Notes

|

Topics to be Learn :

|

Meaning and Definition of Double Entry Book-keeping System :

Introduction :

- The modern system of book-keeping and accountancy was first introduced by Luca Pacioli on 10 November 1494.

- The present system of accounting is a modified and improved form of the work developed over the last five centuries.

Meaning of Book-keeping : Book-keeping is the art of recording business transactions in a systematic manner in the books of accounts.

- Its main purpose is to find out the financial result (profit or loss) and the financial position of the business.

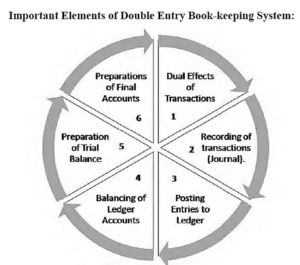

Double Entry Book-keeping System : According to the double entry system, every business transaction has two aspects. These two aspects are recorded in the books of accounts.

Definition : The recording of both aspects of a monetary transaction in the books of accounts using Debit and Credit is called the Double Entry System of Book-keeping.

Methods of Recording accounting information:

There are two methods of recording accounting information:

(i) Indian System.

(ii) English System : (a) Single Entry System (b) Double Entry System

(i) Indian System :

- In this system, business transactions are recorded in special books called ‘Bahi-khata’, ‘Kird’, etc.

- The records are usually written in Indian regional languages such as Marathi, Gujarati, Punjabi, etc.

- This system is traditional and mostly used by small traders and local businesses.

(ii) English System :

- In this system, business transactions are recorded systematically in books like Journal and Ledger.

- It is a more advanced and scientific system.

- It is widely used by most business organisations.

Types of English System

(a) Single Entry System : In this system, only one aspect of a transaction is recorded and the other aspect is ignored.

- Generally, only Cash Book and Personal Accounts are maintained.

- Therefore, it is considered an incomplete and unscientific system.

- It is suitable for small businesses and hawkers.

(b) Double Entry System : It is the most scientific, reliable, and complete method of recording business transactions. It records both aspects of every transaction.

Definition : According to J. R. Batliboi:

- Every business transaction has a two-fold effect.

- It affects two accounts in opposite directions.

- Therefore, one account is debited and another account is credited.

- Recording these two effects is called the Double Entry System.

Principles of Double Entry Book-keeping System :

- Two Aspects of Every Transaction : Every business transaction has two effects – Debit and Credit.

- Two Accounts Involved : One account is the receiver of the benefit. The other account is the giver of the benefit.

- Debit and Credit Rule : If one account is debited, the other account must be credited. Every debit has an equal and corresponding credit of the same amount.

Advantages of Double Entry Book-keeping System :

- Complete Record : In this system, both aspects of every transaction are recorded. Therefore, it provides a complete and systematic record of all business transactions.

- Accuracy : In double entry system, every debit has a corresponding credit. This helps to check the arithmetical accuracy of the books of accounts on any date.

- Determination of Business Results : All expenses, incomes, losses, gains, assets, liabilities, debtors and creditors are properly recorded. Therefore, it becomes easy to find the correct profit or loss of a business for a particular accounting period.

- Common Acceptance : The records maintained under this system are widely accepted by financial institutions, banks and government authorities.

Conventional Accounting System (Traditional) :

- The Indian system of accounting, based on traditional practices and commonly accepted rules, is called the Conventional Accounting System.

- In this system, clear rules, concepts and conventions are not properly defined.

- It is an incomplete system of recording transactions because it does not fully follow the principles of the Double Entry System.

Classification of Accounts :

Meaning of Account : An account is a summarized record of transactions related to a particular person, asset, liability, expense or income, recorded at one place.

- In daily business activities, many transactions take place, and each transaction affects different accounts.

- After a certain period, the businessman balances these accounts to know important information such as: Total capital, Total assets and liabilities, Total income and expenses of the business.

Definitions of Account :

- According to G. R. Batliboi: “An account is a summarized record of transactions affecting one person, one kind of property or one class of gain or loss.”

- According to Carter: “An account is a ledger record in a summarized form of all the transactions that have taken place with the particular person or thing specified.”

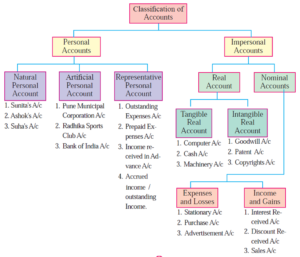

Classification of Accounts :

Accounts are mainly divided into two types:

- Personal Accounts

- Impersonal Accounts

(1) Personal Account : An account of a person or group of persons with whom the business deals is called a Personal Account.

Types of Personal Accounts :

(a) Natural Person’s Account : Accounts related to human beings or individuals.

- Examples: Parth’s A/c, Kalpana’s A/c, etc.

(b) Artificial Person’s Account : Accounts related to organisations or institutions created by law.

- Examples: Bank A/c, University A/c, Club A/c, etc.

(c) Representative Personal Account : Accounts that represent a person or group of persons with whom the business deals.

- Examples: Prepaid Insurance Premium A/c, Outstanding Salary A/c

(2) Impersonal Accounts :

All accounts other than personal accounts are called Impersonal Accounts.

Types of Impersonal Accounts

(A) Real Accounts : Accounts related to assets or properties owned by the business.

- Tangible Real Account : Accounts of assets that can be seen, touched and measured. Examples: Machine A/c, Cash A/c, Furniture A/c, etc.

- Intangible Real Account : Accounts of assets that cannot be seen or touched, but have value in money. Examples: Goodwill A/c, Patent A/c, Trademark A/c, Copyright A/c, etc.

(B) Nominal Accounts : Accounts related to expenses, incomes, losses, gains or profits. Examples: Wages A/c, Dividend A/c, Discount A/c, Rent A/c, etc.

Debit and Credit :

- Debit (Dr.): Left hand side of an Account is called Debit (Dr) side.

- Credit (Cr): Right hand side of an Account is called Credit (Cr) side.

Proforma of an Account

Dr. (Title of the Account) Cr.

| Date | Particulars | J.F. | Amount (₹) |

Date | Particulars | J.F. | Amount (₹) |

| 20…. | To …. A/c …. | -- | ---- | 20…. | By ….. A/c … | ---- | ---- |

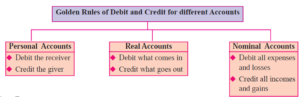

Golden Rules of Debit and Credit (Traditional Approach):

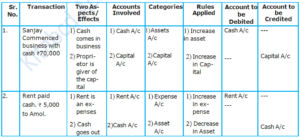

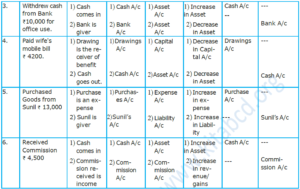

Illustration : I) From the following transactions find out

1) Two aspects 2) Two accounts 3) Classify the accounts

1) Commenced business with Cash ₹ 20,000.

2) Purchased goods on credit from Ajay ₹ 10,000.

3) Cash Sales ₹ 7,000.

4) Received commission ₹ 500.

5) Paid Rent ₹ 800.

Two Aspects, Two Accounts and Classify the Accounts.

| Sr.

No. |

Two aspects | Two accounts | Classification |

| 1. | Cash comes in

Proprietor (Capital) is the giver |

Cash A/c

Capital A/c |

Real A/c

Personal A/c |

| 2. | Purchases is an expense

Ajay is giver |

Purchases A/c

Ajay A/c |

Nominal A/c

Personal A/c |

| 3. | Cash comes in

Sales is an income |

Cash A/c

Sales A/c |

Real A/c

Nominal A/c |

| 4 | Cash comes in

Commission is an income |

Cash A/c

Commission A/c |

Real A/c

Nominal A/c |

| 5 | Rent is an expense

Cash goes out |

Rent A/c

Cash A/c |

Nominal A/c

Real A/c |

(1) Analysis of transaction by applying rules of Debit and Credit (Traditional Approach)

PROFORMA

| Sr. No. |

Transaction | Two Aspects/ Effects |

Accounts Involved |

Classification of Accounts |

Rules Applied |

Account to be Debited |

Account to be Credited |

| (1) | |||||||

| (2) |

Illustration : Prepare a chart showing analysis of the following transactions in a tabular form according to Traditional Approach :

(1) Started business with cash ₹ 25,000.

(2) Purchased goods of ₹ 10,000 for cash.

(3) Sold goods of ₹ 12,000 to Prihaan.

(4) Received interest ₹ 800.

(5) Paid stationery bill ₹ 800.

(6) Deposited cash ₹ 5000 into bank.

Classification of Accounts (Modern approach) :

In the following chart, different types of accounts have been summarised, which are divided into five categories for recording of the transaction :

Analysis of transaction by applying rules of Debit and Credit (Modern Approach) :

PROFORMA

| Sr. No. |

Transaction | Two Aspects/ Effects |

Accounts Involved |

Categories | Rules Applied |

Account to be Debited | Account to be Credited |

| (1) | |||||||

| (2) |

Illustraion :

(1) Classify the following accounts into Personal, Real and Nominal accounts.

| 1) | Stationery A/c | 2) | Mahesh's A/c |

| 3) | Machinery A/c | 4) | Capital A/c |

| 5) | Loss by Fire A/c | 6) | Pune Municipal Corp. A/c |

| 7) | Building A/c | 8) | Bank of Maharashtra A/c |

| 9) | Copyright A/c | 10) | Repairs A/c |

| 11) | Laptop A/c | 12) | Wages A/c |

| Personal Account | Real Account | Nominal Account |

| Mahesh's A/c | Machinery A/c | Stationery A/c |

| Capital A/c | Building A/c | Loss by fire A/c |

| Pune Municipal Corp. A/c | Copyright A/c | Repairs A/c |

| Bank of Maharashtra A/c | Laptop A/c | Wages A/c |

(2) Classify the following accounts under Personal, Real and Nominal Accounts.

| 1) | Cash A/c | 2) | Outstanding Salary A/c | 3) | Rohit's A/c |

| 4) | Furniture A/c | 5) | Life Insurance Corp. A/c | 6) | Goodwill A/c |

| 7) | Prepaid Insurance A/c | 8) | Trademark A/c | 9) | Commission A/c |

| 10) | Loan A/c | 11) | Drawings A/c | 12) | Interest A/c |

| Personal Account | Real Account | Nominal Account |

| Outstanding Salary A/c | Cash A/c | Commission A/c |

| Rohit's A/c | Furniture A/c | Interest A/c |

| Life Insurance Corp. A/c | Goodwill A/c | |

| Prepaid Insurance A/c | Trademark A/c | |

| Loan A/c | ||

| Drawings A/c |

(3) Classify the following accounts under Assets, Liabilities, Income and Expenditure.

| 1) | Prepaid Rent | 2) | Salary A/c | 3) | Bank Loan A/c |

| 4) | Motor Car A/c | 5) | Rent Payable A/c | 6) | Bad Debts A/c |

| 7) | Copyright A/c | 8) | Interest Received A/c | 9) | Dividend Received A/c |

| 10) | Premises A/c | 11) | Insurance Premium A/c | 12) | Audit Fees A/c |

| Assets | Liabilities | Income/Gains | Expenditure/

Loss |

| Prepaid Rent A/c | Bank Loan A/c | Interest Received A/c | Salary A/c |

| Motor Car A/c | Rent Payable A/c | Dividend Received A/c | Bad debts A/c |

| Copy Right A/c | Insurance Premium A/c | ||

| Premises A/c | Audit Fees A/c |

(4) Classify the following accounts into Assets, Liabilities, Income, Expenditure and Capital.

| 1) | Land and Building | 2) | Interest Received | 3) | Computer |

| 4) | Sundry Creditors | 5) | Bills Receivables | 6) | Discount Allowed |

| 7) | Sundry Debtors | 8) | Goodwill | 9) | Freight |

| 10) | Discount Received | 11) | Bills Payable | 12) | Amit`s Capital |

| 13) | Interest on Fixed deposit. | 14) | Bank Overdraft | 15) | Live Stock |

| 16) | Printing & Stationery | 17) | Cash at Bank | 18) | Rent Received |

| 19) | Repairs & Maintenance | 20) | Carriage | 21) | Outstanding Rent |

| 22) | Commission Received | 23) | Bank Loan | 24) | Electricity Bill |

| 25) | Copyright |

| Assets | Liabilities | Income/Gains | Expenditure/Loss | Capital |

| Land & Building | Sundry Creditors | Interest Received | Discount Allowed | Amit`s Capital |

| Computer | Bills Payable | Discount Received | Freight | |

| Bills Receivable | Bank Overdraft | Interest on Fixed deposit. | Repairs & Maintenance | |

| Sundry Debtors | Outstanding Rent | Rent Received | Carriage | |

| Goodwill | Bank Loan | Commission

Received |

Printing and

Stationary |

|

| Live Stock | Electricity Bill | |||

| Cash at Bank | ||||

| Copyright |

Accounting Equations :

Accounting equation signifies that the assets of a business are always equal to the total of its liabilities and capital. This fact can be represented in terms of accounting equation as follows :

Assets = Liabilities + Capital OR A = L + C

Total Assets = Total Liabilities

Assets = Liabilities

- The property of every description owned and possessed by the business is called asset.

- The rights of proprietor to the assets are called equities.

- The equity of creditors and the equity of owners represents debts of business and capital respectively.

Accounting equation for a transaction :

Example:-

(1) Rahul started business with Cash ₹ 50,000.

The accounting equation will be- Assets = Capital + Liabilities

Cash = Capital + Liabilities

₹ 50,000 = ₹ 50,000 + 0

₹ 50,000 = ₹ 50,000

(2) Rahul purchased Machinery from H.P. Co. on credit of ₹10,000.

The accounting equation will be- Assets = Capital + Liabilities

Cash + Machinery = Capital + Sundry Creditors

₹ 50,000 + ₹ 10,000 = ₹ 50,000 + ₹ 10,000

₹ 60,000 = ₹ 60,000

(3) Rahul purchased goods ₹ 20,000.

The accounting equation will be- Assets = Capital + Liabilities

Cash + Machinery + Stock = Capital+ Sundry Creditors

Old Bal. ₹ 50,000 + ₹ 10,000 + 0 = ₹ 50,000 + ₹ 10,000

New Transaction ₹ 30,000 + ₹ 10,000 + ₹ 20,000 = ₹ 50,000 + ₹ 10,000

New Balance. ₹ 30,000 + ₹ 10,000 + ₹ 20,000 = ₹ 50,000 + ₹ 10,000

₹ 60,000 = ₹ 60,000

Illustration–:

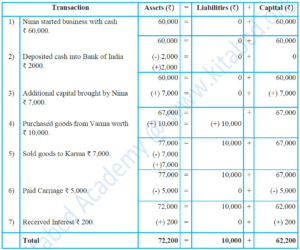

(1) Give the accounting equation for the following transactions-

- Nima started business with cash ₹ 60,000

- Deposited cash into Bank of India ₹ 2000

- Additional capital brought by Nima ₹ 7,000

- Purchased goods from Varma worth ₹ 10,000

- Sold goods to Karma ₹ 7,000

- Paid Carriage ₹ 5,000

- Received Interest ₹ 200

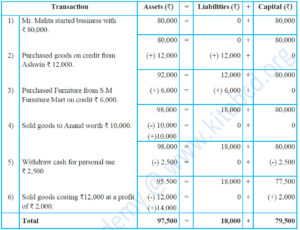

(2) Show the accounting equation for the following transactions-

- Mehta started business with ₹ 80,000

- Purchased goods on credit from Ashwin ₹ 12,000.

- Purchased Furniture from S.M Furniture Mart on credit ₹ 6,000

- Sold goods to Anand worth ₹ 10,000.

- Withdrew cash for personal use ₹ 2,500

- Sold goods costing ₹ 12,000 at profit of ₹ 2,000.

We reply to valid query.