprietor Account : Records goods taken by the owner for personal use.

- Goods Distributed as Free Samples Account : Records goods given free for promotion.

- Goods Destroyed by Fire Account : Records loss of goods due to fire.

- Goods Damaged or Lost in Transit Account : Records goods damaged or lost while transporting.

- Goods Pilfered or Stolen Account : Records loss of goods due to theft.

(1) Purchase Account : It is an account for recording all purchase of goods for trading/producing activity

There are two types of purchases : i) Cash Purchases ii) Credit Purchases

(i) Cash Purchases : When goods are purchased and payment is made to seller immediately, by cash or by bank, it is called as cash purchases.

Example : Purchased goods for cash from Mr. Sonu worth ₹ 2,000

In this transaction goods “comes in” on purchasing of goods and therefore purchase A/c is debited on purchase of goods and cash goes out therefore cash A/c credited the entry is as follows

(ii) Credit Purchases : When goods are purchased and payment is to be made in future date to seller i.e. Seller allows a certain period of time to the buyer to make the payment in respect of such purchases it is called as credit purchases.

Example : Purchased goods from Mrs Sonali worth ₹ 15,000 on credit.

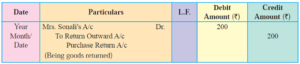

(2) Return Outward (Purchase Return)Account: This account is for recording return of goods purchased.

- Sometime goods purchased are returned to the supplier for various reasons.

- When goods purchased are returned to the supplier, it is called as “Return Outward” or "Purchase Return"

Example : Returned Goods worth ₹ 200 to Mrs. Sonali

In this transaction the goods “goes out” on returning of goods to supplier therefore Return Outward Account should be credited

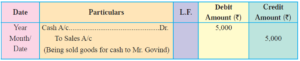

(3) Sales: Sales for the business means goods sold. Sales are classified in the following types a) Cash sales b) Credit sales.

(a) Cash sales: When goods are sold and money is received immediately, is called as cash sales.

Example : Sold goods worth ₹ 5,000 for cash to Mr. Govind.

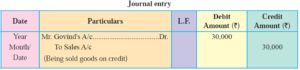

(b) Credit sales : when goods are sold and money will be received on future date it is called as credit sales.

Example : Sold goods to Mr. Govind for ₹ 30,000

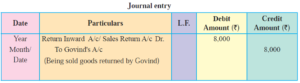

(4) Return Inward (Sales Returns): When the goods sold to customer are returned by that buyer to the Seller due to various reasons it is called as “Return Inward” or Sales Returned.

Example : Govind returned goods worth ₹ 8000 out of goods of ₹ 30,000 purchased by him

Evaluating Discount Structures :

| Feature | Trade Discount | Cash Discount |

| Nature | Reduction in catalog/list price. | Incentive for prompt payment. |

| Recording | Not recorded in the books. | Always recorded as a financial entry. |

| Order | Calculated first on catalog price. | Calculated on invoice price (after Trade Discount). |

Accounting for Unusual Goods Movements :

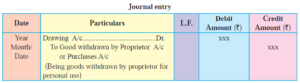

- Drawings: Goods taken for personal use. (Debit Drawings A/c; Credit Purchases/Goods Withdrawn A/c).

- Advertisement: Goods given as free samples. (Debit Advertisement A/c; Credit Purchases A/c).

- Physical Loss Scenarios:

- Uninsured: Debit Loss by Fire/Theft A/c; Credit Purchases A/c.

- Fully Insured: Debit Insurance Co. A/c; Credit Purchases A/c.

- Partly Insured: Debit Insurance Co. (Claim amount) and Loss by Fire (Loss amount); Credit Purchases A/c.

- Loss in Transit: This occurs when goods are damaged before reaching the buyer. (Debit Loss in Transit A/c; Credit Purchases A/c).

Example : Goods Withdrawn by Proprietor : When the proprietor takes goods from the business for personal use, it is called drawings. In this case, the Drawings Account is debited and Goods (Purchases) Account is credited, as the goods go out of the business.

Writing of Journal Entries :

Two types of journal entries we have viz.

(1) Simple Journal Entry : Simple Journal Entry is to be passed when in a transaction only two accounts are affected, one account is debited and other account is credited.

(2) Compound/Combined Journal Entries : A journal entry which contains more than one debit or more than one credit or both is called a combined / compound journal entry.

Compound vs. Simple Entries :

- A Simple Entry affects only two accounts.

- A Combined (Compound) Journal Entry is used when more than two accounts are affected by a single event, offering greater efficiency.

Example: The Kishor Transaction Consider selling goods worth ₹30,000 to Kishor, where he pays ₹10,000 immediately.

(1) Simple Method : In this method, the transaction is recorded as two separate events: first, the full credit sale, and second, the partial cash receipt.

Journal ….

| Date | Particulars | L.F. | Debit Amount (₹) | Credit Amount (₹) |

| Transaction A | Kishor's A/c .................... Dr. | 30,000 | ||

| To Sales A/c | 30,000 | |||

| (Being goods sold to Kishor on credit) | ||||

| Transaction B | Cash A/c .................... Dr. | 10,000 | ||

| To Kishor's A/c | 10,000 | |||

| (Being part payment received from Kishor) |

(2) Compound (Combined) Method : The compound entry is more efficient because it combines these effects into a single recorded event, netting out the credit to Kishor to show his actual remaining debt.

Journal of ….

| Date | Particulars | L.F. | Debit Amount (₹) | Credit Amount (₹) |

| Combined | Cash A/c .................... Dr. | 10,000 | ||

| Kishor's A/c .................... Dr. | 20,000 | |||

| To Sales A/c | 30,000 | |||

| (Being goods sold to Kishor and part payment received) |

Key Efficiency Note :

- In the simple entries, Kishor’s account is first debited by ₹30,000 and subsequently credited by ₹10,000.

- The compound entry is considered more efficient because it directly shows the net effect: a debit to Kishor’s account for the true remaining balance of ₹20,000.

We reply to valid query.